There has been a seismic shift in how the world banks due to the pandemic. More than half of U.S. adults were fully vaccinated as of early June, causing financial institutions (FIs) to question what the future of banking will look like as consumers return to normal. Many consumers were comfortable using online or mobile banking channels prior to the pandemic’s onset, but others reluctantly joined the switch to digital as branches closed and hours were reduced. The share of consumers who opted to interact with their bank digitally at least once a week has since reached 50 percent, a major increase from the 32 percent who did so just two years ago. Nearly 75 percent of Americans favored online banking before the pandemic, and this figure rose to 87 percent once restrictions set in.

There has been a seismic shift in how the world banks due to the pandemic. More than half of U.S. adults were fully vaccinated as of early June, causing financial institutions (FIs) to question what the future of banking will look like as consumers return to normal. Many consumers were comfortable using online or mobile banking channels prior to the pandemic’s onset, but others reluctantly joined the switch to digital as branches closed and hours were reduced. The share of consumers who opted to interact with their bank digitally at least once a week has since reached 50 percent, a major increase from the 32 percent who did so just two years ago. Nearly 75 percent of Americans favored online banking before the pandemic, and this figure rose to 87 percent once restrictions set in.

Many consumers welcomed the digital turn, though some who prefer in-person experiences at branches, even for simple transactions, took time to convince. One survey revealed that 55 percent of respondents who preferred in-person banking prior to the pandemic are now more receptive to going digital. The conversion of this consumer group is expected to have long-term effects on the banking space, too. This month’s Deep Dive will examine how digital-first banking has quickly evolved over the course of the pandemic and what consumers can expect from their banks in a post-pandemic world.

Digital Shift Challenges

The switch from physical branches to digital channels will likely have a lasting impact. Thirty percent of those who used bank branches before the pandemic plan to keep using digital banking channels even after all restrictions have lifted. The top reasons for this are that 54 percent enjoy the easy access, 49 percent prefer banking without in-person interactions and 26 percent find online and mobile financial tools to be useful.

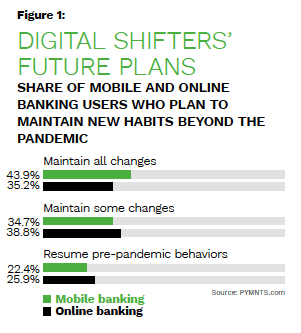

Most consumers plan to keep at least some of the changes they made during the pandemic, most prominently their use of digital services, according to PYMNTS research. Nearly 44 percent of mobile banking users plan to maintain all of their changes, while another 35 percent will maintain at least some.

The massive volumes of transactions and banking activities now being carried out online mean that there has also been an increasing need for tighter security and consumers’ cooperation by supplying information to confirm their identities. One study found that 23 million U.S. consumers, 11 percent, are convinced that their identities have been stolen by cybercriminals and used to open accounts at some point. Seventy-five percent of consumers are thus willing to provide banks their biometric information, such as fingerprints, facial scans or voiceprints, to help safeguard their sensitive data.

It is important for banks to carry out these security checks within the same channels on which consumers are onboarded. An average of 25 percent of Americans will go to a competitor or abandon an application if asked to leave the channel to finish the identity verification process. FIs will have to streamline the user experiences on their digital banking channels to keep consumers satisfied and engaged.

Post-pandemic Customer Expectations

Consumers may have become more comfortable with digital banking throughout the last year. But 49 percent plan to return to in-person banking after restrictions are lifted, according to a survey. The most popular reasons for wanting to return to in-person banking are that 31 percent find it easier to bank in person, 28 percent believe that digital banking tools are difficult to use, 24 percent would rather discuss finances in person with a bank associate and 17 percent think it is safer to complete transactions in person. Thirteen percent of respondents did not follow the digital-shift trend and continued to visit bank branches. This group resisted digital channels mainly due to distrust and security concerns. Forty percent worried about privacy, 39 percent disliking the idea of managing finances on computers or mobile phones and 25 percent not trusting online banking.

Consumers expect uninterrupted banking journeys when they open accounts digitally. They have voiced displeasure at being forced to use separate channels to complete tasks, especially when providing proof of identity during onboarding. Canadians have higher expectations than U.S. consumers when it comes to completing tasks digitally. Seventy percent of Canadians expect to be able to prove their identities digitally, 60 percent said they should be able to prove their addresses online or via an app and 45 percent noted they prefer to establish biometric security within the digital channel. The shares holding those expectations drop to 62 percent, 52 percent and 42 percent, respectively, in the U.S.

If FIs are to meet consumers’ expectations in the digital-first banking world, they must focus on improving user experiences and building trust by communicating the security measures in place to keep their information safe. Only then will consumers either confidently stick with digital options or finally go digital for the first time.