Many credit unions (CUs) have resolved to follow rather than lead in digital innovation. Nearly two-thirds adopt a cautious wait-and-see approach even as more members want innovative experiences and their competitors gain an advantage.

PYMNTS’ latest study finds that 28% of CU members are willing to ditch their current financial institution (FI) for one that offers more leading-edge digital banking experiences — and the share is growing. By disregarding the potential of innovation as a differentiator and member retention strategy, CUs risk their members leaving.

PYMNTS’ latest study finds that 28% of CU members are willing to ditch their current financial institution (FI) for one that offers more leading-edge digital banking experiences — and the share is growing. By disregarding the potential of innovation as a differentiator and member retention strategy, CUs risk their members leaving.

These are some of the key findings in “Credit Union Innovation: Credit Union Membership and Credit Profiles,” a PYMNTS and PSCU collaboration. The report is based on a survey of 4,097 consumers conducted in April. We gathered data on consumers’ opinions on digital and product innovation and how this affects their views of their financial services providers. We also surveyed 100 CU executives with responsibilities such as financial planning and analysis, fraud detection or analysis, operations, product development and research and development. Additionally, we surveyed 54 executives from FinTechs that provide products and services to CUs, individual consumers, commercial banks and community banks during the same period.

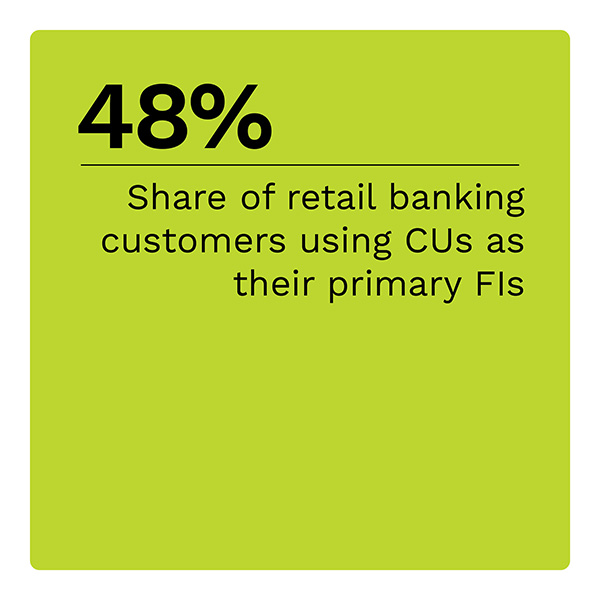

Urban millennials prefer to use a credit union.

Credit unions appeal most strongly to the lucrative millennial and bridge millennial age groups, with 56% and 57%, respectively, choosing CUs as their primary FIs. Urban consumers also slightly prefer credit unions to other FIs. However, CUs trail other FIs among older consumers, Generation Z and consumers in rural areas.

Convenience and trust drive banking and credit union satisfaction.

Customer satisfaction in retail banking is rooted in convenience and trust. Thirty-six percent of retail banking consumers attribute their satisfaction to convenience. This share climbs to 43% among consumers with subprime credit scores. Trust tops the list for CU members, with nearly one-third identifying it as the key to their satisfaction. Perceptions about trust also correlate with credit persona. Super-prime and prime consumers are more likely to cite trust as a key determinant of satisfaction than subprime consumers.

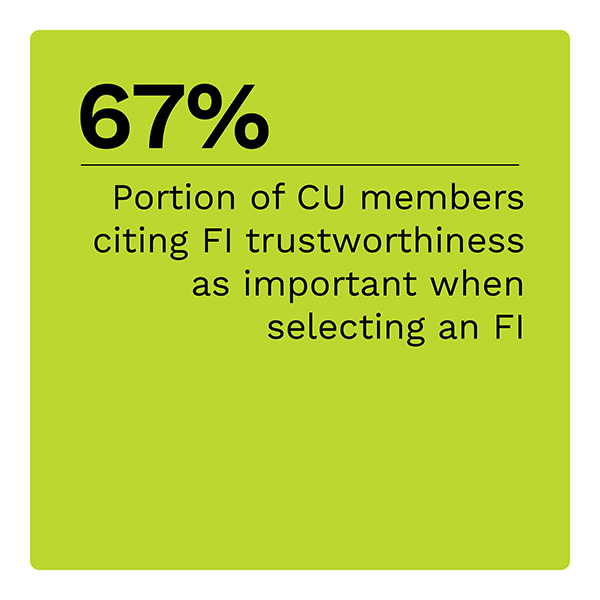

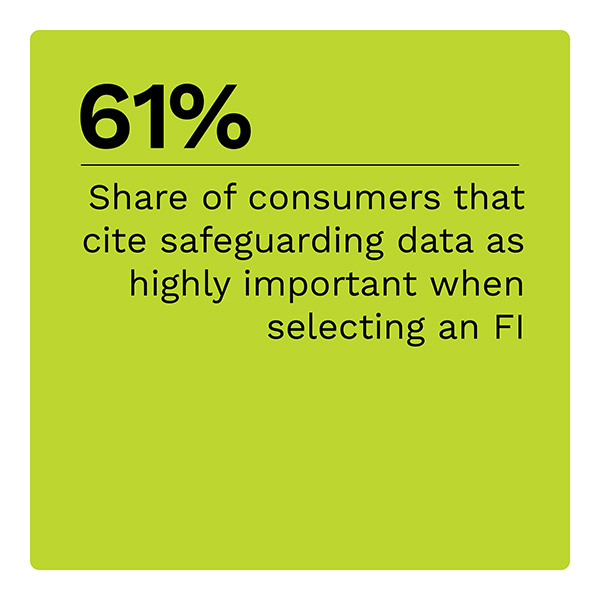

Security is paramount for consumers with strong credit scores.

Trust, data privacy and asset security are pivotal for consumers boasting strong credit profiles when selecting an FI. Our data shows that two-thirds of CU members and super-prime consumers value trustworthiness above all other factors. A somewhat lower share of consumers values data security. Though asset protection commands less emphasis than trust and security, most consumers still consider it critical to their decision.

Consumer perspectives on product innovation and what innovations FIs offer can make or break whether customers stay or go. Download the report to learn more about how digital banking innovation influences consumers’ views on where to take their money.