In challenging economic times, accessing credit is vital for many individuals, particularly those living paycheck to paycheck.

One form of credit that consumers often rely on is overdrafts, which serve as a safety net for individuals facing unexpected financial hiccups or temporary cash shortages. Unlike traditional loans or credit cards, overdrafts are a convenient way to cover immediate expenses without the formal application process or predetermined borrowing limits.

Additionally, the flexibility of overdrafts in enabling transactions that exceed available account balances is a major draw for individuals seeking short-term financial relief.

However, using overdrafts comes at a cost, as noted in “The Credit Accessibility Series: How Consumers Use Overdrafts,” a PYMNTS Intelligence report that used insights from over 2,800 consumers in the United States to examine consumer behaviors and sentiments related to the use of overdrafts.

According to the survey, consumers living paycheck to paycheck were six times more likely to have attempted a transaction without sufficient funds in the past year, with more than two-thirds of those transactions resulting in an overdraft fee being paid.

Millennials and credit marginalized consumers — individuals who have experienced at least one credit rejection in the past year — were also more likely to attempt transactions with insufficient funds.

While some financial institutions offer to cover overdrafts without a fee, the survey found that 71% of transaction attempts without sufficient funds resulted in the account being overdrawn, with the average consumer being overdrawn for nine days.

Most consumers who experienced overdrafts had their accounts with FIs that covered them for a certain amount of time or up to a certain amount of money without a charge or transaction decline. However, many consumers were still unable to cover their overdrafts during the grace period.

The survey also revealed that overdrafts often resulted in additional fees for consumers. High-income consumers and Generation X consumers paid overdraft fees at a higher rate than other consumer groups. On average, high-income consumers paid $30.90 in fees, while low-income consumers paid $25.50. These fees can add to the financial burden of low-income consumers, who are already in vulnerable financial situations.

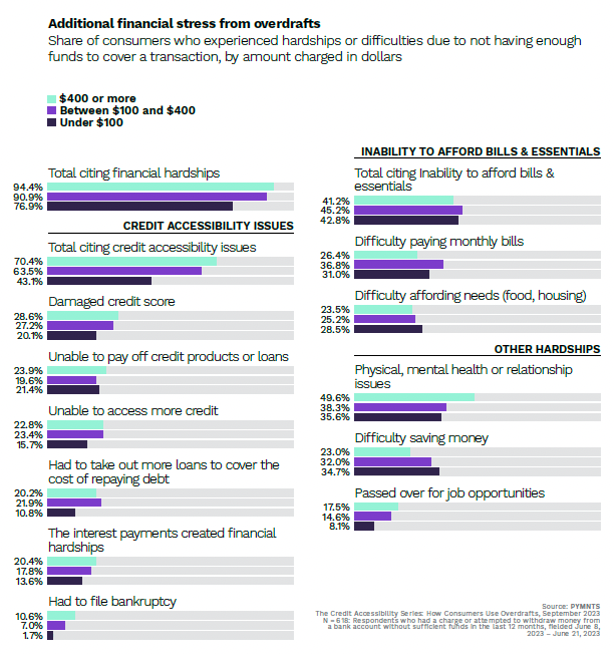

The survey found that consumers who struggled to cover charges to their accounts experienced further financial hardships. Two-thirds of overdrafts led to broader credit accessibility issues, such as damaged credit scores or the inability to pay accumulated fees.

The survey data indicated that consumers who frequently used overdrafts or had higher dollar amounts charged were more likely to experience financial hardships. For example, 98% of consumers with more than one overdraft each month reported some form of hardship, compared to 79% of those who had an overdraft only once or twice a year.

Moreover, among individuals who used overdrafts for transactions exceeding $400, 94% encountered difficulties, such as challenges in obtaining credit or difficulties in meeting bill payments. In contrast, only 77% of those who made transactions under $100 experienced similar hardships.

Similarly, the shortfall of funds to cover transactions under $100 can bear notable consequences on credit accessibility. Specifically, 43% and 20% of consumers, respectively, reported facing issues with obtaining credit and suffering damage to their credit scores due to this shortfall.

While overdrafts offer a lifeline of financial flexibility during crunch times, the convenience they offer can be overshadowed by the extra financial strain they introduce. As the study revealed, the fees and interest associated with overdrafts can lead to increased financial stress and, in some cases, compound the hardships consumers are already facing.

This underscores a critical need for comprehensive financial education, empowering consumers with the knowledge needed to make informed decisions about their finances, including understanding the implications of using overdraft facilities.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More