In an interview with PYMNTS earlier this year, Casey Porter, vice president of merchant sales and acquiring at Visa’s Global Acceptance Fast Track, spoke to PYMNTS CEO Karen Webster about the evolution of PayFacs, highlighting how they have evolved from their 1990s roots, when merchant acquirers handled enrollment, boarding, underwriting and settlement.

Back then, Porter said companies were reluctant to navigate the complexities of setting up a merchant account due to lower transaction volumes. This is where aggregators stepped in, managing underwriting, assuming responsibility, and offering this service. This alleviated the underwriting burden for acquirers, expanding beyond the medical field into utilities and later into various other industries.

Fast forward to today, and although the acquirer is still involved in the transaction from a revenue and risk perspective, the PayFac now stands as “an entity that has control of the transaction and the merchant experience, from end to end,” Porter said.

Moreover, as more businesses transition online and numerous companies operate digital-only entities, PayFacs have had to adapt, expanding beyond simply facilitating card transactions to helping merchants enhance consumer-facing experiences across diverse verticals.

According to findings detailed in a recent study conducted by PYMNTS Intelligence in collaboration with Carat from Fiserv, among the entities enabling payment acceptance, PayFacs facilitate payments for 39% of independent software vendors (ISVs) and 78% of marketplaces that engage with them. And in a nod to the digital era, 59% of PayFacs are dedicated exclusively to supporting digital payments either online or through specialized applications.

Examining the data further shows that customer demand plays a crucial role in determining the payment methods offered by PayFacs. Digital wallets are gaining traction among ISVs and PayFacs, with approximately one-third of transactions being made using digital wallets. Marketplaces, on the other hand, see only 22% of transactions completed via a digital wallet.

As businesses strive for growth, PayFacs are also exploring their potential for expansion. Per the study, these entities estimate that value-added services, such as installment payments and invoicing, are key drivers for their growth, accounting for half of their projected revenue next year. Currently, they generate around 66% of their revenue from payment processing.

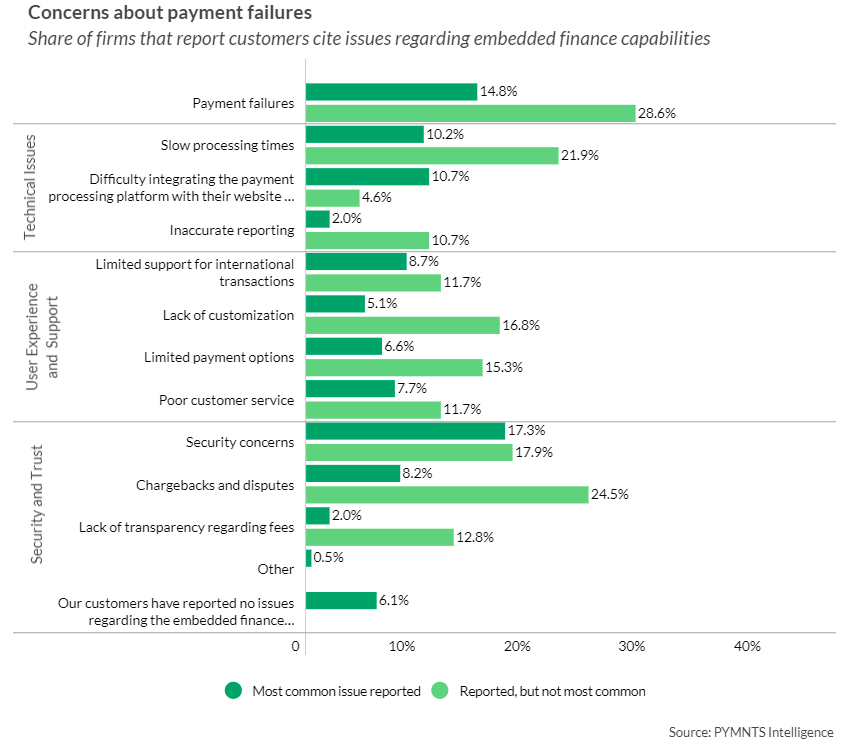

However, certain customer service issues will need to be addressed for PayFacs to reach their full potential.

As the study noted, 43% of firms report customers encountering payment failures. Specifically, 12% of PayFacs’ clients face payment failures on a monthly basis, accumulating to 43% throughout the year. One-third of these businesses deal with chargebacks and disputes, while 15% report customer struggles in integrating the payment processing platform into their websites or apps.

In essence, PayFacs are playing a pivotal role in reshaping the payments industry by enabling software platforms, ISVs and eCommerce marketplace sellers to integrate payments into their end customer experience. With the increasing demand for digital payments, these entities are set to continue their significant impact on the payments industry in the coming years.