Consumers are a resourceful lot and will do what they must to make ends meet, even if it means splitting up the weekly grocery bill into more manageable chunks.

PYMNTS Intelligence data shows that 40% of lower-income consumers have used split-pay plans in the last 12 months for everyday necessities like food or gasoline.

Lower-income consumers — those with annual earnings of less than $50,000 — share some characteristics that significantly impact their spending capacity and credit decisions, according to a PYMNTS Intelligence study done in collabotation with Sezzle. For instance, lower-income consumers have, on average, $78,000 in outstanding debt, and only 24% of these consumers are not living paycheck to paycheck. Thus, lower-income consumers tend to rely on credit cards and other payment methods to cover their daily expenses.

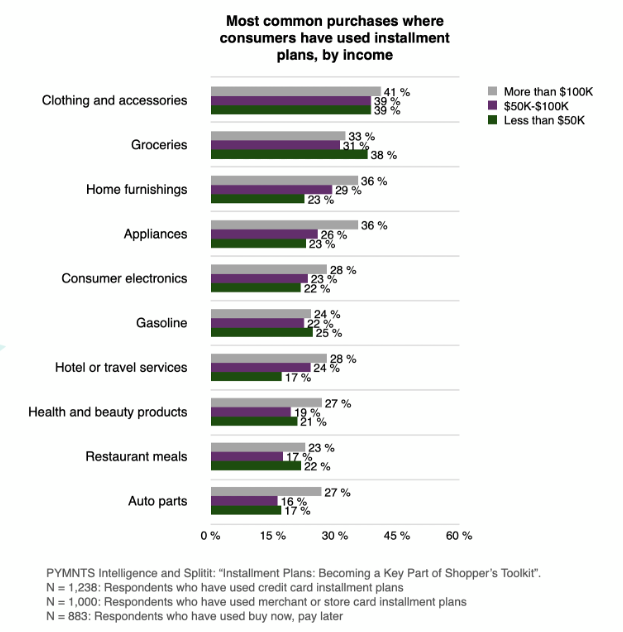

In this regard, more than half of lower-income consumers used split-pay installment methods in the last year, and a similar number plan to do it next year. What is noteworthy is that on many occasions they did so not for large purchases, such as home furnishing or appliances, but for everyday expenses. To give some illustrative numbers, 39% used it for buying groceries, 38% for clothing, and 25% for gasoline.

Lower-income consumers favor the use of debit cards and PayPal for their retail purchases, according to PYMNTS Intelligence research, as this method allows them to better control their spending and is free of transaction fees. This contrasts with the predominant usage of credit cards in their transactions by other middle-income and large-income segments, evidence of the clear divide in payment methods based on financial stability.

If debit cards are lower incomers’ first option for purchasing retail products, credit cards are their choice for holiday shopping or unexpected expenses, per PYMNTS Intelligence research. Credit cards are their preferred split-pay plans, at least for 38% of individuals from this segment, followed by BNPL at 35% and merchants or stores cards at 31%.

When using credit cards, the research notes, while 60% of high-income earners are non-revolvers, this proportion drops to 45% in the case of the lower-income segment, a disparity that highlights the different financial realities faced by individuals across the economic spectrum.

In conclusion, lower-income people prefer to pay by debit card or PayPal-type systems whenever they can afford it. However, when they do not have enough cash available to make ends meet, they often turn to split-pay purchases, sometimes even to pay for everyday expenses, such as clothing, food or gasoline. This occurs in a greater proportion than any other demographic cohorts, underlining the economic constraints lower-income earners often face.