Many people are resorting to credit cards to navigate difficult financial times, especially as the rising prices of goods and services continues to weigh on U.S. consumers’ wallets this holiday season.

In “The Credit Card Use Deep Dive Edition” of the “New Reality Check: The Paycheck-to-Paycheck Report,” PYMNTS Intelligence draws on insights gathered from a survey of over 3,250 U.S. consumers to examine their financial habits and assess their strategies in leveraging credit cards to navigate cash flow challenges and sustain their day-to-day expenses.

According to findings detailed in the report, a LendingClub collaboration, nearly 60% of consumers living paycheck to paycheck own credit cards, with 80% of these consumers owning two credit cards, on average.

The report also reveals that paycheck-to-paycheck consumers value certain features when choosing a credit card. Higher credit limits and split payment plans are particularly important to them, indicating that these individuals rely on credit cards as a financing option to manage their cash flows.

Additionally, financial distress often leads to a higher frequency of reaching credit card limits and carrying balances from month to month. Paycheck-to-paycheck consumers are more likely to experience these challenges, highlighting the importance of credit card management in their financial stability.

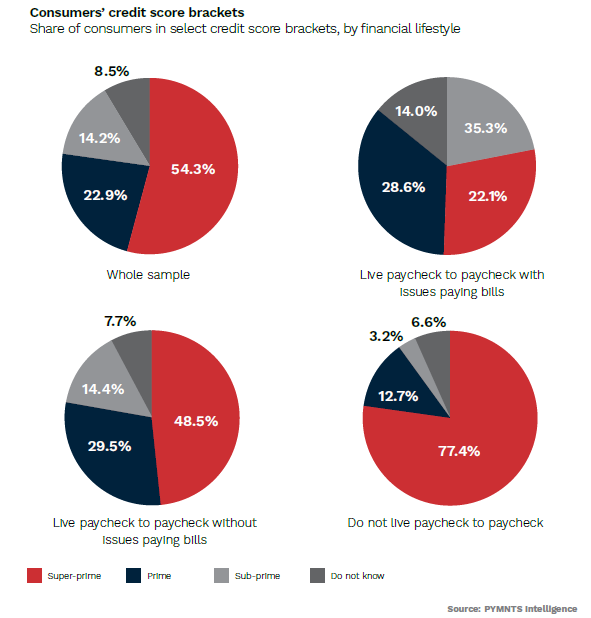

Examining the data further reveals that paycheck-to-paycheck consumers are slightly less likely to consider their credit scores important and check them as frequently as the average consumer. However, it is worth noting that living paycheck to paycheck doesn’t necessarily undermine one’s creditworthiness.

In fact, 40% of these consumers still have super-prime credit scores of 720 or higher, demonstrating their commitment to maintaining good credit despite their financial circumstances. Moreover, 49% of paycheck-to-paycheck consumers without issues paying bills boast of having these high credit scores. And even among those facing bill payment issues, 22% report maintaining scores of 720 and above.

This further suggests that these individuals are effectively managing their credit card usage to “stay creditworthy, with many successful at the task, even as those most struggling tend to find it more challenging,” the report noted.

In summary, it’s clear that paycheck-to-paycheck living doesn’t hinder individuals from achieving excellent credit scores. Consumers adeptly manage their credit card usage and financial obligations, maintaining strong credit standings despite financial constraints.

Recognizing the needs of financially distressed consumers, credit card providers should offer features that facilitate effective cash flow management. By doing so, these companies empower individuals facing financial challenges to navigate them while preserving their creditworthiness.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More