As more consumers try buy now pay later (BNPL) and like it, the paradox of choice is becoming an issue as numerous third-party providers and major payments brands pile into the space.

Who should consumers pick? Spin the wheel at checkout, as it were, and try a new option from a FinTech? Use a familiar payment method? Yes to all — and put banks high on that list as well.

This Millennial Minute examines how more members of younger demographic groups with serious buying power and an attraction to installments see their bank as a top BNPL choice.

The study “BNPL, Banks And The Trust Factor: How FIs Can Gain A Competitive Edge In A Growing Market”, a PYMNTS and Amount collaboration, was based on a survey of nearly 2,240 U.S. consumers and analyzes this trend.

Trust at the Center

Look behind the awesome apps and digital wonderment, and the invisible force driving commerce is age-old trust, especially in matters of extending or accepting credit.

Underpinning all finance is the fundamental human idea of trust — who we should “bank on,” as the saying goes — and daring younger demographics who were first into apps and made FinTechs what they are today show a somewhat surprising predilection for BNPL from banks.

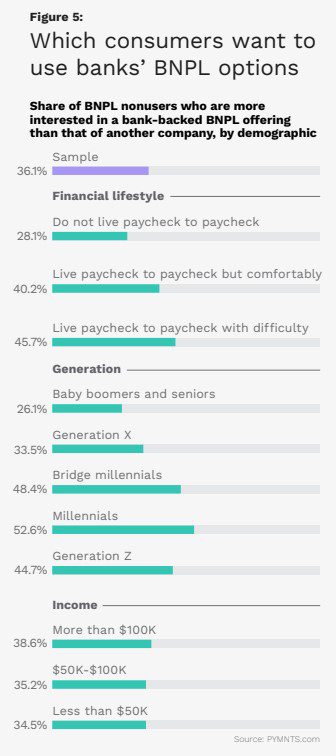

Per the study, “60% of millennial, 57% of bridge millennial and 54% of Generation Z consumers all say they would be more interested in a bank-backed BNPL option than one from a FinTech,” pointing to the opportunity banks have in BNPL as these demographics enter peak earning years.

As 52% of consumers overall are interested in using BNPL options, and 65% of those already using BNPL are using it more now than a year ago with inflation squeezing household budgets, banks face optimal timing to leverage the trust of young high earners into BNPL.

Giving a sense of the business opportunity for banks — and the service opportunity for their account holders — PYMNTS found that 77% of bridge millennial BNPL users, 75% of millennial BNPL users and 64% of Generation Z BNPL users used or increased BNPL usage over the past year.

Benefits of Bank-Issued BNPL

Younger digital-first and digital native demographics are thinking about banks as their best BNPL option because of trust, but they also consider factors from convenience to security.

PYMNTS research found that bank-sponsored BNPL offerings are perceived as easier to use and being more dialed-in to the user’s whole financial situation, with 41% saying they want BNPL credit issued by banks to help them manage and keep track of their spending.

Additionally, notable shares of consumers also believe bank-offered BNPL solutions are appealing for the following reasons: 34% cite better data security, 32% say credit approvals are faster, and 32% said it helps build credit scores. That last one is key for younger users.

Among the most tantalizing of potential bank-issued BNPL users are high-earning millennials and bridge millennials who haven’t used installment credit at all yet.

According to the study, “Interest in bank-issued BNPL plans is high among younger generations of consumers who are not BNPL users, including 53% of millennials, 48% of bridge millennials and 45% of Generation Z consumers who say they are interested in using bank-issued BNPL plans.”

Get the study: BNPL, Banks And The Trust Factor: How FIs Can Gain A Competitive Edge In A Growing Market