An increasing number of Americans are moving towards relying on FinTech services to improve their financial well-being, research has found.

With as many as 60 percent of Americans showing willingness to improve their lack of financial stability, more of them are relying on technology to help them reach their goals. Of the surveyed base, 65 percent said they were currently using some form of technology, such as an app, to gain a tighter grip over their finances.

“Our research is consistent with our impression of the financial well-being of the average American: While our national economy may have pulled out of the depths of the recession, the after-effects are still being felt, with many Americans still struggling to get ahead financially,” said Aaron Vermut, CEO of Prosper Marketplace, the San Francisco-based company that conducted the research.

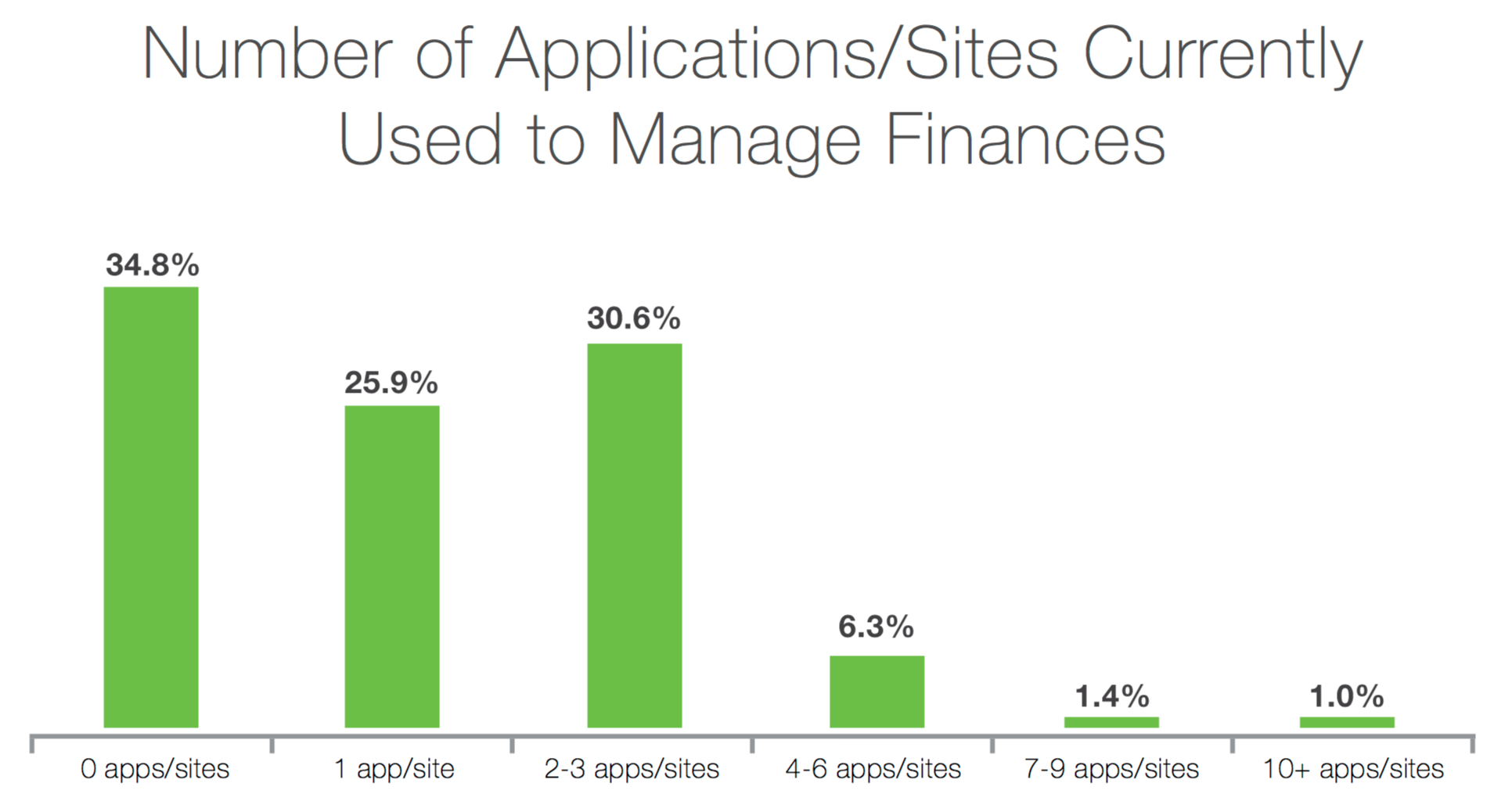

Of the surveyed base of 1,000, most reportedly stated using one to three applications to analyze and keep up with their finances a few times a week. The survey also found a shift in user behavior, with 18 percent of users who have not previously used financial mobile apps or websites saying they were planning to do so, according to the research. A growing number of participants also reported using personal financial management tools, such as BillGuard (29 percent) and marketplace lending services like Prosper (16 percent).

“With the current economic volatility, the power of having a clear plan in place — whether that be consolidating debt at a lower, fixed rate, cutting expenses or creating a better strategy for saving — is instrumental in helping people feel in control of their finances,” Vermut added.