Across the United States, the startup community is still reeling after Silicon Valley Bank’s collapse, the largest bank failure since the 2008 financial crisis, and Main Street businesses are no exception.

In the “Main Street Health Q1 2023: Using Finance to Ease Recession Fears” report by PYMNTS, we surveyed more than 500 small- to medium-sized businesses (SMBs) with physical stores located in commercial areas across the U.S. to uncover how these business owners are adjusting their economic predictions for the upcoming year, as well as to identify the primary challenges they perceive in sustaining their operations both presently and in the face of a potential economic downturn.

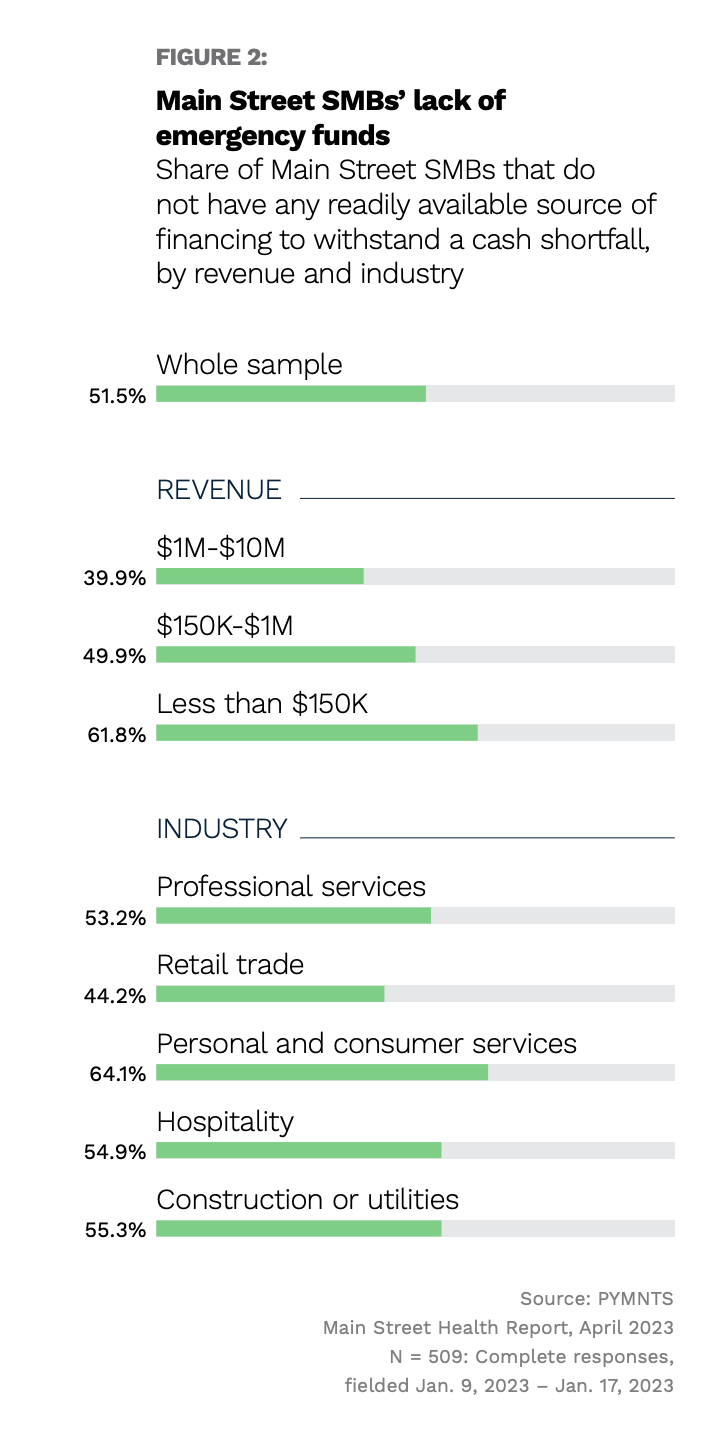

Per the results from the joint PYMNTS-Enigma study, Main Street’s recession fears and pessimism about the economy are justified, particularly among SMBs.

In fact, more than 50% of Main Street SMBs do not have any readily available source of financing to survive a cash flow crisis, highlighting a dire need for alternative funding options to keep small businesses afloat in the short term.

The report also found that the smaller the business, the less likely it is to have ready access to emergency financing options and the higher the risk of folding in the event of cash flow deficit.

Against that backdrop, it was revealed that 62% of Main Street SMBs with less than $150,000 in annual revenues have no access to funding to help defend against potential cash flow shortfalls, while nearly 50% generating annual revenues between $150,000 and $1 million find themselves in the same situation.

“Even 40% of Main Street SMBs generating between $1 million and $10 million in annual revenue have no readily available financing options that they might need to stay afloat if there were a sudden drop in sales,” the report added.

Drilling down into the data further showed that firms operating in the fields of personal and consumer services (64.1%) and those in construction or utility (55.3%) are the least prepared to navigate a deficit in cash flow. They are closely followed by firms in the hospitality sector (54.9%) and those operating in the professional services industry (53.2%).

Even among Main Street SMBs engaged in retail trade — the most likely to have access to readily available financing options, per the report — 44% of firms still reported a lack of available financing, further emphasizing the significant funding shortfalls experienced by these Main Street SMBs.

Consequently, all Main Street SMBs stand to benefit from access to additional funding alternatives to weather a financial storm, regardless of industry or size.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More