Access to business financing remains a significant challenge for small- to medium-sized businesses (SMBs), with many finding it increasingly difficult to secure traditional funding from banks.

According to data from a recent study conducted by PYMNTS Intelligence and Cross River, the share of SMBs that reported having access to business financing sources dropped from 42% to 39% between April and July. Even larger firms, which are more financially stable, faced challenges in accessing financing, with only 46% reporting access to business financing in July, compared to 59% in April.

The study reveals that smaller SMBs — generating less than $1 million in annual revenue — are particularly vulnerable during tough economic times. Nearly 10% of these smaller firms consider themselves at risk of closure.

On the other hand, larger SMBs — generating revenues between $1 million and $10 million — are more stable, with only 4.8% identifying themselves as at risk of closure. This suggests that smaller firms face tighter short-term working capital and limited financing options compared to their larger counterparts.

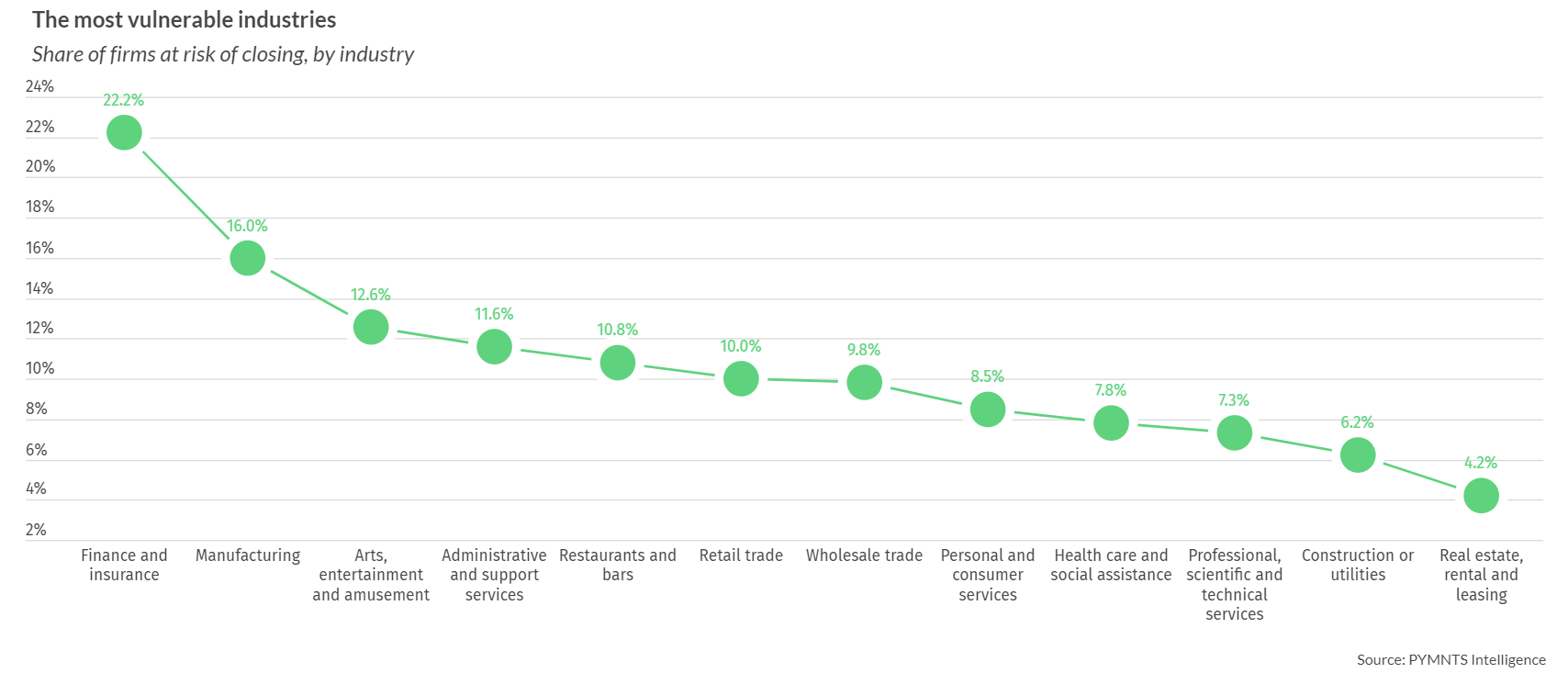

Drilling down into the study further reveals that the finance and insurance industries are the most vulnerable, with 22% of SMBs in these sectors reporting a risk of closure. Manufacturing and arts and entertainment sectors also face higher-than-average closure risks, at 16% and 13% respectively. These industries have less working capital and access to financing than others, making them more susceptible to economic downturns.

To bridge the gap, SMBs predominantly rely on corporate credit cards as their primary form of business financing. However, many SMBs also turn to personal credit sources and assets owned by the business owners, indicating the difficulty they face in accessing business financing.

Personal credit cards ranked as the second-most used form of financing for SMBs, with 9.3% relying on them. Other sources of financing included personal loans from banks, liquidating personal investments, loans from family members or friends, and mortgage loans.

Overall, as traditional banks become less accessible for many industries, there is an opportunity for FinTechs to step up and fill the gap by providing alternative business credit sources that can improve SMBs’ access to financing solutions while managing risk.

Firms across Europe, Middle East and Africa (EMEA) have been rising up to this challenge. Earlier this year, PYMNTS reported that FinTechs across the three regions had stepped up to plug the small business finance gap.

These include London-based embedded finance provider Liberis, which raised an additional $32.6 million on top of the $172.57 million the company raised last September, with plans to grow its receivables financing proposition across the continent. Another British FinTech, iwoca, extended its credit line with Pollen Street Capital from $150 million to $204 million after seeing the total number of SMBs it funded across the U.K. and Germany increase by 54% in 2022.

In February, South African FinTech Lulalend announced a $35 million Series B round to help fund its SMB lending platform, stating in a blog post that the new capital would enable the firm to “service the surging demand for the fast access to working capital we offer businesses.”