In the latest Disbursements Tracker, PYMNTS explores how banks and card providers are approaching payment innovations to keep pace with consumer demand, and to better protect against fraudsters.

In the latest Disbursements Tracker, PYMNTS explores how banks and card providers are approaching payment innovations to keep pace with consumer demand, and to better protect against fraudsters.

Around the Disbursements World

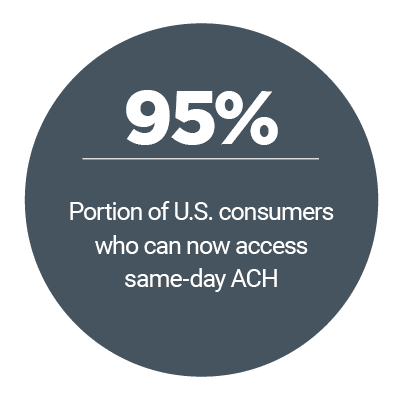

Though regulators and banks in the U.S. have expressed a vested interested in real-time payments, the U.S. Federal Reserve is years away from actually developing one. The Fed is still debating whether or not it should even take an active role in real-time payments, even as it continues to roll out ACH settlement windows.

In other markets, the growth of instant and mobile payments is breeding more competition by the day. Social media platform Facebook is set on further innovating WhatsApp features with a new U.K.-based team. The team will focus on building out the WhatsApp payment capabilities, as the company looks to expand them to new countries.

For instance, Facebook is promoting WhatsApp payments in India, where it’s already facing competition from other interested foreign parties. Amazon is also pushing into the region, relying on India’s Unified Payments Interface (UPI) to enhance P2P payments through Amazon Pay.

To find out more news and trends, download the Tracker.

Why Cash Security Deposits Should Be the Exception to the Rule

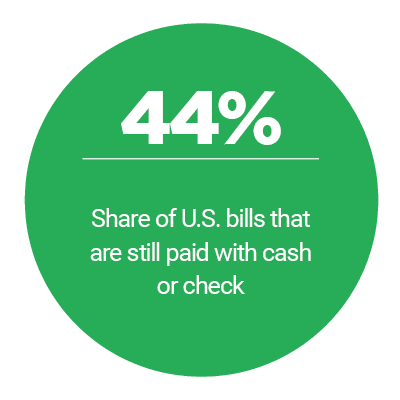

While consumers have come to expect digital and instant disbursements, many of them still rely on legacy methods, like cash and checks, for larger payments. In the real estate space, for example, a cash security deposit is a common way for tenants to secure a new lease with a potential landlord — a costly and cumbersome process for both parties involved in the transaction.

In this month’s feature story, PYMNTS spoke with Paraag Sarva, CEO and co-founder of Rhino, about why the cash security deposit should be eliminated altogether in favor of insurance policies, thereby freeing up $190 billion tied up in deposits.

Deep Dive: The Challenges of Government Disbursements

Millions of customers and businesses worldwide are still reliant on difficult and slow methods of payment, which can lead to costly delays. While some governments are moving forward with digital payments to fix these friction points, others are struggling.

To read the Deep Dive and discover more about the state of government disbursements, download the Tracker.

Around the world, banks and FinTech firms are addressing challenges associated with enabling fund disbursements in real time — and some markets are developing real-time networks faster than others.

Around the world, banks and FinTech firms are addressing challenges associated with enabling fund disbursements in real time — and some markets are developing real-time networks faster than others.