Banking faces a critical juncture. Against a rising tide of inflation and record debt levels, 59% of retail bank customers say they expect help from their financial institutions (FIs) in understanding and managing their financial health. All too often, however, consumers are finding that help lacking. United States retail bank customers’ overall satisfaction has dropped over the last year, with one survey finding that traditional banks came in last in customer satisfaction when compared against their digital competitors. Still another report found that customers in the Asian-Pacific (APAC) region now trust Big Tech to handle their banking more than their banks.

Consumers consistently show a strong preference for digital approaches to financial support, underlining the necessity of banks’ meeting their clients’ technology needs. With Americans growing increasingly burned out by financial difficulties, traditional banks have a golden opportunity to become the trusted financial advisers their customers crave through robust digital innovation.

Traditional banks have the home advantage

For all consumers’ overwhelming interest in digital financial tools, it is worth noting that just 9% of banking customers have their primary bank accounts with digital-only banks. Consumers are still disinclined toward exclusively digital banking experiences, continually expressing a need for contact with a real person in a branch, on the phone or via chat. They are also experiencing unprecedented anxiety about their finances, with more than half wanting their FIs to be proactive in reaching out to them if their spending habits put them at financial risk.

This complex combination of preferences represents a powerful advantage for traditional banks. By negotiating a balance between the human element and innovation, formerly legacy banks can be everywhere their customers need them to be. That said, they can achieve that balance only by offering the kinds of digital tools their customers most want, from notifications when finances are insufficient to cover upcoming bills to all-in-one financial services and biometric logins.

Partnering for success

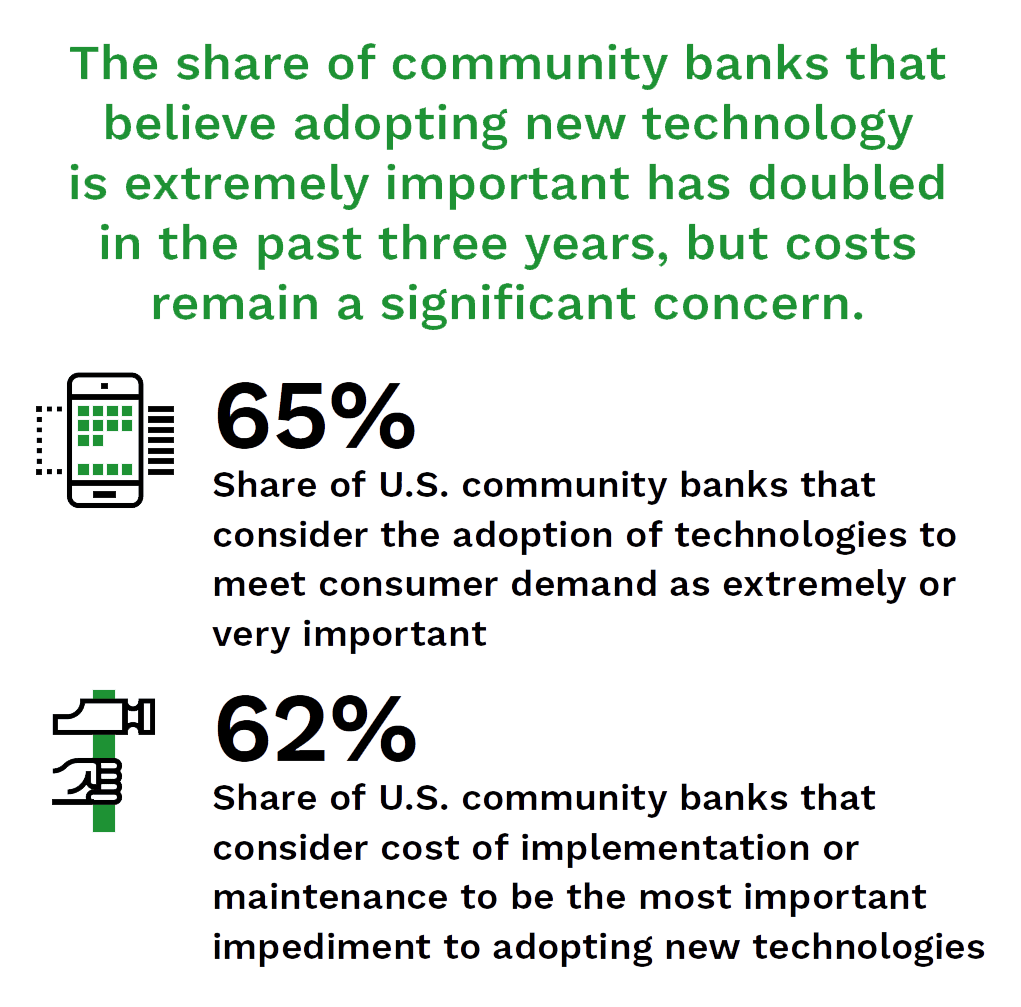

Banks are spending on technology, with a median increase of 11% in their technology budgets last year. The costs of implementation and maintenance, however, continue to be an obstacle, with nearly two-thirds of community banks considering costs to be the most important impediment to their adoption of new technologies.

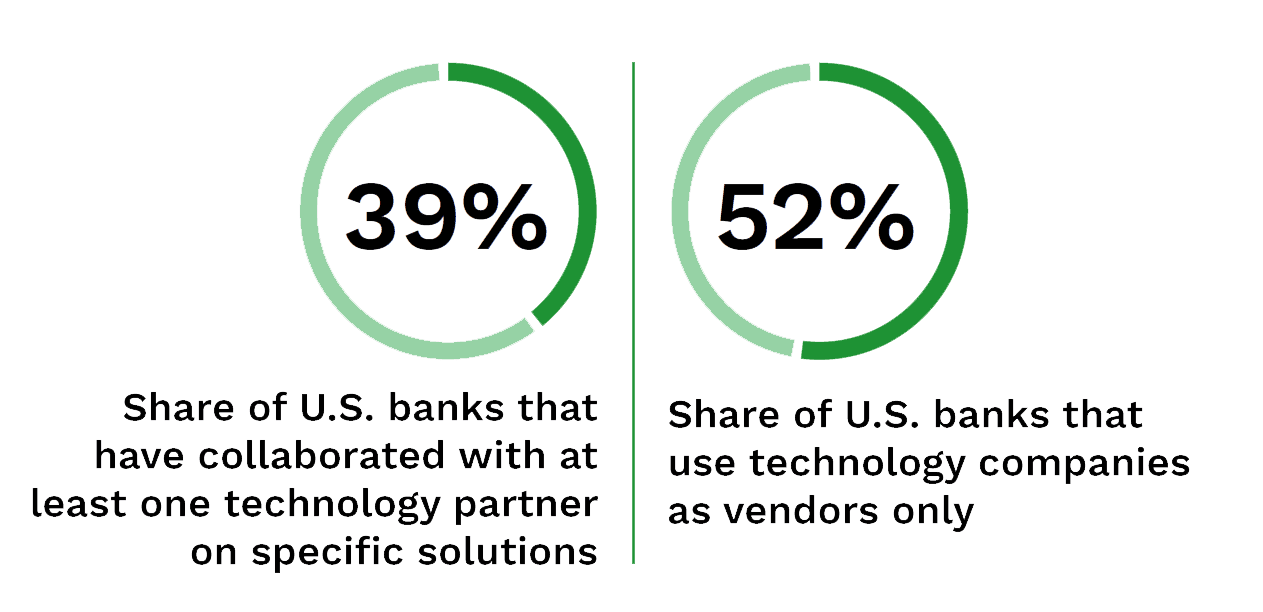

The U.S. Department of Treasury is encouraging responsible partnership between banks and FinTechs to do away with the outdated notion that there must be rivalry between the two. With 45% of banks still relying on antiquated technology and 35% unable to identify the right tools to achieve strategic goals, it is vital for banks to be aligned with technology providers to fulfill their objectives. Partnerships can reduce the costs of innovation for banks and make serving consumers’ needs in adversity a shared victory for all participants.