In a credit-based economy such as that of the United States, credit scores determine more than whether consumers qualify for a mortgage or auto loan. Often, access to credit can also decide whether or not consumers can afford everyday essentials. Credit access is critical, yet PYMNTS’ data reveals that few consumers with low credit scores know how to improve their credit status.

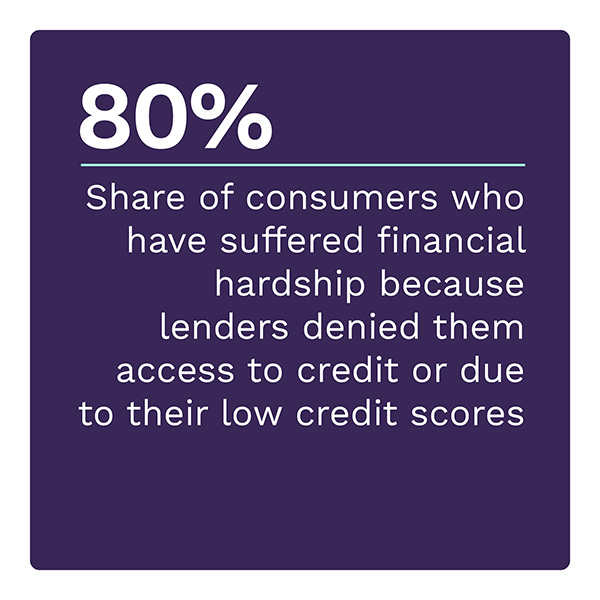

Consumers with low credit scores are roughly twice as likely as the average consumer to experience issues that impact their finances and daily lives. Our survey found that 27% of U.S. consumers have a score of 650 or less, which our study considers to be a low score, while 14% have deep subprime scores of 579 or lower.

This is one of the key findings in “The Credit Accessibility Series: BNPL’s Wide-Ranging Impact on Consumers and Merchants,” a PYMNTS and Sezzle collaboration. This report is based on a survey of 3,177 U.S. consumers conducted from April 26 to May 2. It assesses the rising popularity of buy now, pay later (BNPL) as a credit option, examines consumers’ reasons for using it and explores the potential of BNPL to improve their credit profiles.

More key findings from the study include the following:

Deep subprime consumers can alleviate their financial woes by improving their credit scores.

Helping low-credit and deep subprime consumers improve their credit scores can allow them the opportunity to escape from high-interest-rate loans and help raise their living standards. According to our analysis, if deep subprime consumers — those with credit scores of 579 or less — raise their credit scores to near prime levels, they could increase their borrowing capacity by 68% of their income. Doing so allows them to finance an additional $44,000 worth of purchases.

To improve their scores or increase their credit amount, consumers often turn to credit builder apps and BNPL.

Improving credit drives consumers with low scores to act so they can afford essentials and access additional credit products. We found that 29% of consumers with credit scores of 650 or less have used a credit-builder app in the past year. Seventeen percent did so primarily for credit-building purposes. They are also significantly more likely than those with high scores to use BNPL loans to raise scores, since BNPL plans do not affect credit reports. Ultimately, when it comes to boosting scores, it seems that desire is not the issue for consumers.

The higher the dissatisfaction with their credit score, the more likely a consumer is to take steps to improve it.

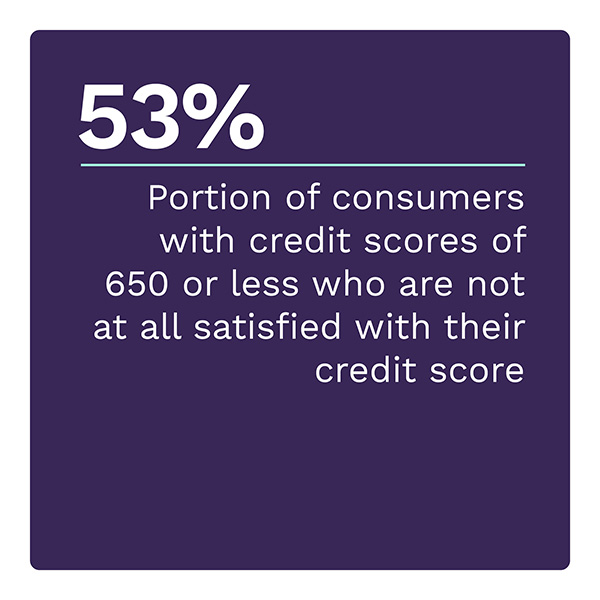

Consumers with credit scores of 650 or less are mostly dissatisfied with their scores and are willing to take steps to improve their credit status. Just 4 in 10 consumers with low credit scores were very or extremely interested in using user-friendly options, however, which may suggest a link between consumer credit scores and their knowledge of how credit works. The challenge faced by vendors of BNPL loans and credit-builder products is to find ways in which low credit score consumers can learn about their product’s ability to improve credit scores.

Our research shows a knowledge gap presents a challenge for the financial services industry, which would like more consumers to qualify for their products. Providers will need to develop innovative ways to educate the credit insecure. Download the report to learn more about how low-credit consumers can utilize BNPL to improve their financial health.