Men With Higher Savings Tend to Splurge More Than Women

Consumers who indulge in extravagant spending across various product and service categories typically maintain significantly higher savings.

This is one of the key findings in “New Reality Check — The Paycheck-to-Paycheck Report: The Nonessential Spend Deep Dive Edition,” in which PYMNTS Intelligence draws on insights from a survey of more than 3,400 U.S. consumers to examine the impact of nonessential spending on consumers’ ability to manage expenses and put aside savings.

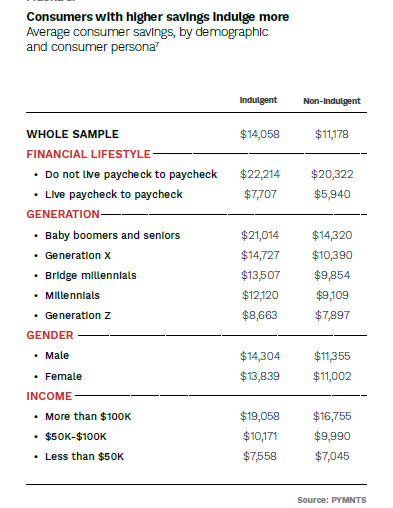

Data from the PYMNTS Intelligence-LendingClub study shows that on average, these indulgent consumers have savings balances that are 26% higher than those who do not engage in such spending. With an average savings balance of $14,058, indulgent consumers outpace non-indulgent consumers, who have an average savings balance of nearly $11,200.

The correlation between savings and indulgent spending becomes even more pronounced when examining specific demographic groups. Among baby boomers and seniors, 18% engage in indulgent spending, and these individuals have savings balances that are 47% higher than their counterparts who do not indulge. On average, splurging baby boomers and seniors hold savings of $21,014, while non-splurging individuals have an average of $14,320 in savings.

Furthermore, the study reveals that high-income consumers earning more than $100,000 are more likely to engage in indulgent spending and have higher savings balances. This suggests that individuals with greater financial resources are more inclined to treat themselves to nonessential purchases.

Interestingly, the study uncovers a different pattern among Gen Z consumers. While 36% of Gen Z individuals admit to indulgent spending, their average savings are similar to those who do not engage in such behavior. This finding suggests that younger consumers may have different priorities when it comes to their finances, focusing less on saving and more on immediate gratification.

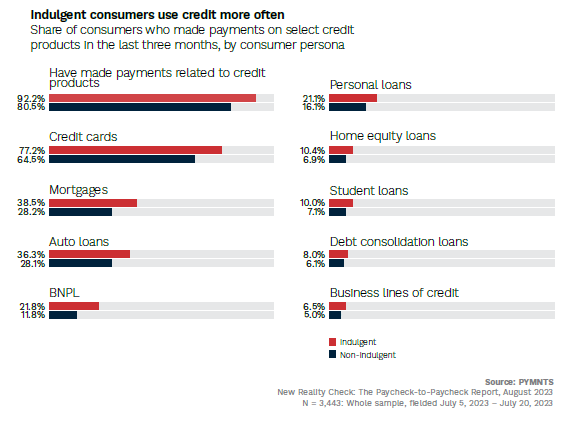

The study also explores the credit usage of consumers who engage in indulgent spending. Compared to non-indulgent consumers, indulgent shoppers have an 11 percentage point higher overall credit product usage.

Specifically, credit card usage is 20% higher among indulgent shoppers, indicating their reliance on credit for nonessential purchases. Furthermore, buy now, pay later (BNPL) usage is 85% higher among indulgent consumers, highlighting their preference for this payment method. Personal loans also see a higher usage rate among indulgent shoppers compared to non-indulgent consumers.

In conclusion, the study’s findings confirm the connection between savings and indulgent spending. Consumers with higher savings balances, particularly high-income consumers, men, and baby boomers, are more likely to engage in nonessential purchases. This study also highlights the increased credit usage among indulgent shoppers, further emphasizing the relationship between savings, indulgent spending, and credit utilization.