In the United States, the average consumer has four credit cards, and the total credit card debt is nearly $1.1 trillion, according to data from the Federal Reserve Bank of New York. But who do they turn to for their primary credit cards?

Consumers pick national banks, followed not so closely by credit unions and community banks, according to “Credit Unions and Community Banks Gain Credit Card Issuing Momentum,” a PYMNTS Intelligence and Elan Credit Card collaboration. The study, which drew from a survey of 2,088 U.S. consumers, examined evolving preferences regarding card issuers.

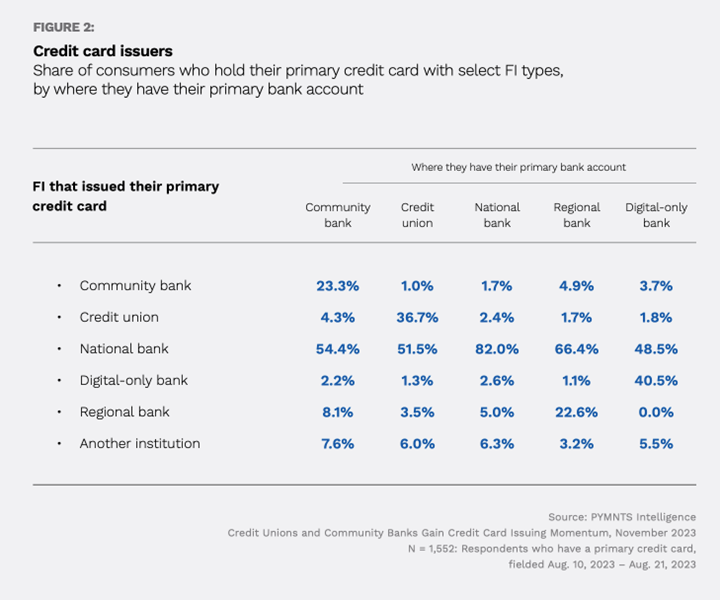

It found that U.S. consumers prefer national banks for their primary credit cards over any other issuer, even if they have a primary bank account with another financial institution. This preference is stronger among clients from traditional FIs, but it also applies to digital-only bank clients.

Although the share of adults holding a primary credit card issued by a national bank has declined from 76% to 68% since 2020, these FIs are still the dominant issuers of consumer credit cards in the U.S. They have the broadest coverage of bank accounts nationwide, allowing them to reach more customers with whom to cross-sell credit cards.

They are also the preferred choice for primary credit cards for customers of any FI. Two-thirds of consumers who have a primary bank account at a regional bank use a credit card issued by a national bank as their primary option. In the case of community banks or credit unions, the portion exceeds 50% in both cases. Where they seem to be less successful is among digital bank customers, where the share stands at 48%.

Nevertheless, regional banks, credit unions and community banks combined have increased the share of consumers choosing them for their primary credit cards from 14% to 21% since 2020. This trend is poised to grow as many consumers prefer credit unions or community banks for their next credit card, including sizable shares of those currently without a primary card.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More