Now nearly a quarter of the world’s population, millennials and their slightly older bridge millennial friends are the most courted of all cohorts from a marketing perspective, and their spending behavior is the obsession of virtually every brand and merchant.

In this Millennial Minute, we look at these digital-first consumers as it pertains to their use of buy now, pay later (BNPL) alternative credit versus use of store-issued credit cards.

The BNPL revolution is seen as being carried aloft primarily by millennial consumers, and that’s true. But when and why this demographic chooses installments over other forms of credit is an image that’s been somewhat distorted by the blizzard of BNPL headlines in the past few years.

We analyzed this question in “The Truth About BNPL And Store Cards,” a PYMNTS and PayPal collaboration based on a census-balanced survey of over 2,160 U.S. consumers.

Millennials Embrace BNPL

For context, the study found that 52 million U.S. consumers had used BNPL by the end of 2021. Traditional card issuers continue watching the situation intently, concerned that BNPL either will — or already is — siphoning sales away from store cards to third-party BNPL solutions.

Overall, “The Truth About BNPL And Store Cards” report found that 59 million U.S. consumers shopped with merchants offering store cards within the prior 30 days, and of that number we found that approximately 4.9 million consumers (8.3%) financed the purchase using BNPL.

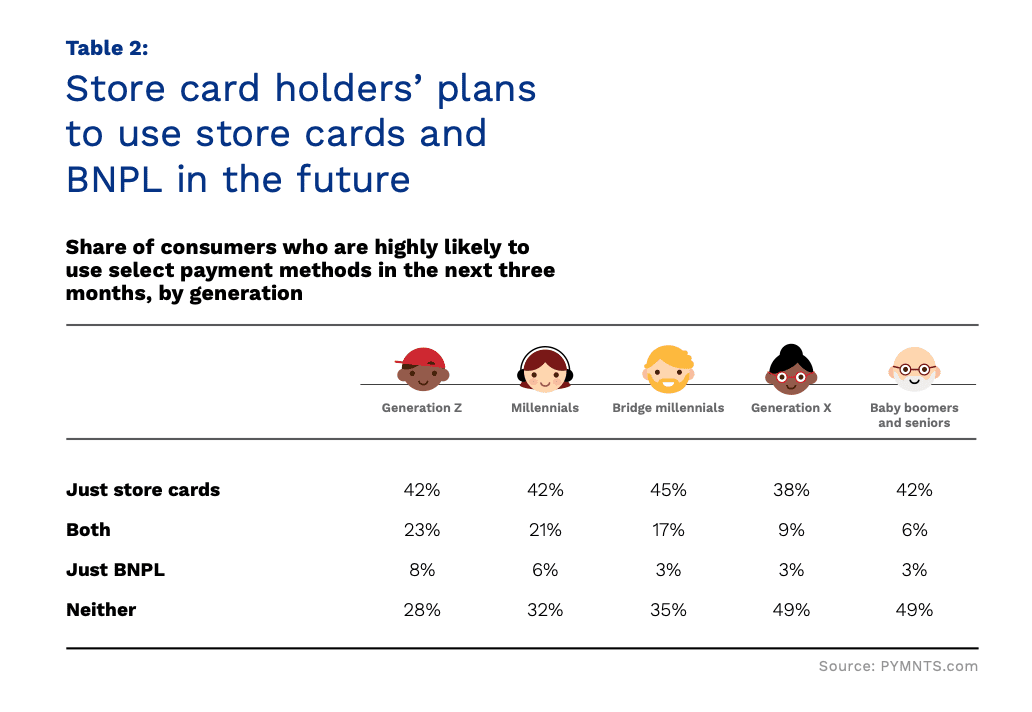

The millennial demos are less likely than Gen X or baby boomers to have a store card in the first place, with research finding 26% of both millennials and older bridge millennials have store cards. And they are more likely to be using BNPL for purchases.

Per the report, “Millennials are the most likely of all generations to have used BNPL at these merchants, as 46% have done so. This contrasts with baby boomers and seniors, of whom just 37% have ever used BNPL at merchants with which they held store cards.”

Additionally, we found that millennials and Gen Z are more likely to turn to BNPL more going forward, with 6% of millennials reporting they will “pay exclusively using BNPL within the next three months, and 21% plan to pay using a mix of BNPL and store cards within the same time frame. Among Gen Z, 8% and 23% expect to pay with BNPL and a mix, respectively.”

It’s the 6% figure that store card programs will want to watch most closely as it represents millennials who appear to be thinking about abandoning traditional credit use for BNPL.

By comparison, the number of consumers in all demographic groups intending to use BNPL exclusively in the coming three months stands at 4%.

The Upside of Options

An important takeaway from the study is not that stores with card programs should shun BNPL, but rather the opposite, as payments choice is a decisive factor among millennial consumers.

Our research concludes that 41 million consumers in the U.S. want to pay using BNPL, and merchants are wise to include it at the point-of-sale because it’s better to make the sale using installments than risk losing a sale — and a customer — from absence of choice at checkout.

“While consumers might not always want to use BNPL options when store cards are available,” the study states, “adopting BNPL options can help retailers convert millions more in sales than they would without BNPL plans,” and those sales will likely skew toward millennial shoppers.

Get the study: The Truth About BNPL And Store Cards Report

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More