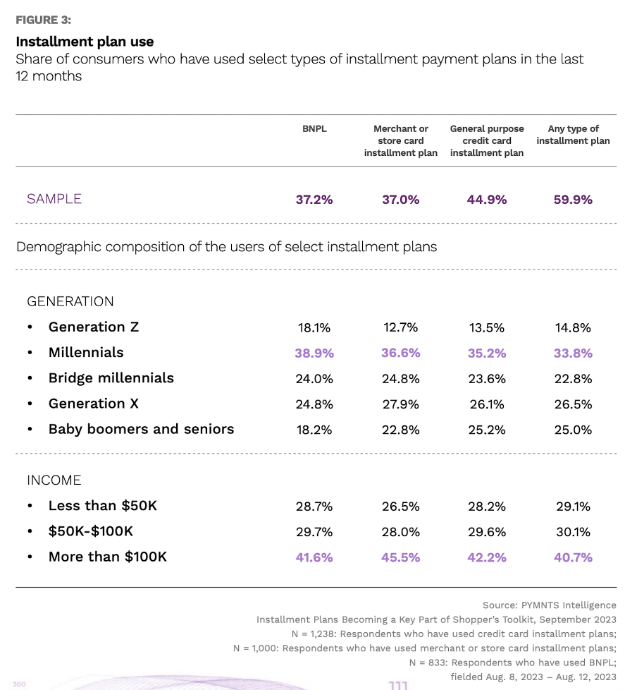

In recent years, split-pay options have gained popularity among consumers of all demographic groups looking for greater flexibility in managing their expenses. But it’s not millennial, Gen Z, or low-income consumers who are most likely to use these plans — it’s high-income consumers. This applies for all forms of split-pay options, including general-purpose plans from credit card issuers, those offered by merchants via store cards, and buy now pay later (BNPL) plans, although store card-based plans are preferred by these consumers. This fact challenges the assumption that high-income earners are averse to credit use.

These are some of the key conclusions drawn from “Installment Plans Becoming a Key Part of Shopper’s Toolkit,” a PYMNTS Intelligence research study done in collaboration with Splitit that examines how consumers use all types of split-pay plans.

According to the study, almost 46% of high-income earners — defined as those making more than $100,000 annually — have used store card installment plans in the last 12 months prior to being surveyed, on average using the plans twice during that period.

It seems that the high level of adoption among this consumer segment is not a coincidence but could be maintained over time, as 78% of consumers who have used a store card installment plan have been very satisfied with the experience, and 42% say that they are likely to use one in the next 12 months.

High-income consumers in particular tended to use this credit option for amounts above $2,000, which can be used either for the purchase of home furnishings, consumer electronics, or even hotel expenses, to cite a few examples.

The use of split-pay options by high-income earners is one trend reshaping consumer behavior, with the widespread adoption of installment purchase plans by this segment in particular presenting a business opportunity for merchants and credit card issuers. By adapting their offerings to meet consumer preferences, merchants and credit issuers can capitalize on this trend and expand their market presence even further. Fine-tuning their installment offerings to align with these priorities can help merchants build stronger brand credibility and foster customer loyalty.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More