Banks have been forced to reduce or suspend in-branch activities to prevent the risk of infection at branches at least temporarily. The largest bank in the United States, J.P. Morgan Chase, closed 1,000 branches for awhile, and Citigroup temporarily shut down 100 branches.

Customers are instead turning to digital means to maintain their financial lifestyles, and this shift is likely to continue even after the pandemic is in the rear-view mirror. A recent survey found that the pandemic has changed the way 45 percent of bank customers interact with their FI, with Citigroup seeing an 84 percent increase in daily mobile check deposits in May, and digital bill payments increasing by 78 percent between February and April.

In the July Digital-First Banking Tracker®, PYMNTS explores the latest in the world of digital-first banking, including the long-lasting effects brought on by the pandemic, the shifting attitudes surrounding ATM use, and how the digital banking development field is reaping dividends from the financial industry’s sea change.

Developments From Around The World Of Digital-First Bank ing

ing

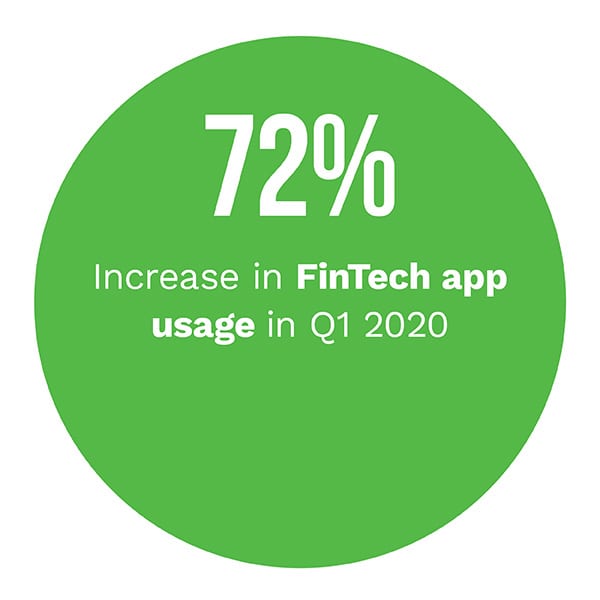

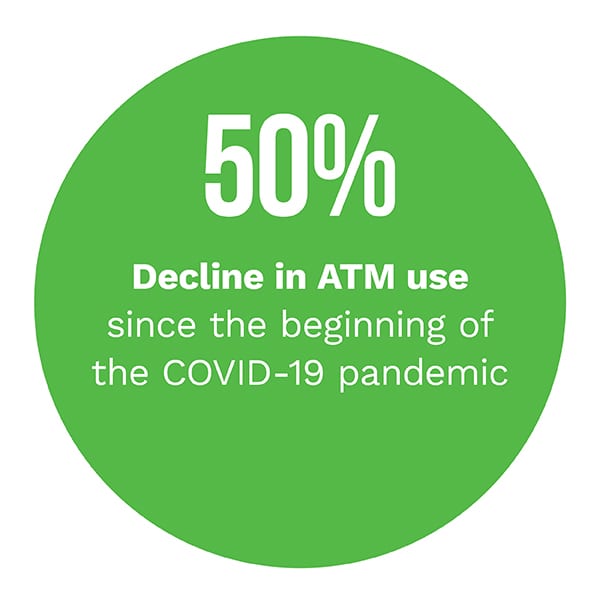

ATM usage rates have been one of the financial industry’s many casualties amid the pandemic. A study from AppsFlyer and Google found that global ATM use had decreased by 50 percent since the beginning of the outbreak as social distancing and stay-at-home orders have increased customers’ reliance on mobile apps and online banking options rather than ATMs. FinTech apps, for example, saw a 72 percent increase in usage in the first quarter of 2020 alone.

Developers of these digital banking apps have been seeing success, however, building on an overall trend toward digital banking that has been brewing for years. The global digital banking platform industry generated $3.95 billion in revenue in 2019, for example, and this growth is only expected to continue heading into the future. Experts predict that the market will reach $10.87 billion by 2027, generating a compound annual growth rate (CAGR) of 13.6 percent over the next seven years.

In-branch operations have been severely impacted by the pandemic, with many banks instituting an appointment-only mandate for meetings be tween bank staff and customers to reduce the risk of infection. This change in operations could remain after the end of the crisis, according to Stephen Griffin, senior vice president at Alabama-based Regions Bank, as it has two major benefits over the status quo. Not only can bank customers better plan their days around their bank visit, but it also helps bank staff more efficiently plan their daily operations as well.

tween bank staff and customers to reduce the risk of infection. This change in operations could remain after the end of the crisis, according to Stephen Griffin, senior vice president at Alabama-based Regions Bank, as it has two major benefits over the status quo. Not only can bank customers better plan their days around their bank visit, but it also helps bank staff more efficiently plan their daily operations as well.

For more on these and other digital-first banking news items, download this month’s Tracker.

Scotiabank On How COVID-19 Could Lead To Lasting Change In Banking Operations

Digital banking has never been more popular than it is right now, as consumers flock to online and mobile channels to avoid potential exposure at bank branches. Studies have shown this change is likely here to stay, meaning that bank branches will have to invest large sums in developing the infrastructure necessary to meet this demand.

In this month’s Feature Story, PYMNTS talked to Adam Swinemar, vice president of digital channels at Scotiabank, about how banks are helping their customers understand the capabilities of digital banking systems, and the logistical and educational challenges that banks face going forward.

Deep Dive: The Post-Pandemic Future Of The Financial Industry

Deep Dive: The Post-Pandemic Future Of The Financial Industry

The banking industry is scrambling to cope with the ongoing pandemic and is altering branch operations, investing in digital banking innovations and exploring several other avenues for customer engagement. The end of the pandemic will likely not be the end of the crisis for banks, however, as they will need to anticipate what the post-pandemic financial world will look like and begin planning accordingly as soon as possible.

This month’s Deep Dive explores how banks will leverage digital banking apps and revamped branch protocols to ensure customers’ needs are met in a safe and satisfying way once the pandemic is over.

About The Tracker

The Digital-First Banking Tracker®, done in collaboration with NCR Corporation, is your go-to monthly resource for updates on trends and changes in digital-first banking.

Financial institutions (FIs) are beginning to see the light at the end of the tunnel for bouncing back from the pandemic, but the crisis has not been without its casualties.

Financial institutions (FIs) are beginning to see the light at the end of the tunnel for bouncing back from the pandemic, but the crisis has not been without its casualties.