Studies have found that B2B invoices take an average of 37.4 days to settle, a pace that is largely due to the business world’s lingering reliance on analog payment methods like paper checks.

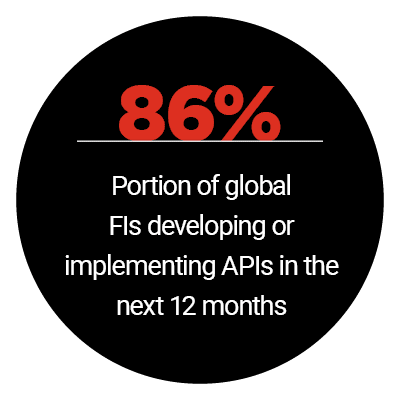

Digitizing these payments has been a top priority for banks, payments processors and businesses for several years, but this digitization has its own fair share of obstacles like interfacing disparate banking software and ensuring fraudsters cannot intercept payments mid-transfer. Application programming interfaces (APIs) and open banking are being harnessed to face these obstacles in turn, but their implementation has been slow in much of the world, including the U.S.

In the July “B2B API Tracker®,” PYMNTS explores the latest developments in the B2B API space, including new open banking initiatives in the U.S. and the United Kingdom, a study of how open banking has reduced the need for outmoded data sharing practices like screen scraping, and an examination of how legacy systems have hindered the spread of open banking.

Developments From Around the World of B2B APIs

Developments From Around the World of B2B APIs

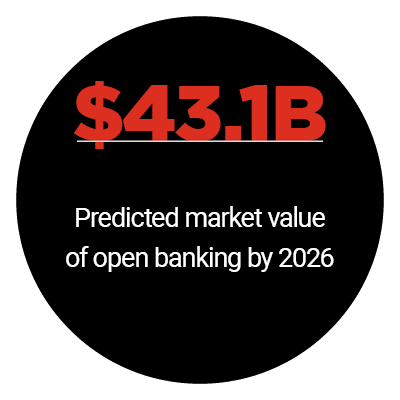

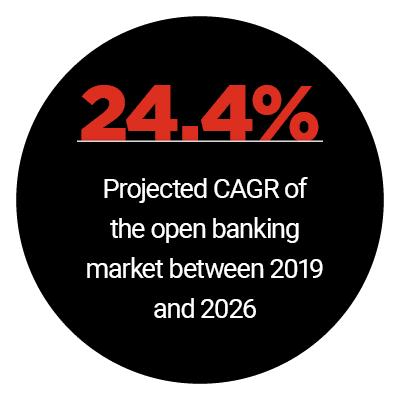

The European Union is one of the world’s leaders in embracing open banking, thanks to the revised Payment Services Directive (PSD2) mandating open banking and APIs among its member states. Banks in the EU currently spend between 50 million euros ($56.2 million) and 100 million euros ($112.3 million) on average each year on open banking investments. Some banks are further along in their open banking implementations than others, however, with 63 percent of banks increasing their open banking budgets each year, and 10 percent reducing their open banking budgets.

The U.K. is also forging ahead in its open banking initiative despite not being an EU member state anymore. A British FinTech-as-a-service company recently developed a new solution that harnesses APIs to connect with banks and accelerate B2B payments while also being compatible with 900 different payment methods in more than 100 countries. This solution is fueled by the firm’s partnerships with ClearBank, Mastercard, Payzone, Visa and other payment companies that power these transactions, creating a payment network for online marketplaces, B2B payment companies, FinTechs and others. The company plans to augment the solution by processing cross-border B2B payments in the near future as well.

Alabama-based bank holding company BBVA is also getting in on the open payments game with the launch of a new real-time B2B payments service powered by BBVA’s APIs and based on  Visa’s push payments offering, Visa Direct. This new system offers users the ability to conduct real-time payments and digital bill pay, and it is one of 30 based on Visa Direct, which had processed 2 billion transactions as of the beginning of 2020. The first customers of BBVA’s solution are reportedly B2B marketplace Tuvoli and business bank Wise.

Visa’s push payments offering, Visa Direct. This new system offers users the ability to conduct real-time payments and digital bill pay, and it is one of 30 based on Visa Direct, which had processed 2 billion transactions as of the beginning of 2020. The first customers of BBVA’s solution are reportedly B2B marketplace Tuvoli and business bank Wise.

For more on these and other B2B API news items, download this month’s Tracker.

US Bank on the Challenges Impeding Open Banking Adoption for B2B Payments

The tedium and pain points of B2B payments are well documented, with banks and payments processors struggling with incompatible systems that delay payments and increase their fees. Open banking can enable seamless transfers between banks and thus accelerate payments, provide heightened security and keep customers more apprised of their payments’ status, but its implementation has had several hiccups in the U.S.

In this month’s Feature Story, PYMNTS spoke with Gareth Gaston, executive vice president and head of digital platforms at U.S. Bank, about how legacy systems and a lack of regulatory oversight have impeded open banking’s adoption in the U.S.

Deep Dive: How B2B Payments Benefit From Open Banking Principles

Deep Dive: How B2B Payments Benefit From Open Banking Principles

The advent of open banking has been a game changer for the global financial industry, with initiatives around the world allowing for open data access between banks, FinTechs and developers looking to streamline and simplify app development. One field already feeling the effects of open banking is B2B payments, with APIs being developed for real-time data gathering, invoice issuance and a host of other features.

This month’s Deep Dive explores the benefits that open banking has provided to the B2B payments industry, and how it reduced the field’s reliance on outdated and risky practices, such as screen scraping.

About the Tracker

The “B2B API Tracker®,” done in collaboration with Red Hat, is your go-to monthly resource for updates on trends and changes in B2B APIs.

B2B payments account for $25 trillion in the United States each year, but these transactions are often fraught with frustrations and challenges.

B2B payments account for $25 trillion in the United States each year, but these transactions are often fraught with frustrations and challenges.