Before stablecoins, cryptocurrencies or even the blockchain technology on which these are based, eMoney emerged as a concept that promised to revolutionize commerce. Instead of cash, checks or cards, eMoney advocates envisioned a world in which transactions were made easily and with little friction over electronic channels.

Some of the earliest iterations of eMoney came in the form of PayPal accounts and prepaid debit cards, and these became mainstays of early electronic commerce. They paved the way for the emergence of cryptocurrencies, which took digital transactions to a new level by removing the need for a centralized authority and making transactions secure and transparent. Stablecoins — which peg their value to fiat currencies or other reserve assets — were introduced with the purpose of reducing or even eliminating the price volatility associated with cryptocurrencies while maintaining the benefits of crypto transactions, such as immediacy and immutability.

This month, PYMNTS examines eMoney tokens, stablecoins and cryptocurrencies, the roles they play and how consumers have responded to these payment options.

The Emergence and Growth of Cryptocurrencies

While cryptocurrencies were not the first attempt at independent electronic currency, blockchain technology made it possible to conduct immutable transactions, whether with cryptocurrencies or another digital asset. This means that the information exchanged, the transaction, could not be altered or manipulated. As a result, supply can be limited and there is no potential for fraudulent or counterfeit currency to be circulated.

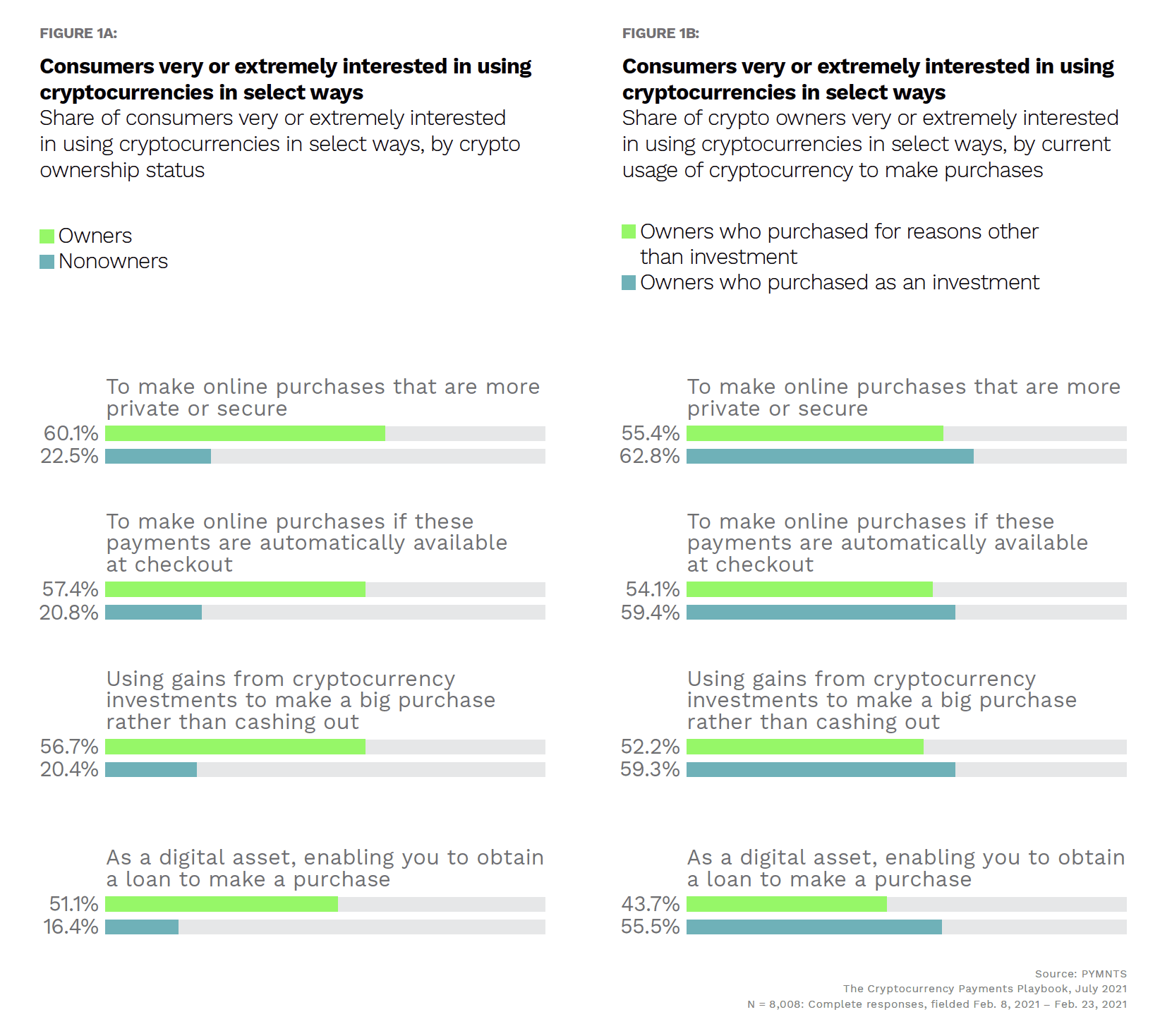

In the years since its inception, cryptocurrency has gained acceptance among the general population. While only 19% of consumers own cryptocurrency, 91% are aware of it. Among crypto owners, only 30% reported making an online purchase with their crypto assets, but perhaps more indicative of crypto’s growth as currency is the fact that 21% used it for in-store purchases.

In a world where a combined 32% of millennials and bridge millennials prefer merchants that accept cryptocurrencies, crypto-based transacting has become intermingled with other forms of eMoney. Merchants and retailers want access to the benefits of accepting crypto payments, such as the immediacy of funds, the availability to operate 24/7 year-round and, in some cases, the lower cost of transactions, but some worry about potential volatility. As a result, companies such as Mastercard and Visa have developed platforms that convert consumers’ cryptocurrencies into fiat currency that is then transferred to merchants. Crypto owners reported that 54% of their online crypto purchases and 64% of their in-store crypto purchases were made with prepaid debit cards.

The data from these tables shows how much crypto owners value the privacy offered by cryptocurrencies, with 60% of respondents saying they would use crypto to make online purchases in a more private and secure way. Additionally, the data suggests that crypto owners may have a longer commitment to the digital assets, as 57% will not cash out the gains from cryptocurrency investments, compared to only 20% of nonowners who would not cash out a crypto gain.

The data from these tables shows how much crypto owners value the privacy offered by cryptocurrencies, with 60% of respondents saying they would use crypto to make online purchases in a more private and secure way. Additionally, the data suggests that crypto owners may have a longer commitment to the digital assets, as 57% will not cash out the gains from cryptocurrency investments, compared to only 20% of nonowners who would not cash out a crypto gain.

Seeking a Stable Crypto Option

As the name suggests, stablecoins are intended to be more stable than other cryptocurrencies by serving as tokenized versions of reserve assets. This has made stablecoins popular for investment and decentralized finance (DeFi) crypto loans, as they are perceived as a better option than fiat currencies since transactions using these digital assets still benefit from the features of blockchain-based assets, such as immutability and record-keeping.

Stablecoins are still cryptocurrencies, and transactions on public blockchains can be completed at any time and can be cryptographically secured. These transactions can be based on smart contracts, with funds secured and released based on milestones within the program rather than requiring a third-party intermediary. Improved stability also means that stablecoins could have greater utility than other cryptocurrencies for everyday spending.

The stability of stablecoins is predicated on the underlying reserve assets, however, and the assumption of stablecoins’ inherent stability has been rocked by recent devaluations. Allegations have included misrepresentation of the actual reserve asset relationship to specific stablecoins, and concern over the impact of secondary market activity has invited calls for regulatory solutions.

Feeding a Consumer Need

While crypto’s regulatory future remains uncertain and innovations may continue to change the crypto space, consumer desire for an electronic monetary solution remains the same. Sixty percent of crypto owners expressed high levels of interest in crypto as a means of making online transactions more private and secure, and 23% of nonholders shared that same interest. Even among those who own crypto as an investment, 59% would rather use gains to make large purchases instead of simply cashing out, showing a long-term commitment to the underlying assets as an investment.

Regardless of the challenges, many consumers believe cryptocurrencies are the future of money, and they like the idea of secure, private and anonymous transactions. Whether they own crypto or not, consumers want the benefits eMoney first promised — faster, simpler and more reliable transactions — with the added value of blockchain-based tokens and cryptocurrencies.