In recent weeks and months, joint research between PYMNTS and Sezzle has underscored the embrace of buy now, pay later (BNPL) at the point of checkout.

In the report “The Credit Accessibility Series: BNPL’s Wide-Ranging Impact on Consumers and Merchants,” we found that more than 40% of the 3,000+ consumers we surveyed said that they’d delay a purchase — or opt for a cheaper substitute — if BNPL were not offered.

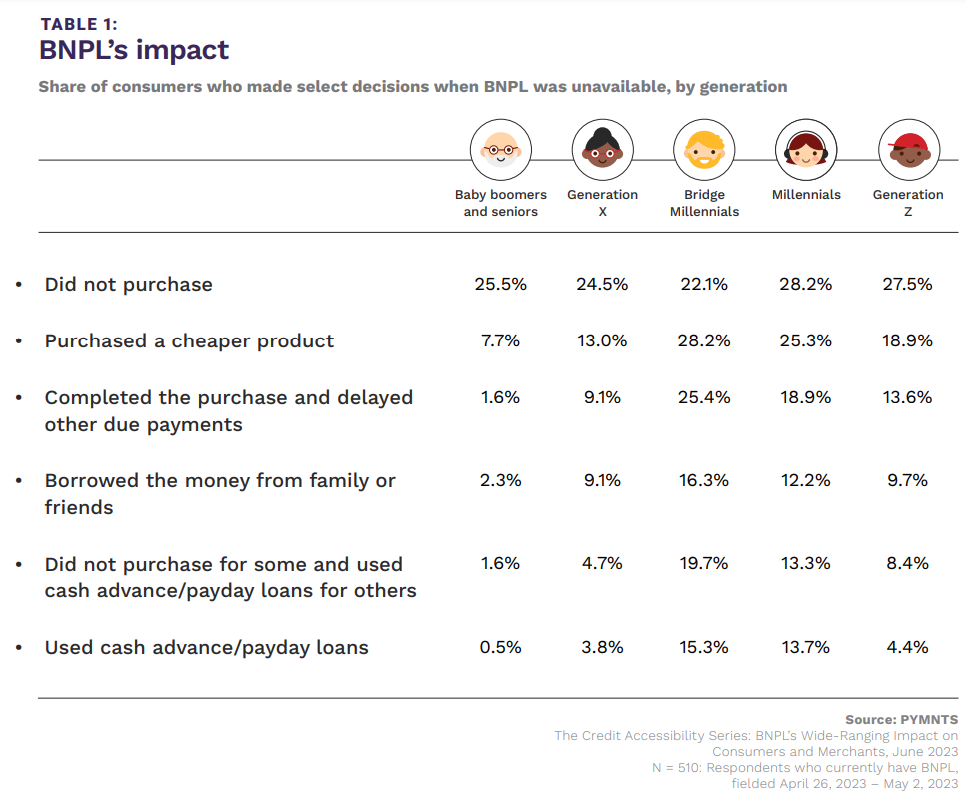

And as the chart below shows, the impact to merchants’ fortunes if not offering BNPL has been tangible: More than a quarter of respondents simply did not buy the item or service under consideration at all.

Recent data points gleaned from the midst of earnings season bears out the fact that BNPL is one of the factors that incentivize consumers to pull the trigger.

In one recent example, Affirm’s earnings showed that transactions per active account were growing in the double digits. And some key categories within consumer spending showed category volume growth that was in the double digits, too. Fashion and beauty volumes were up 14% year on year as measured in the June quarter, and general merchandise was up 61%, as measured in volumes over the same period.

BNPL’s Use in Credit Scoring

Sezzle’s most recent business update this past week, detailing July and August activity, shows that underlying merchant sales are up more than 15% in August to date versus the prior comparable period in July.

BNPL is also cementing a more visible role in helping consumers build credit.

During the call with analysts, Affirm CEO Max Levchin noted that “credit reporting is a really important piece of the puzzle” and revealed on the call to discuss the March quarter’s results that the company is working with FICO to build a credit-scoring model.

Sezzle, for its part, has been expanding the availability of its credit building service, Sezzle Up. As noted here, the company has brought the service to Canada, having already made it available in the United States. Sezzle Up lets users report their payment behavior to credit reporting agencies, which in turn helps them build credit.

In separate PYMNTS/Sezzle research, we found that 29% of consumers with credit scores of 650 or less have used a credit-builder app in the past year.

The data also shows that deep subprime consumers — those with credit scores of 579 or less — can enjoy significant financial advantage by boosting their credit scores. Hypothetically speaking, if these subprime consumers raise credit scores to near prime levels, they could increase their borrowing capacity by 68% of their income. Doing so allows them to finance an additional $44,000 worth of purchases.