As is often the case, but especially during troubled economic times, a fair amount of borrowing to meet expenses goes on.

In New Reality Check: The Paycheck-to-Paycheck Report — The Household Finances Deep Dive Edition, a PYMNTS and LendingClub collaboration, a survey of more than 4,600 U.S. consumers reveals that while a full-blown recession has yet to materialize, many Americans are nonetheless struggling.

Per the study, “Members of Gen Z, at 52%, are the most likely to have received such financial support over the last year, followed by 51% of consumers who live with their parents or siblings. We found that 47% of those living with friends or housemates received financial support from a household member. Urban dwellers and consumers living paycheck to paycheck with issues paying their bills, at 44% each, are also more likely than average to have received such financial support.”

Per the study, “Members of Gen Z, at 52%, are the most likely to have received such financial support over the last year, followed by 51% of consumers who live with their parents or siblings. We found that 47% of those living with friends or housemates received financial support from a household member. Urban dwellers and consumers living paycheck to paycheck with issues paying their bills, at 44% each, are also more likely than average to have received such financial support.”

Per the study, “Members of Gen Z, at 52%, are the most likely to have received such financial support over the last year, followed by 51% of consumers who live with their parents or siblings. We found that 47% of those living with friends or housemates received financial support from a household member. Urban dwellers and consumers living paycheck to paycheck with issues paying their bills, at 44% each, are also more likely than average to have received such financial support.”

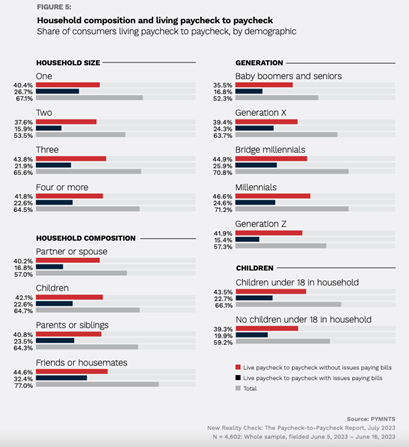

Living with others or alone, plus one’s stage of life, end up being decisive factors in our financial footing, explaining much about the different strata of those living paycheck to paycheck — or not — and how they’re managing financially in 2023.

The housing market meltdown of 2008 reconfigured how millions of Americans live, forcing adult children back to the family homes they grew up in, sometimes with spouses and kids in tow. It’s now 15 years since that systemic shock, and now a pandemic followed by economic disruptions has reenergized multigenerational households with new twists.

The housing market meltdown of 2008 reconfigured how millions of Americans live, forcing adult children back to the family homes they grew up in, sometimes with spouses and kids in tow. It’s now 15 years since that systemic shock, and now a pandemic followed by economic disruptions has reenergized multigenerational households with new twists.

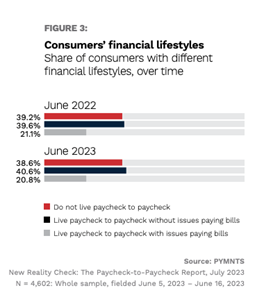

Standout findings include that in June 2023, 61% of U.S. consumers lived paycheck to paycheck, and 21% struggled to meet expenses. Both figures are unchanged from June 2022. It’s a situation where not being worse off than we expected begins to look like winning.

Household composition of earners versus non-earners, like younger children and older adults living with working parents, as well as lifestyle choices within homes of any makeup, are among the chief factors deciding the financial health of households at a time when the economy itself remains pressured, though perhaps not to the degree forecast early this year.

Per the July report, the share of consumers living paycheck to paycheck without issues paying monthly bills grew by only 1 percentage point since last year to 41% in June 2023. It’s an indication that “consumers continue to adapt to inflationary pressures, finding ways to manage their spending and live within their means.”

As the latest data shows, one dependable way to manage spending is to live in pairs, ideally with two incomes. The study notes that consumers not living paycheck to paycheck “are most likely to reside in two-person households, at 41%. Meanwhile, 49% of millennials and 55% of bridge millennials live in households of four or more people, making them the age groups most likely to reside in the largest households. Urban dwellers also average somewhat larger households than suburban or rural consumers, with 39% living in households of four or more people.”

As the latest data shows, one dependable way to manage spending is to live in pairs, ideally with two incomes. The study notes that consumers not living paycheck to paycheck “are most likely to reside in two-person households, at 41%. Meanwhile, 49% of millennials and 55% of bridge millennials live in households of four or more people, making them the age groups most likely to reside in the largest households. Urban dwellers also average somewhat larger households than suburban or rural consumers, with 39% living in households of four or more people.”

Of those who live with family longer, 43% said they’re saving money and 30% lack the means to afford housing. Along with economic reasons, “consumers remain at home to maintain family ties (24%), for transitional reasons (23%) and to provide care (22%).”

While those living alone carry lower credit card balances than any other group, they tend to pay more for housing, and with no one to help bear financial burdens, including routine household expenses and utilities, living alone generally means struggling between paychecks.

“Those not living paycheck to paycheck are the most likely to live with a partner or spouse,” the study states. “By contrast, consumers who reside with dependent children are more likely to struggle financially. This can be attributed to an increase in the ratio of income earners to members of the household, resulting in a higher likelihood of financial distress.”

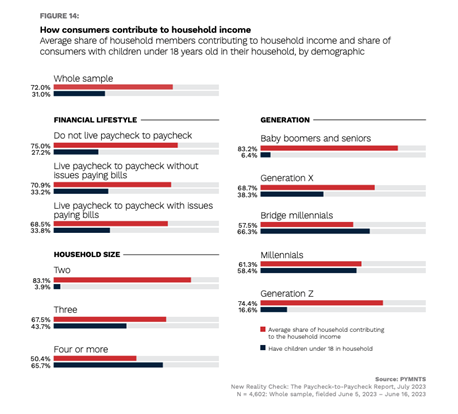

Among respondents, 80% of those living with children under 18 report outstanding credit card balances, and those living with children under 18 average outstanding credit card balances that are 50% above those of consumers who live alone.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More