Three-quarters of Main Street businesses say they would close within 60 days of a cash crunch.

Consumer spending may be up, but so are prices, forcing consumers to struggle to pay more for the same item — or in the case of shrinkflation, less of an item than before. While megaretailers such as Walmart or huge grocery chains such as Kroger may often be able to absorb some of these increased supplier costs without raising prices for consumers, small-to-medium-sized businesses (SMBs) are faced with tougher choices. After all, deciding to absorb higher supplier and shipping costs (or not to absorb them) could be the difference between survival or a quick closing for a small business.

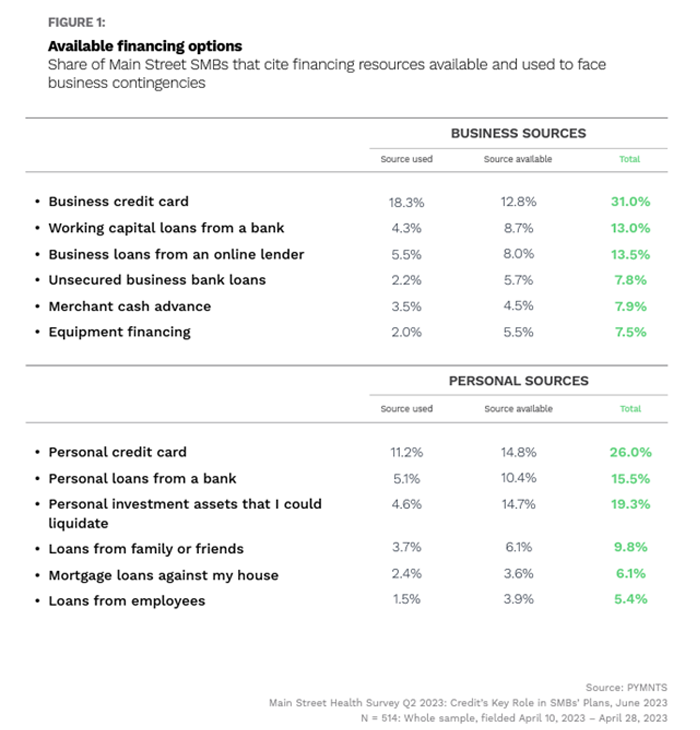

Walking this financial tightrope has led some SMBs to experience revenue shortfalls as they attempt to balance absorbing the least cost possible while retaining their customer base. When they do hit a cash crunch, SMBs, like businesses of all sizes, generally turn to credit, at rates reflected in the below chart created for “Main Street Health Survey Q2 2023,” a PYMNTS collaboration with Enigma.

The majority of SMBs surveyed have used business financing sources to face past cash flow contingencies. The top source to help these businesses through a rough patch was business credit cards, with 13% of SMBs turning to the resource, followed by the 9% of SMBs who relied on working capital from loans instead.

While this credit use may be expected in tough periods, 38% of SMBs have relied on personal sources, possibly due to challenges that could include lack of collateral or short length of establishment. Personal resources used in the event of these business contingencies include personal credit cards for 11% of SMBs, personal banks loans for 5% and loans against over 2% of SMB personal mortgages. Although these percentages are low, the stakes for the SMBs that fail to make payments on these personal loans can be extremely high.

For the 17% of small businesses with no cash access, relying on personal credit may become a lifeline. However, as credit options shrink daily while the Fed continues to raise interest rates, cash-strapped SMBs may want to deeply consider what comes with signing that dotted line.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More