Artificial intelligence is quickly moving from a productivity tool to an operating layer for commerce. Consumers already use AI to search for products, compare prices, plan travel and manage everyday financial tasks. Merchants are experimenting with personalized shopping experiences powered by real-time data. Banks and issuers are trying to modernize systems built for an earlier era of payments. Across the ecosystem, one issue is becoming clear. AI can accelerate commerce, but only if the infrastructure behind it can keep pace.

That challenge is creating new pressure points for the financial services industry. Fraudsters are using the same AI tools as legitimate businesses, allowing scams to scale faster and appear more convincing. Consumers expect checkout experiences to feel seamless and invisible. Yet payment systems still rely heavily on manual authentication and fragmented data flows. Banks want to launch new AI-enabled products but often find themselves constrained by legacy systems that were never designed for real-time intelligence or automated decision-making.

Against that backdrop, Visa is increasingly focusing its value-added services strategy on becoming the connective layer between AI-driven commerce and the trust that supports it. Across a series of interviews conducted by PYMNTS CEO Karen Webster as part of the Visa The Edit series, Visa executives outlined how the company is embedding intelligence, identity, risk management and infrastructure modernization directly into the payments ecosystem.

Together, the conversations revealed a broader thesis about the future of payments. AI may transform the customer experience, but value-added services will determine whether that transformation can scale safely, securely and profitably.

Three Themes Emerging From the Series

- Trust Becomes Infrastructure: As AI agents begin participating in commerce, trust cannot rely solely on visible checkout steps. Identity, consent, authentication and dispute resolution increasingly need to operate invisibly in the background.

- Real-Time Data Changes Everything: AI depends on immediate access to clean, governed data. Across banking, fraud prevention and payments, real-time infrastructure is becoming the foundation for personalization, compliance and automation.

- Fraud Evolves Alongside AI: Fraudsters are using AI to industrialize scams, automate attacks and exploit fragmented payment systems. Defending against those threats requires intelligence embedded throughout the payments lifecycle, not isolated point solutions.

Trust Has to Scale

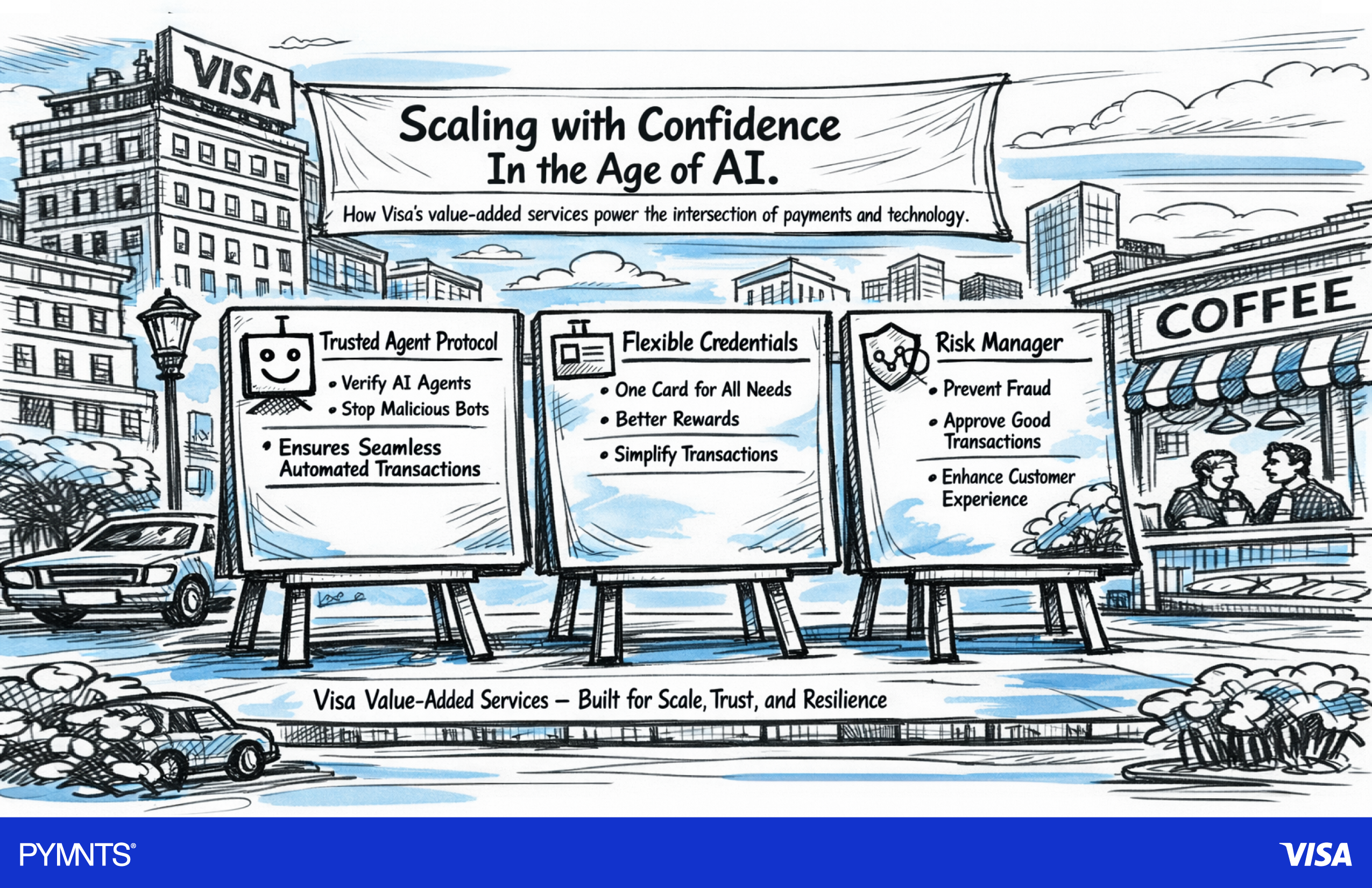

In his conversation with Karen Webster, Andrew Torre, president of Visa’s value-added services division, described agentic commerce as the next major shift in digital payments. Consumers are using AI tools to search, compare and make purchasing decisions. The next step, he argued, is software agents that can complete purchases autonomously on behalf of consumers. But the real challenge is not whether AI can shop. It is whether consumers and businesses will trust it enough to let it transact.

Torre framed value-added services as the operational layer that enables agentic commerce. AI agents may eventually streamline purchasing journeys, but those journeys still require identity verification, authentication, tokenization, consent capture and dispute resolution behind the scenes. Without those safeguards, automation risks becoming unmanageable.

“One of the constraints we’ve seen is a lot of customers using their legacy, whether it’s in-house or another issuer processing stack. It’s complicated to deploy,” Torre said.

A recurring theme in the conversation was the idea that Visa has already spent decades building many of the capabilities now becoming essential for AI commerce. Torre pointed to Visa’s long history of using AI for fraud detection and risk scoring, arguing that many banks and merchants are more prepared for agentic commerce than they realize. The company’s newer initiatives, including Visa Intelligent Commerce and its Trusted Protocol framework, are designed to extend those capabilities into environments where software agents act on behalf of consumers.

Torre repeatedly returned to the importance of reversibility and consumer control. He used a simple example involving his daughter searching for a difficult-to-find pair of Nike sneakers in highly specific colors. In an AI-driven shopping environment, the agent might locate and purchase the shoes automatically. But if the wrong product arrives, the consumer still expects a straightforward path to dispute the purchase and reverse the transaction.

“Let’s just say my daughter’s sneakers, they come, and they’re not the right sneakers,” Torre said. “They’re giant, in the wrong colors, and she’s upset.”

That moment, Torre argued, captures the broader challenge facing AI-powered commerce. Automation can speed up decisions and reduce friction, but trust still depends on transparency, accountability and consumer protections. In his view, value-added services are becoming less of an add-on and more of the architecture that allows AI commerce to function at scale.

Infrastructure Must Evolve

Michele Herron, senior vice president and head of North America value-added services at Visa, focused her conversation with Webster on the widening gap between consumer expectations and payments infrastructure. Consumers expect commerce experiences to feel seamless and intelligent, shaped by AI systems that understand their preferences and anticipate their needs. Yet many payment systems still require manual authentication steps that interrupt the buying experience.

“If I’m on my phone, and I want to buy, and my favorite payment button is not available, I’m out,” Herron said.

Herron described the payments industry as being at the early edge of true agentic commerce. Consumers are already becoming comfortable with AI-driven recommendations and digital assistants. Over the next several years, she expects those assistants to evolve into autonomous agents capable of handling tasks such as reordering household goods, booking travel and selecting payment methods automatically.

A central part of Herron’s argument was that payment infrastructure must evolve from a constraint into an accelerator for innovation. She pointed to Visa’s orchestration layer and tokenization capabilities as examples of how existing payment tools can be adapted for AI-driven commerce. In an agentic environment, tokenized credentials could allow AI assistants to complete transactions securely without exposing sensitive card data.

Herron called tokenization “the future of agentic” because it allows payment credentials, spending limits, preferences and authentication rules to travel together inside a trusted framework.

The conversation also explored how AI could reshape payment choice itself. Rather than consumers manually selecting a card or payment method, intelligent assistants could optimize those decisions automatically. An AI system might choose a rewards card for travel purchases, an installment option for a larger transaction or a digital wallet for speed and convenience.

That same intelligence could transform loyalty programs and offers. Herron acknowledged that many current reward systems feel disconnected from the purchase moment.

“Loyalty and card-linked offers today can sometimes be a little static … and a little reactive,” she said. With AI and tokenized data integrated directly into the payments flow, incentives could become far more dynamic and personalized. Merchants and issuers would gain the ability to influence decisions in real time, rather than after a transaction has occurred.

Still, Herron emphasized that automation cannot come at the expense of security. In an environment where AI agents transact autonomously, payment systems must verify not only identity but also intent. Visa’s approach combines cryptographic authentication, behavioral analysis and contextual signals to determine whether a transaction reflects legitimate consumer behavior.

For Herron, the broader goal is straightforward: modernize payments infrastructure so innovation can move as quickly as consumer expectations.

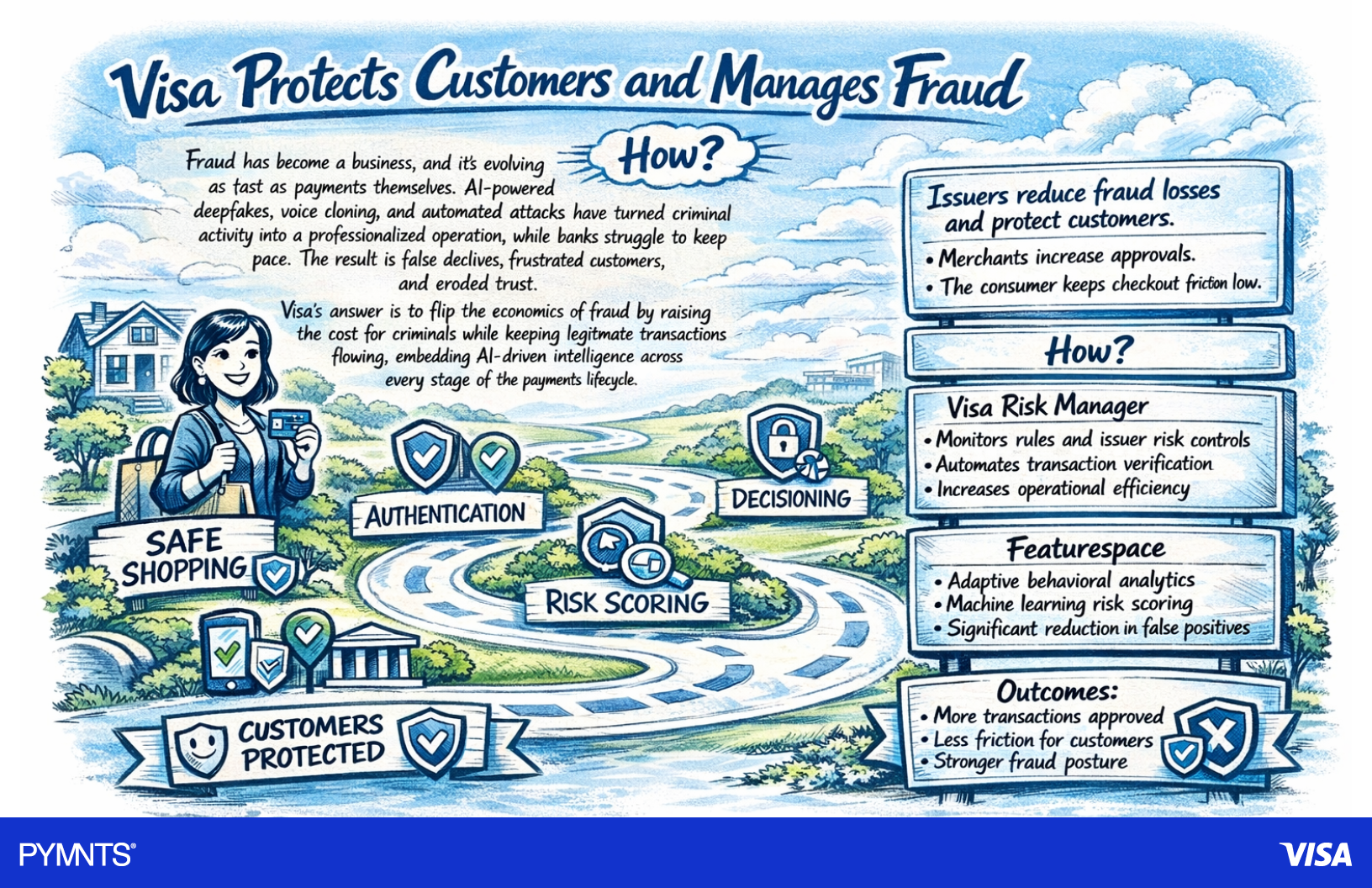

Fraud Becomes Industrialized

James Mirfin, Visa’s senior vice president and head of risk and security intelligence solutions, focused his interview on the darker side of AI-driven commerce: the rapid industrialization of fraud.

“Fraud has become a business, an economy,” Mirfin told Webster.

His argument was that AI has fundamentally changed the scale and sophistication of modern fraud operations. Criminal organizations are no longer running isolated scams manually. They are using automation, deepfakes, voice cloning and AI-powered agents to operate at an industrial scale.

Mirfin warned that modern fraud operations are increasingly patient and coordinated. Stolen credentials may sit dormant for months before being activated. Fraudsters continuously test systems, adapt tactics and exploit fragmentation across payment rails. Consumers often assume the same protections apply across cards, faster payments and other digital payment methods, but those protections vary significantly.

The result, Mirfin said, is a growing challenge for financial institutions trying to balance fraud prevention with customer experience. Banks face structural disadvantages because they operate within regulatory and operational constraints.

“Banks aren’t notorious for being fast,” Mirfin said.

False positives and false declines have become major friction points across commerce. Consumers become frustrated when legitimate transactions are blocked, while merchants lose sales and trust erodes. Mirfin argued that solving this problem requires intelligence embedded across the full payments lifecycle rather than isolated at a single checkpoint.

Visa’s strategy is to connect signals across provisioning, authentication and authorization. Instead of treating those functions separately, the company is building systems where intelligence gathered at one stage informs decisions at another. Visa can analyze patterns across its global network and deliver real-time risk insights to issuers.

Mirfin also discussed how Visa is layering behavioral analytics into its fraud tools following the acquisition of Featurespace. The focus is increasingly on understanding what legitimate customer behavior looks like, not just identifying suspicious activity.

“The strategic objective is to flip the economics,” Mirfin said.

That phrase captured the broader philosophy behind Visa’s fraud strategy. Rather than simply blocking attacks, the company wants to make fraud so expensive and inefficient that criminals cannot sustain it profitably.

Mirfin argued that scale itself has become a defensive advantage. Fraudsters operate collaborative ecosystems, sharing tools and stolen credentials across networks. Visa’s response is to create a larger collaborative ecosystem involving issuers, merchants, acquirers and partners.

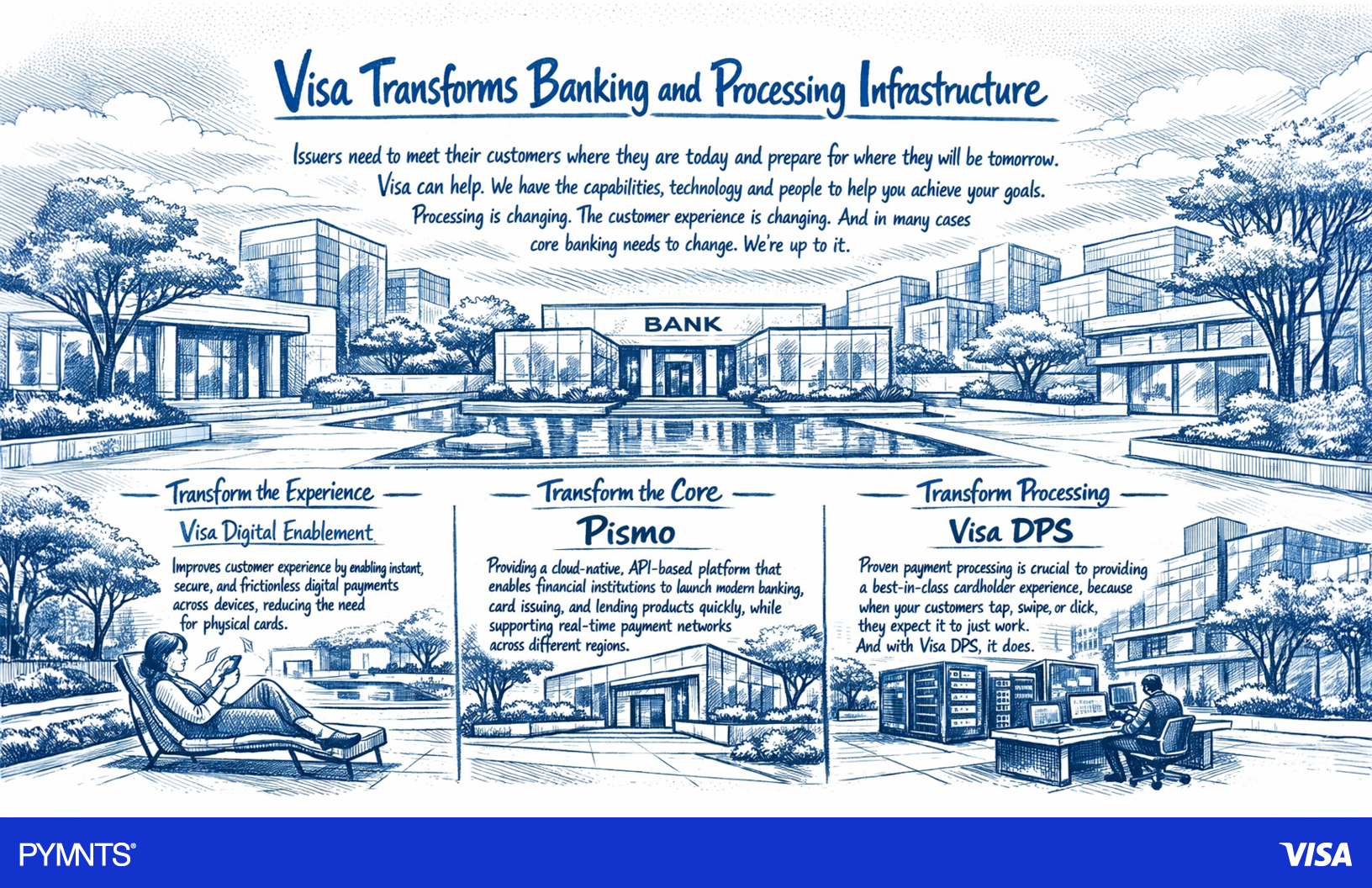

Modernization Can’t Wait

Kathleen Pierce-Gilmore, senior vice president and global head of issuing solutions at Visa, approached AI through the lens of infrastructure modernization. Her central argument was blunt: banks can no longer separate AI strategy from core infrastructure decisions.

“If you don’t have well-understood, well-managed, well-governed data, it’s going to be really hard to use AI,” Pierce-Gilmore said.

She described legacy core systems as increasingly incompatible with the demands of real-time, AI-enabled banking. Many banks still operate in fragmented, batch-based environments where data is trapped across disconnected systems. Pierce-Gilmore referred to those silos as “data prisons.”

That fragmentation affects far more than customer experience. It also complicates compliance, governance and risk management at a time when regulators themselves are still determining how to supervise AI.

Pierce-Gilmore argued that modernization is no longer optional. Banks are under pressure to deliver real-time experiences, launch new products faster and maintain transparency around how data moves through AI systems.

“I do think there is a greater sense of urgency than ever,” she said.

One of the conversation’s strongest themes was the importance of modular modernization. Rather than forcing banks to undertake massive core replacements, Visa’s approach centers on enabling institutions to modernize incrementally. Pismo, the cloud-native issuer processing and banking platform that Visa acquired, plays a central role in that strategy.

Pierce-Gilmore said many banks face technology queues that stretch over multiple years, making full-scale transformation impractical in the near term. Modular infrastructure allows institutions to launch new capabilities while continuing broader modernization efforts in parallel.

The conversation also highlighted how real-time infrastructure changes customer engagement itself. Pierce-Gilmore used the example of a consumer paying down a credit balance and instantly receiving updated available credit, relevant alerts and personalized offers tied to that activity.

“You can do that in a much more seamless and relevant way if you’ve got the data at the time that it’s happening,” she said.

For Pierce-Gilmore, the future of banking infrastructure is less about a fixed destination and more about adaptability. Banks cannot predict every future AI use case or regulatory requirement, but they can build systems flexible enough to evolve alongside them.

Her closing remark captured the conviction behind Visa’s infrastructure strategy.

“I would put my whole life savings on the modernization of infrastructure,” Pierce-Gilmore said.