There’s no shortage of intriguing and successful players in the burgeoning buy now, pay later (BNPL) market. Afterpay, Affirm, PayPal and Klarna are just a few of them. But in the country where the BNPL model first caught fire — Australia — a new banking competitor and a series of new regulations have disrupted what was already a competitive market.

As of Wednesday (March 17), the Commonwealth Bank of Australia (CBA) has marked itself as the first bank to directly challenge Afterpay and others with a promise of lower fees on lending products. The CBA launch is planned for mid-2021, according to Reuters reports, coinciding with the entry of PayPal into an Australian market where BNPL regulation is thin and adoption is high.

Like Afterpay, the CBA BNPL product offers consumers an option to pay back a purchase in four installments on purchases up to a $1,000 limit. Unlike many BNPL pureplays, however, CBA said it would charge stores only the “standard merchant fees” that it does for credit cards to use its BNPL provider — unlike the roughly 4 percent merchant fees players like Afterpay typically charge.

“The CBA product is cheaper for merchants, however merchants are willing to accept higher fees from Afterpay as recompense for the referral traffic it drives,” said Lachlan Hughes, CEO of Swell Investment Management, which does not hold shares in CBA or Afterpay.

Instead of interest, CBA plans to make money by charging late fees. The Australian Securities and Investments Commission (ASIC) indicates those fees are a growing potential revenue stream as BNPL late fees in Australia industry-wide grew 38 percent to $43 million in the previous financial year. That model — harvesting late fees from credit card companies and banks — is the antithesis of one of the fundamental tenets of the BNPL companies. They don’t charge late fees. In fact, in an open letter to the industry published at the beginning of the pandemic, Affirm CEO Max Levchin challenged the entire financial services business to drop them.

“The primary way we support consumers is by lending responsibly. We do this by making smart, ongoing adjustments to our credit models that enable people to spend in a way that’s responsible and wise,” Levchin wrote. “In addition, we are steadfastly committed to our policies against late fees and unexpected interest. We make no extra money when consumers pay late, and we show them on day one exactly what they’ll owe — an amount that never goes up. It is our view that no lender, or business, should seek to profit from their consumers’ misfortunes, especially now.”

And CBA isn’t the only moth drawn to the flame of the Australian BNPL market. The bank’s announcement follows an announcement by PayPal a little over a week ago that it will be expanding its installment product to Australia starting this June. PayPal’s installment offering is already online in the U.S., the U.K. and France.

Andrew Toon, general manager of payments at PayPal Australia, told Reuters the expansion was largely motivated by demand from both businesses and consumers in the nation as soon as the first iterations of the service started launching last year. Toon also told Reuters the firm would not attempt to muscle out other BNPL providers by seeking exclusive arrangement with their merchants. Investors, however, aren’t so sure that PayPal presence won’t do more to cannibalize the existing market than really expand it.

Regulation

Banks and PayPal would be enough to rock any market. But the market has also been stirred by news that the country is becoming the first market to implement industry standards for BNPL players to keep the market safe for potential users, according to reports. In effect since early March, the new rules place nine requirements on BNPL lenders that include things like caps on the number of late payments a person can accrue, and mandatory financial checks before purchasing.

Australian Finance Industry Association (AIFA, which drafted the new code for BNPL players) Chief Executive Diane Tate said the code would simultaneously protect consumers and allow the emerging sector to flourish.

“The growth and diversity of the products and services enhances consumer choice,” Tate said. “It brings to life the concept that innovation and competition are for the everyday person and that this can be achieved while codifying strong consumer protections.”

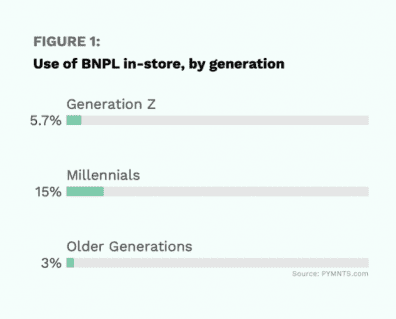

And competition and new regulation to the side, the industry keeps picking up strength in Australia and around the world, a fact confirmed by a quick glance at the March edition of the PYMNTS BNPL Tracker. Consumers, particularly Generation Z and millennial consumers, like BNPL so much that its availability is starting to determine where shoppers will and will not transact. In the U.S., for example Gen Z’s spending with the payment plans rose 201 percent year over year in 2020 while millennials’ grew 86 percent. When asked, over a quarter of millennials (26 percent) reported having used a BNPL tool on their last purchase.

Moreover, as new players are entering the market, incumbents like Afterpay are also working overtime to expand their reach. In late February, for example, Afterpay announced a new partnership with Stripe that gives Stripe merchants the option to offer Afterpay’s BNPL services via an “easy and seamless integration.”

Noah Pepper, Stripe’s business lead for APAC, said the goal is to “make it easy and fast for online businesses to offer their customers buy now, pay later. We’ve seen strong demand from users around the world for flexible payment options, and this partnership gives businesses on Stripe an effective tool for capturing more sales and reaching new customers.”

In a recent conversation with Karen Webster, Afterpay Co-Founder Nick Molnar noted that though competition in the BNPL field is growing, the range of fields where such installment based payment services can and should be offered is also growing. For example, the firm has already seen BNPL branch out into health and medical services like dentistry in its home market of Australia. Given the pressing need in the U.S., Molnar thinks it is reasonable to expect a similar path.

“I think consumers should be able to get the healthcare they deserve and desire — not the healthcare that they can afford on that particular day because their pay is coming in a few days or whatever it might be,” he said. “To have the ability to be the bridge without any subsequent debt trap, to empower a customer to engage in the healthcare they truly want — it’s a really privileged position to be in.”

A privileged position, perhaps, but also a very busy one. Because BNPL is a growing business around the world, and in Australia all of a sudden everyone is looking to snag their piece of it.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More