A good game, one that attracts hundreds of millions of players and dollars in the app store, can take all kinds of forms. There are complicated adventures, simple puzzles, first-person shooters and even music lessons. And although it’s not exactly attracting Candy Crush numbers, new games are starting to pop up in the financial services category.

Which makes complete sense to Charlie CEO Ilian Georgiev, whose company has created a new app that gamifies financial wellness. He told PYMNTS that every good game will have three things in common: They all have clear goals, clear paths to attain those goals and offer escalating levels of positive reinforcement every time the player completes one of those goals.

And those three elements used in combination work so well, he said, that consumers spend hundreds of hours and tens of billions of dollars interacting with virtual worlds. And they do so because they create an environment that very successfully draws consumers in and keeps them there with a very effective and efficient positive feedback loop.

It’s a loop that Georgiev has spent a lot of time thinking about, as he worked bringing games to market in his pre-financial services career. And it’s a loop that he noticed is almost absent from financial services, particularly when it comes to putting one’s financial house in order. The good experience one has in a virtual world inverts nearly entirely when consumers manage their finances in the real world.

“Most people, they’re phenomenally worried about their debt,” Georgiev told PYMNTS. “The number one thing they want is to figure out their personal finances, but they’re struggling and failing. Why is that happening? Because the interaction of paying off debt is missing those three elements. People don’t have an achievable goal or they don’t know how to think about their goal. The action of them moving towards that goal is very complicated or very painful. And lastly, even when you are making progress, you don’t get a thank you from anyone: not from your bank, not from anybody around.”

But Charlie, using the techniques of gamification, he said, can step in and start to fix this problem — by offering consumers a financial wellness plan designed to be actually attainable.

Keeping Consumers On Their Financial Diet

Financial responsibility can be a lot like dieting, Georgiev told PYMNTS, in that loading too many onerous changes and responsibilities onto the front end in to radically change one’s habits — spending or eating — overnight. The process becomes so painful and unpleasant that attaining the goal doesn’t seem worth the suffering.

“The reason why they’re not engaging in the right behavior here is because they’re paralyzed by the prospect of doing it, the feeling like this is unachievable. They don’t need another voice telling them they are messing up,” Georgiev said.

What they need is a voice telling them what to do, in a way that seems manageable. Charlie attains that by simply ascertaining the consumer’s financial picture as they come in. It aggregates and analyzes where their debt is, how much they are paying, what their spending habits look like and what is their overall financial picture. On average, he said, their customers come in with about $80,000 in debt split between credit cards and personal loans making a lot of minimum payments every month.

“We can show what that means, and so for example we can show them information like at the rate you’re going right now, you’re going to be debt-free in 40 years. And you’re going to pay $80,000 of interest. For most users, [it’s] like the moment [of truth], because they’ve never seen the math,” Georgiev said.

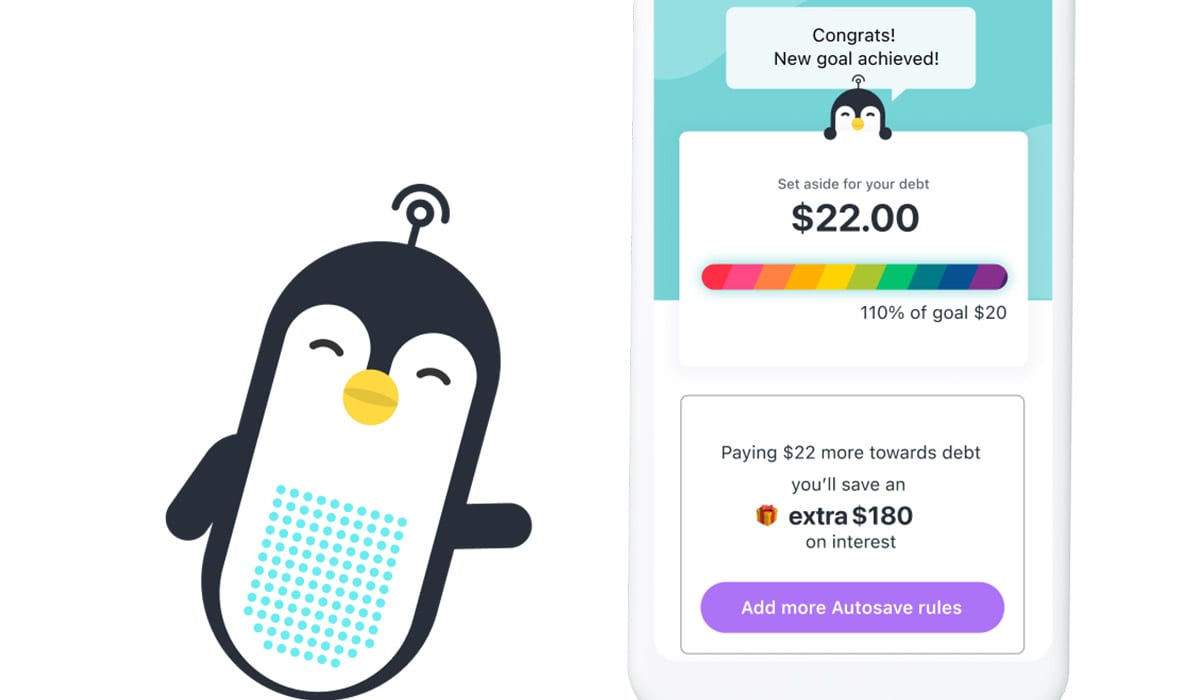

And from that “wow moment” Charlie then makes suggestions about how they can take on that debt in ways that are highly manageable — like paying an additional $25 a month. The complicated math will show them that even those small adjustments can cut the time and the interest they will pay in half, and thus make it concretely clear why it’s worth doing.

But that is not enough, he said. The good game experience also guides users down the path to achieving those stated goals. It’s a thing Charlie does by letting users set rules that will turn their “bad” spending habits into good saving habits. Those rules could be linked to their spending. For example, every time they buy Starbucks, they donate a percentage of the purchase to paying down their debt. It might be one of the zany offerings that Charlie has built it — like an automatic savings contribution whenever certain events happen on The Bachelor. The point, he said, is to give the customer actual tools with which to reach the saving goals they’ve set so it doesn’t remain hypothetical or appear unattainable.

And, he said when they hit the goal — they are rewarded. Anytime Charlie detects a payment, confetti starts flying down the screen.

The Bigger Picture

The goal for Charlie over time, he said, is to build a different kind of bank for consumers who Silicon Valley often forgets. Their customer base is mostly female, mostly makes around $50,000 a year and isn’t what is generally considered a “tech-forward customer.” Their first customer was a mom from Minnesota trying to figure out how to save $400 to buy her daughter a birthday present. By contrast, their first customer from the Bay Area asked about Bitcoin trading options.

That world of left-out FinTech innovators and consumers needs a banking solution that is more proactively oriented toward helping them improve their financial situation over time, and Charlie’s goal is to build the tools that will let them do that. Later this year, he said, they will begin issuing their own debit card which they believe will greatly expand the range of their offering — in a world that greatly needs it.

“Our job as a product is to take consumer data, anonymize it and then figure out what it means for the user,” Georgiev said. “And to give them simple actionable things they can do next to achieve their goals.”