On the face of it, $1.7 trillion in “excess” personal savings is a lot of firepower — enough to keep consumer spending buoyant through, and well beyond, the holiday season.

But there’s a lopsided aspect as to just who holds that money, and the signals are there, in the data, and in earnings season commentary, that show the consumer, particularly the paycheck-to-paycheck consumer, may tighten the purse strings, perhaps dramatically, over the near term.

The Fed’s data late last month show that during the pandemic, U.S. households built up $2.3 trillion in savings through the pandemic and into the second half of 2021.

But since then, a quarter of that’s been spent, and the saving rate has dropped below pre-pandemic levels, and the tally now stands at $1.7 trillion. Within that latter figure we see a skew: Households in the top half of income distribution hold $1.3 trillion, or more than 75%, while households in the lower half of income hold about $350 billion, which had been padded by stimulus payments.

The Fed noted in its report that “excess savings may help to damp a feedback loop — where a negative shock to income leads to a cut to spending, which then leads to an additional cut to income, et cetera — that, at its worst, could lead to a recession. At the same time, excess savings have fueled high levels of spending for some households, which may have contributed to persistently high inflation amid constrained supply.”

Less Liquidity Is Available

And, as the Fed explained further, with emphasis on the lower income households, “it is important to note that many of these households have used some of their excess savings to pay down debts, or possibly to invest in equity and other financial assets or as a down payment for buying a home, instead of keeping them as liquid assets, thus shifting where the savings appear on their balance sheet.” In other words, they’ve drained some of the ready cash, and less of it sits in actual, accessible deposit accounts.

While the debt paydown has given households some breathing room, PYMNTS data show that amid the paycheck-to-paycheck reality that confronts more than 60% of us, P2P consumers are three times as likely to revolve credit card debt and carry higher monthly balances overall. Among cardholders living paycheck to paycheck, 34% of those without issues paying monthly bills and 47% of those who struggle to pay their bills “always” or “usually” have a revolving balance.

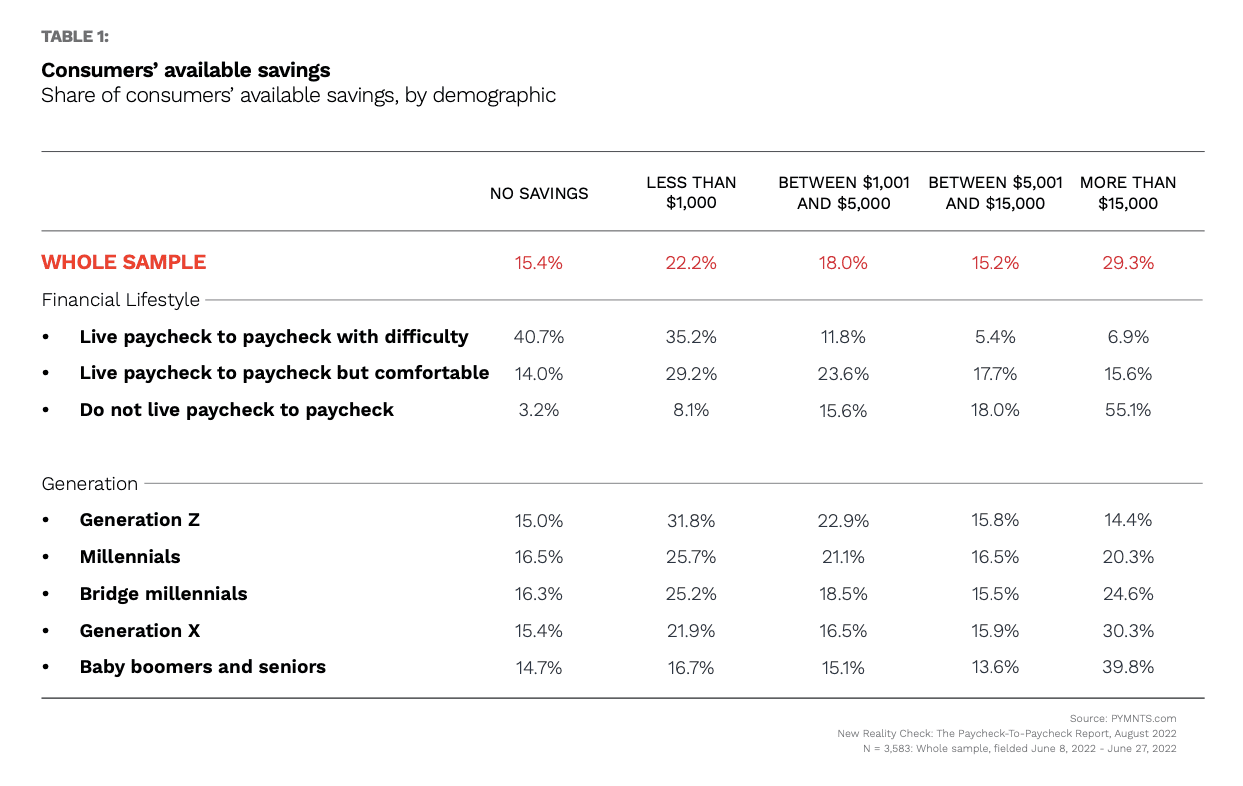

There’s evidence too, that with the ready cash available to help “stopgap” the divide between cash flow and monthly obligations is waning. Separate PYMNTS findings showed that for the paycheck-to-paycheck consumers struggling with expenses, the average stands at less than $3,000, down from more than $4,000. A significant percentage, as seen below — at more than a third — have no savings at all, or have less than $1,000.

The Fed’s report concludes that “In summary, our estimates suggest that households across the income distribution continue to have a buffer of excess savings to help them navigate higher prices and/or a tightening cycle. While this buffer is dwindling, for now it is likely still providing some needed balance sheet support that could help to stanch a negative feedback loop were the economy to slow.”

That italicized emphasis is ours. The “for now” is temporary. Commentary from this earnings season – which continues to roll on — points to the fact that it is the lower-to-mid income consumer that is pulling back on spending. In just a few recent examples, management at restaurant giants such as Yum, McDonald’s and Chipotle Mexican Grill have made those observations. With a relatively broader view of consumer spending, PayPal management has said the same thing. The holidays may not be as full of glad tidings — at least not for merchants — as might have been hoped.