If regulators approve the deal, it will bring together two of the largest U.S. credit card issuers, resulting in a global payments platform that includes 70 million merchant acceptance points and outreach into more than 200 countries and territories. Additionally, the acquisition would position Capital One alongside leading card companies Visa, Mastercard and American Express.

But it is not just Capital One and Discover shareholders that stand to benefit from the deal. As PYMNTS: wrote, “bringing the two credit card giants together would pave the path toward creating a banking giant with particular expertise in serving the paycheck-to-paycheck consumer.”

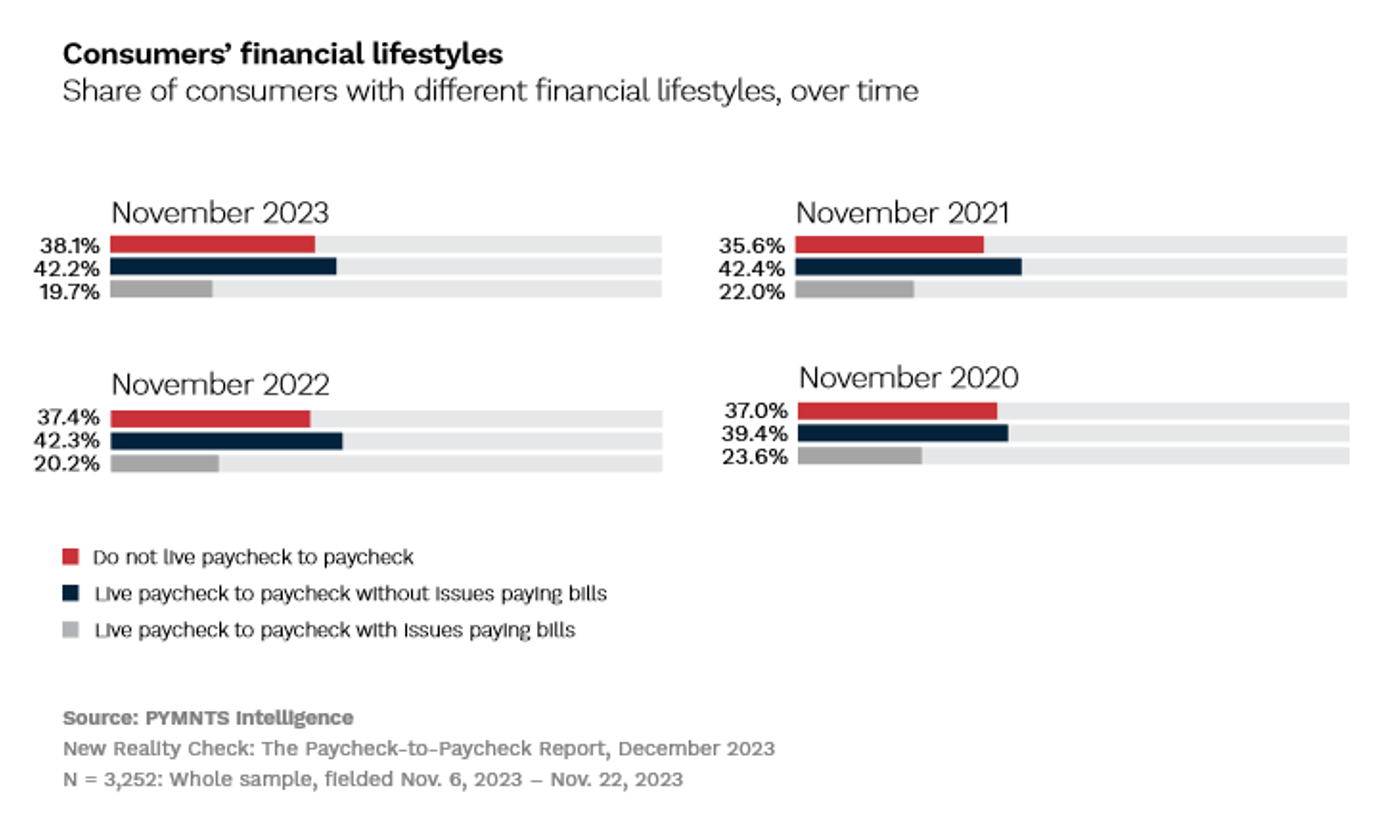

And the paycheck-to-paycheck consumer segment is a formidable demographic.

According to the December 2023 edition of “The New Reality Check: The Paycheck-to-Paycheck Report,” 62% of consumers say they live paycheck to paycheck.

The PYMNTS Intelligence report is based on a survey of 3,252 U.S. consumers and years of historical data, providing a uniquely detailed perspective into the financial balancing act many Americans must negotiate.

For starters, living paycheck to paycheck is a status that reaches across an array of income brackets. The report found that 77% of respondents who earn less than $50,000 each year define themselves as paycheck-to-paycheck consumers, while 67% of those earning between $50,000 and $100,000 say they too live paycheck to paycheck. Even those earning six figures are not immune; 45% of those making more than $100,000 annually report living paycheck to paycheck.

Collectively, nearly 20% of all paycheck-to-paycheck consumers say they struggle with bills; however, the report found most consumers are committed to managing credit despite their financial circumstances.

And this is why Capital One’s potential purchase of Discover might prove beneficial to both the two financial powerhouses and consumers.

As previously mentioned, both Capital One and Discover have long histories working with paycheck-to-paycheck consumers, and “The Paycheck-to-Paycheck Report” found nearly 60% of all credit cards are held by consumers living paycheck to paycheck.

But — despite the easy access to money credit cards can provide — PYMNTS Intelligence uncovered a variety of data points that show most paycheck-to-paycheck consumers are fiscally responsible.

For starters, 40% of paycheck-to-paycheck consumers with credit cards have “no issues paying their bills.” The report also found that paycheck-to-paycheck consumers are more likely to reach for their debit cards when making day-to-day purchases rather than their credit cards.

Additionally, 40% of paycheck-to-paycheck consumers have earned — and maintain — super-prime credit scores (720 or higher), demonstrating a commitment to preserving their solid credit scores — despite financial obstacles.

And though around 4 in 5 of all consumers consider their credit scores to be very or extremely important, paycheck-to-paycheck consumers aren’t far behind: 77% of those who have no issues paying their monthly bills treat their credit scores as very or extremely important, while 73% who do have issues meeting their monthly financial obligations also say credit scores are very or extremely important.

Findings such as these might explain one key motivation behind Capital One’s proposed acquisition. As PYMNTS recently noted, paycheck-to-paycheck consumers are “typically not targeted by the largest banks (or the … largest card issuers).” Given its reputation, it’s possible that Capital One may be betting on appealing to a large consumer segment that is clearly committed to keeping its financial house in order.