Cash flow had become a significant problem for businesses since the pandemic began.

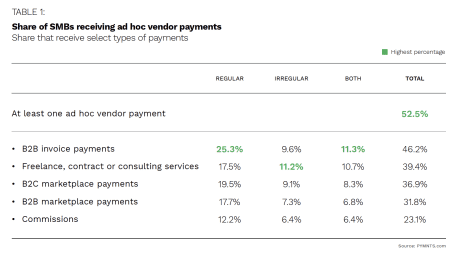

Of the approximately $1.2 trillion in outstanding receivables that small- to medium-sized businesses (SMBs) in the United States obtain each year via ad hoc payments, PYMNTS’ research indicates that 30% are paid late. That means SMBs are forced to chase down $465 billion in revenue or wait until long after the due date to receive their funds. This delay creates cash flow problems for SMBs and strains their B2B relationships when larger organizations do not send payments on time.

These delays do not just plague checks in the mail, either. Automated clearing house (ACH) payments are the most common disbursement method in the U.S., but even these payments cannot provide instant payouts or ensure payments ubiquity. ACH transfers, which take up to three days, are slow by modern standards, especially for SMBs operating on tight margins due to labor and supply costs. Late payments — and even on-time payments — also can be complicated by additional hold periods enforced by receiving financial institutions (FIs).

With their own expenses to meet, businesses and consumers alike are looking to receive disbursements more quickly. Instant payments are becoming more popular, and 75% of SMBs said instant payments offered without additional fees would encourage them to continue business relationships with buyers. Regardless, just 9% of ad hoc vendor payments are instant.

Even in the case of business-to-business (B2B) marketplace disbursements, which are the most common to involve instant payment methods, just 10% of such disbursements to SMBs are instant. This month, PYMNTS examines the benefits of payments ubiquity in B2B transactions, as well as the challenges standing in the way of getting there.

Capitalizing on Business Demand for Faster Disbursements

Instant payments’ popularity transcends cost, and 54% of SMBs said they would be “very” or even “extremely” willing to pay a fee to receive instant payments for ad hoc vendor transactions. The willingness to pay for instant payments is highest among SMBs that have received them in the past, with 68% of these businesses expressing a willingness to pay an additional fee for reliably faster disbursements.

Sixty-eight percent of those operating in B2B digital marketplaces said they would be either “very” or “extremely” willing to pay a fee for instant payments, and 69% of SMBs would be willing to pay a fee for instant payments on commissions.

SMBs’ interest in paying a fee to receive instant payments for B2B digital marketplace transactions and commissions, which are the disbursements most likely to be received late, demonstrates just how significantly late payments can affect SMBs’ ability to operate. The likelihood of receiving an ad hoc payment late correlates directly to vendors’ willingness to accept an added fee to speed those payments. For these businesses, instant payments are not simply an added value — they are a potential solution to cash flow problems.

Instant Payments and Consumer Relationships

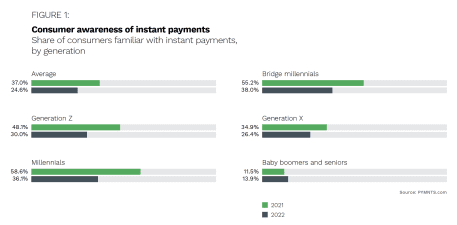

Instant payments also are a hot commodity among consumers, who are increasingly aware of these disbursement options and display a strong preference for them when they are offered. PYMNTS’ research indicates that 37% of consumers are aware of instant payments and what they are — a 50% jump from 2020.

Instant payments also are a hot commodity among consumers, who are increasingly aware of these disbursement options and display a strong preference for them when they are offered. PYMNTS’ research indicates that 37% of consumers are aware of instant payments and what they are — a 50% jump from 2020.

When given a choice of how to receive a disbursement, most consumers choose instant payments when they are available, and 46% of consumers said they would be “very” or “extremely” likely to choose instant payments if given the option. Consumers also generally are receptive to paying fees to unlock the convenience of instant payments. As many as 52 million U.S. consumers would be willing to pay a fee for instant payments, for example, an increase of 15% from 2020.

Additionally, 66% of disbursement recipients said they would be more likely to continue doing business with organizations that offered instant payments without an added fee, compared to 39% of consumers who said the same regarding direct deposit disbursements. This makes free instant payments worthwhile as a way to build customer loyalty.

Achieving Payments Ubiquity

Businesses face greater challenges in reaching a point at which they can reliably send disbursements easily and quickly, regardless of how recipients wish to receive those funds. As a result, they may find it tempting to fall back on traditional payment means, such as checks. With all the security risks and inefficiencies that these paper-based payments bring, they still allow businesses to send and receive disbursements to anyone — a payments ubiquity that many digital solutions lack.

Achieving digital payments ubiquity is no small task, as organizations must connect to multiple types of accounts and platforms and ensure disbursement recipients can access funds quickly, safely and through the method they prefer. Solutions that restrict a disburser to a single network or platform may make some forms of instant digital payments possible, but even these do not reach payments ubiquity.

To truly pay anyone, anywhere and at any time, organizations must look to providers that can connect them — and their payees — to all the available options.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More