Consumer credit card debt in the United States has surpassed the $1 trillion mark, leading to heightened concerns about credit insecurity among both consumers and providers.

Against that backdrop, many consumers grappling with high debt are more likely to face bankruptcy and be limited to high-interest loans, as noted in “The Credit Accessibility Series: Economic Malaise Exacerbating U.S. Consumer Debt Levels,” a PYMNTS Intelligence and Sezzle collaboration which explores how high levels of debt impact different consumers’ credit accessibility, livelihoods and purchasing power.

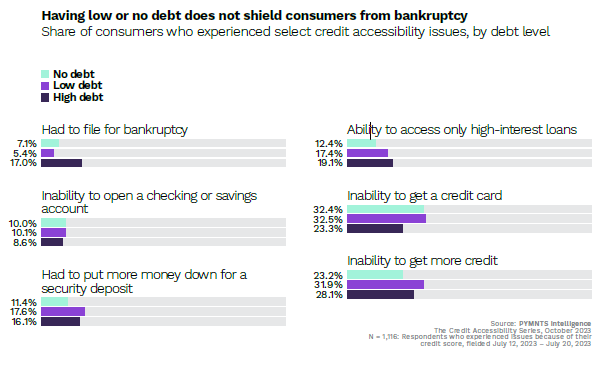

According to findings detailed in the study, consumers who faced credit accessibility issues due to high debt and overdrafts often found themselves in a precarious financial situation. These issues included damaged credit scores, challenges with interest payments, and the need to resort to more loans to cover debt repayment.

In some cases, consumers reported having to file for bankruptcy due to a lack of funds to cover overdraft fees. For instance, 17% of consumers with high debt had to file for bankruptcy and 19% of individuals in this category said they only had access to high-interest loans.

This aligns with data released by the Administrative Office of the U.S. Courts in July showing that personal bankruptcy filings in the country rose by 10% in the year ending in June, compared to the previous year.

As PYMNTS reported, this increase represented a total of 418,724 annual bankruptcy filings during the period. Of these filings, non-business bankruptcy cases rose by 9.5% to 403,000. The spike in bankruptcy filings is noteworthy, considering that filings have only rarely increased over any 12-month period since 2010.

As the country grapples with record-high consumer credit card debt, it is crucial to address these issues and provide support and resources to consumers facing financial hardships. Implementing financial education programs can empower consumers with the knowledge and tools to manage their debt effectively.

Additionally, promoting responsible borrowing practices can help individuals avoid falling into the cycle of high-interest loans and overdrafts. Exploring alternative financial solutions, such as credit-building apps, can also provide consumers with viable options to improve their financial standing.

In conclusion, the combination of high debt, credit score issues, and reliance on overdrafts has created a challenging financial landscape for many consumers. And the burden of overdraft fees, damaged credit scores, and limited credit accessibility has pushed some individuals to file for bankruptcy.

The rise in bankruptcy filings is a concerning trend that calls for proactive measures to support consumers and alleviate their financial hardships, while helping them rebuild their credit and avoid the pitfalls of bankruptcy.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More