Reports from banks and payment networks show credit card delinquency rates are on the rise.

Connect the dots, and the data hints at trouble ahead in the paycheck-to-paycheck economy.

Citigroup said in its latest details from its Credit Card Issuance Trust that its 30-day delinquency rate was 1.3% in November, up from 1.04% in the previous month.

American Express said in its own filings that its 30-day past due loans as a percent of the total was somewhat steady at 0.9% on its consumer loan book — although net write offs were 1% in November, up from 0.9% in October.

Bank of America has detailed in its own Securities and Exchange Commission (SEC) filings that its delinquency rate stood at just over 1% in November from just under 1% in October and from 0.92% a year ago.

The data squares with commentary from the St. Louis Federal Reserve, which showed that the delinquency rate on credit cards for all banks at the end of the third quarter stood at 2.1%, up from 1.9% in the second quarter and up from 1.6% a year ago. Elsewhere, the Fed released data in November that showed that credit card balances had risen by $38 billion, a 15% year-over-year increase and the most outsized jump in 20 years.

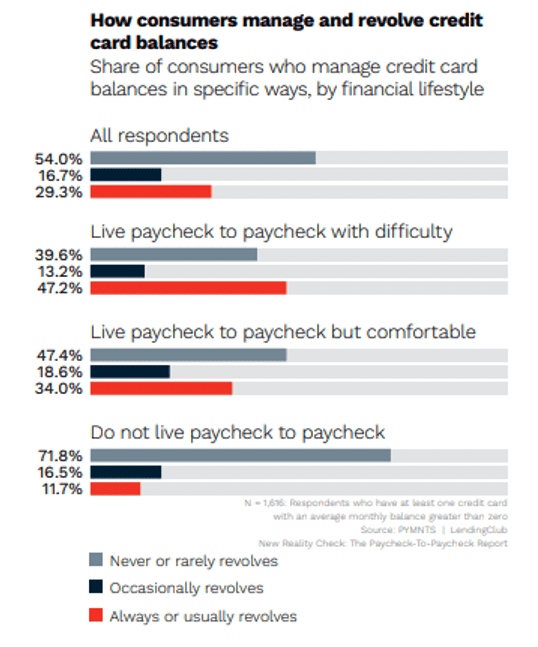

Paycheck-to-Paycheck Consumers Embrace Credit Cards

Paycheck-to-paycheck consumers are three times as likely than other cohorts to revolve credit card debt and carry higher monthly balances overall. Those consumers who never pay their credit balances in full also tend to hold more credit cards than average. The fact that most of us live paycheck to paycheck — at 63% of U.S. consumers — also signals that holding credit cards is a widespread occurrence.

As delinquency rates creep up, it may be the case that peer-to-peer (P2P) consumers are finding it harder to meet their monthly obligations. Inflation is making it hard to triage just where the money goes.

Indeed, PYMNTS data, compiled in collaboration with LendingClub, showed that credit card holders have approximately two credit cards, but the tally rises to three among those not likely to pay their credit card balances in full or those who “always” or “usually” have a revolving balance. The people who revolve their balances is also higher than the balances carried by the consumers who pay their balances every month.

Struggling consumers are, by and large, nearing their limits on their cards. For those struggling consumers, the average credit card spending limit is $4,700, and they have an average balance of $3,800. Paycheck-to-paycheck consumers who do not struggle to pay their bills report an average spending of $3,100 and a limit of $6,500.