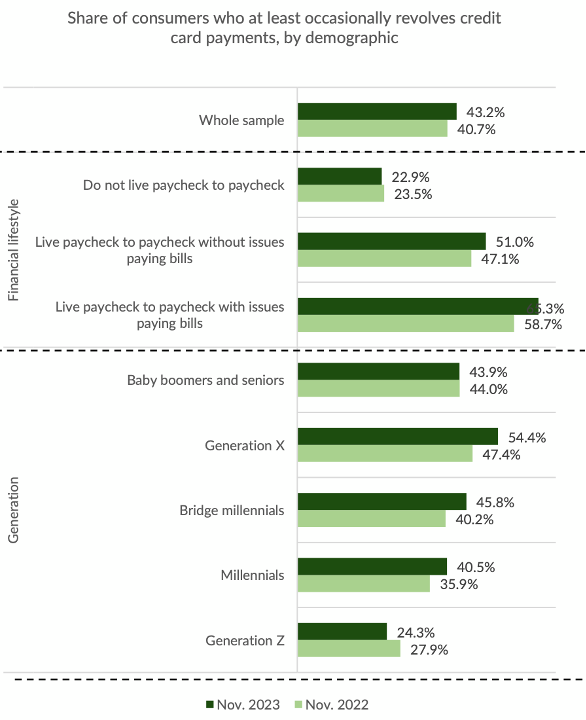

In times of financial hardship, revolving a credit card balance to future months rather than paying it off entirely is a strategy consumers commonly adopt. But despite the oft-held assumption that members of Generation X are more averse to credit use than other generations because of a generally healthier financial lifestyle, a greater share of these consumers turn to revolving their balance than any other generation. Specifically, 57% of consumers from this generation did it at least occasionally in the last year, according to PYMNTS Intelligence data.

This is just one key finding detailed in the most recent edition of “New Reality Check: The Paycheck-to-Paycheck Report,”a PYMNTS Intelligence and LendingClub collaboration. “The Credit Card Use Deep Dive Edition” examines the financial lifestyles of U.S. consumers and explores how they use credit cards to manage their cash flows and get by.

Gen Xers’ high propensity to revolve has been building, as the portion of Gen X consumers revolving their credit increased by 7 percentage points since November 2022, also leading all generations. In comparison, the corresponding share of millennial revolvers increased by 5 percentage points, and baby boomers and seniors remained equal.

During this time, persistent inflation amid wage stagnation impacted struggling consumers’ economy. In the case of Gen Xers, those with difficulties to make ends meet account for around 64% of this cohort. With such a large share of the population struggling financially, it follows that many of them would turn to credit products to stretch their budget.

The average credit limit for a Gen X consumer is nearly $10,200, the second highest of all generations and very close to the leading group, baby boomers and seniors. And nearly 1 in 3 have reached that limit at least occasionally in the last year; for comparison, 15% of baby boomers and seniors have done the same.

With high dependence on credit cards for living, financial hardship is typically associated with a higher utilization of installment or split payment plans. In the last year, Gen Xers paid for 3.6 products in installments on average, whereas baby boomers and seniors paid for just 2.2 on average in this way. Sixty-nine percent of consumers from this generation have made credit card installment payments in the last year, while 13% used some form of buy now, pay later (BNPL) scheme.

Whether opting for installment payment plans or revolving credit card balances, Generation X is heavily turning to credit products to better balance their finances. However, their relatively healthy financial position and high credit limit allows them to turn to this practice more often than other generations do.