In “The Credit Economy: How Younger Consumers Make Credit Decisions,” PYMNTS examined credit-related behaviors and attitudes based on a survey of nearly 3,400 consumers across generations to understand the driving force behind their interest in using credit cards and buy now, pay later (BNPL) for everyday and occasional purchases.

Findings captured in the report showed that a significant portion of consumers rely on credit, with 55% of cardholders carrying monthly balances on their credit cards. Baby boomers and seniors are the most likely to pay their credit card balances in full, but only 50% do so every month.

In contrast, at least 4 in 10 millennials and Generation Z consumers pay their credit card balances in full each month, indicating a higher proportion of these cardholders revolving balances. This means that 38% of all cardholders have installment repayments pending on their credit cards, with 59% of millennials and 45% of Gen Z consumers falling into this category.

Additionally, while credit cards remain dominant, BNPL options have gained popularity due to their easy access to credit and flexible payment plans beyond the traditional 30-day schedule, which appeals to many consumers.

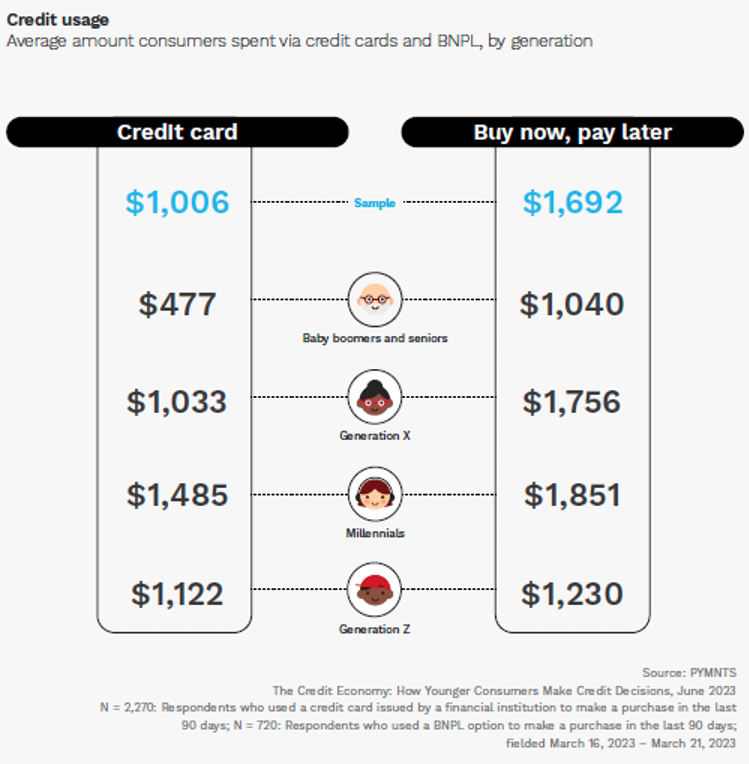

In terms of BNPL use across demographics, consumers spent an average of $1,692 via BNPL and $1,006 via credit card. Among millennials and Gen Z consumers, the prime demographics for BNPL, the dollar value of BNPL purchases was higher than those made with credit cards, with millennials spending $1,851 via BNPL and $1,485 via credit card, while Gen Z consumers spent $1,230 via BNPL and $1,112 via credit card.

As the study noted, Gen Z consumers primarily use BNPL for practical, smaller purchases, such as clothing, which accounted for 39% of BNPL use among Gen Z consumers, followed by groceries and restaurant purchases. On the other hand, baby boomers and seniors are more likely to use BNPL for big-ticket items, such as furniture purchases.

Credit alternatives such as BNPL are gaining traction among consumers, particularly millennials and Gen Zers. While credit cards still dominate the credit product market, the average amount consumers spend via BNPL is higher than credit card purchases, indicating a preference for using BNPL for larger transactions.