A confluence of factors is hurting large swaths of U.S. consumers with little to no access to credit, and a widespread lack of knowledge about how credit works is adding to the problem.

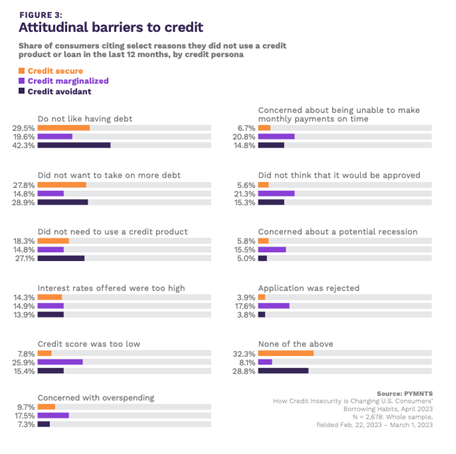

In the new study “How Credit Insecurity is Changing U.S. Consumers’ Borrowing Habits,” a PYMNTS and Sezzle collaboration, a key finding was that consumers along a continuum from credit secure to credit insecure to credit marginalized to those who shun credit (credit avoidant) don’t understand fundamentals of how to maintain or rebuild creditworthiness.

Showing how delicate creditworthiness can be, the study of nearly 2,700 consumers notes that for nearly 1 in 8 (79%) credit-insecure consumers who have been rejected by credit providers, “major life events such as a change in employment, illness or the death of a loved one have negatively impacted their finances in the past year.”

Discussing the matter with PYMNTS’ Karen Webster, Sezzle CEO Charlie Youakim said that’s “a huge part of the problem,” remarking how it dovetails with paycheck-to-paycheck living which impacts over 60% of U.S. consumers, as seen in other PYMNTS research.

“The data that’s shocking is how much of the population lives paycheck to paycheck,” Youakim said. “You have so much of the population living paycheck to paycheck, you probably tend to have a lot of overdraft fees, which hurt them. You have missed payments on credit products, which hurt them. Then you have life events that can completely derail them.”

It’s an important discussion, as the study found that dropping into credit-insecure status often drives consumers to pricey payday loans and the like, with 34% of credit-marginalized consumers reporting difficulty getting lines of credit after these life events, and 27% only qualifying for riskier loans in those cases.

When consumers can’t answer basic questions about credit scores and what goes into them, that lack of knowledge places attaining creditworthiness out of reach for many.

Looking at the fact, for example, that credit-insecure consumers scored one point above credit-secure consumers when answering 10 questions about credit scores and related behaviors, Youakim told Webster he was astounded by the lack of knowledge around this vital unlock to greater economic empowerment.

“I was shocked that the marginalized customer scored better on credit education than the credit secure,” he said. “It was slight, but if someone asked you about that ahead of the study, you’d imagine that the credit secure customer would be 70th percentile plus, and credit insecure would be a lot lower. But the fact that they both struggle with credit education questions — that blew me away.”

He called this “a big opportunity for all groups, for all citizens in the U.S.” to avail themselves of some credit education.

Social media could be helpful in this regard, in no small part because financial education is lacking in primary school curriculums. “I think there can be a lot done in education. If you can make it fun, interesting, put it on social media, give tips and tricks, I think that can go a long way,” he said.

With an estimated 100 million U.S. consumers having used a buy now, pay later (BNPL) product, the discussion led to more activity among the credit bureaus and scoring models to include BNPL borrowing and repayment activity as a new way of improving scores.

Youakim called his company’s Sezzle Up credit-building product “a home run” in the three years since its launch, adding that “one of the data points that sticks in my head … is that in four months we saw the average Sezzle Up customer raise their credit score by 20 points.”

Given what’s been done with Sezzle Up, he added that BNPL reporting could rise to the regulatory level, saying, “I think it comes down to, at this point, is it going to be a regulatory requirement with CFPB, etc. that mandates this [for BNPL providers]? Or are we going to see some of our competition or other players in the buy now, pay later space start to report?”

Another interesting finding from the study concerned the roughly 17 million consumers categorized as “credit avoidant” in that they neither use nor seek to use credit in any form.

Youakim said, “You could probably bifurcate that group into two groups. One is the doomsayers, and we’re probably never going to get them back. They’re just done with credit. But I think there is a group within that subset that got scared away because of credit card debt.”

He hopes that perhaps half of the credit avoidant could be brought back into the credit ecosystem with BNPL usage being reported to credit bureaus and seeing better scores resulting from that.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More