Being underbanked or unbanked is a significant disadvantage in modern society, as this locks households out of personal loans, direct deposits, many types of credit payments and a host of other functionalities that much of the world takes for granted. There are 1.7 billion unbanked adults around the world, according to the World Bank.

Expanding banking and payment services to the underbanked, typically low-income individuals from minority populations, will be crucial to bolstering their economic status. In the United States, 35% of households making less than $40,000 annually are underbanked, and only half of Black householders have access to financial services, according to the Federal Reserve. Telecommunications-based banking and payments could be a crucial tool for reaching these households and improving their economic potential.

Being underbanked has a variety of causes.

More than half of the world’s unbanked adults live in just seven countries, largely concentrated in Asia and Africa, with India claiming the largest global share of unbanked individuals at 17% of the world total. The U.S. is also no stranger to unbanked households, with 16% of the population considered to be underbanked and 8% having no bank account at all.

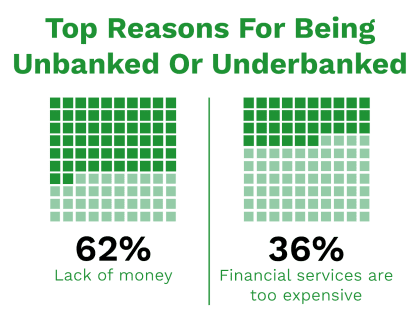

There are many reasons for households to remain unbanked, but financial difficulties are the most prominent factor. More than 60% of unbanked individuals said lack of money was a reason for not opening a financial account, and slightly less than 40% said that financial services are too expensive. Another 27% cited lack of proper documentation to obtain a financial account.

Telecommunications payments can be a valuable tool in enabling financial access for underbanked individuals by linking directly to customers’ devices without requiring the middleman of a financial institution (FI). In almost all the countries with the largest proportions of unbanked households, individuals with mobile phones outnumber those with bank accounts, so offering banking through their phones is an easy way to expand financial access.

Telecom payments can use consumer data to drive customer experiences.

Telecom companies not only can provide banking services to underbanked individuals but also can partner with FinTechs to improve their digital offerings. FinTechs have traditionally used cookies to track customer habits and provide personalized experiences, but many are planning to phase out cookies by next year due to evolving data privacy regulations.

Telecom companies not only can provide banking services to underbanked individuals but also can partner with FinTechs to improve their digital offerings. FinTechs have traditionally used cookies to track customer habits and provide personalized experiences, but many are planning to phase out cookies by next year due to evolving data privacy regulations.

Personalizing experiences could be crucial to improving consumer participation in online-only banks. Currently, just seven out of 100 consumers use an online-only FI as their primary bank, despite huge interest in digital banking services. Leveraging telecom data in partnership with FinTechs could be the key to filling this participation gap, especially among older generations and other cohorts who are reluctant to bank with a digital-only FI or one run by a telecom.