United States consumers received 11 billion disbursements in 2021, and 17% of those were instant payments, approximately tripling the 5.7% of instant disbursements made in 2020. Instant payments are gaining even on same-day account transfers, with 22% of consumers receiving disbursements by same-day automated clearing house (ACH) versus 20% who received at least one disbursement as an instant payment. Consumers are now 50% more likely to be aware of instant payments than in 2020, and they are 15% more likely to choose instant payments.

United States consumers received 11 billion disbursements in 2021, and 17% of those were instant payments, approximately tripling the 5.7% of instant disbursements made in 2020. Instant payments are gaining even on same-day account transfers, with 22% of consumers receiving disbursements by same-day automated clearing house (ACH) versus 20% who received at least one disbursement as an instant payment. Consumers are now 50% more likely to be aware of instant payments than in 2020, and they are 15% more likely to choose instant payments.

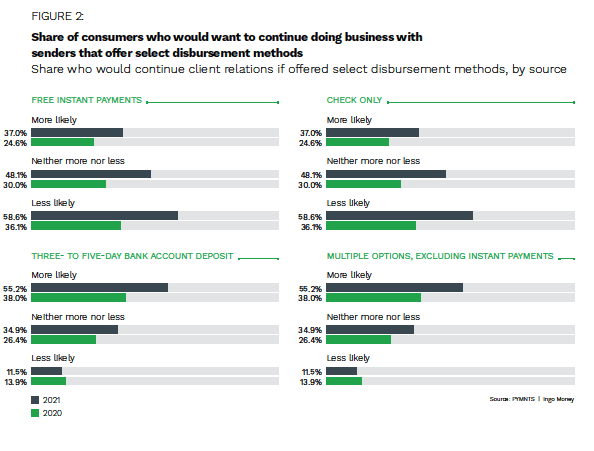

Businesses see the benefits of instant payments as well, and more than 75% want financial institutions (FIs) to offer faster payment options. Instant payments can improve cash flow management, make payment operations more efficient and contribute to more secure and accessible payments. Businesses can leverage instant payments to achieve better automated invoicing and remittance processing, resulting in fewer errors and exceptions. The combined benefits of instant payments can grow revenue while reducing overhead. Instant payments also can drive loyalty, and 66% of consumers said they would do more business with companies that offer free instant payment options.

Interest in instant payments does not always translate into understanding how these paym ents work, however. Most consumers said they believe instant payments do not provide instantly available funds, and 40% of small businesses said they would not switch to instant payments because they are relatively satisfied with their current providers. This month, PYMNTS goes beyond instant payments’ objective benefits and looks at how perceptions are shaping their development and adoption.

ents work, however. Most consumers said they believe instant payments do not provide instantly available funds, and 40% of small businesses said they would not switch to instant payments because they are relatively satisfied with their current providers. This month, PYMNTS goes beyond instant payments’ objective benefits and looks at how perceptions are shaping their development and adoption.

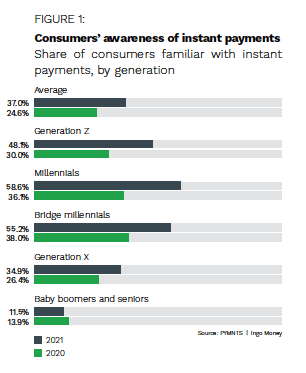

Consumer Understanding of Instant Payments

Most consumers know about payment platforms such as Zelle, Venmo and PayPal, but they may not understand how those platforms work. Instant payments made through Zelle can show up in a user’s bank account immediately, and 50% of consumers recognize that functionality, but 44% of consumers said they think that other apps such as Venmo, Cash App and PayPal have the same ability, although they do not. Consumers have a poor understanding even of ACH transactions, which have existed for decades, and many expect such payments to take up to five days to process, despite the potential for same-day ACH. Experience shapes perception.

FIs may lose ground to nonbank alternatives because consumers do not know how money moves. Those consumers may not see the value in instant payments, choosing instead to use platforms they perceive as most prominent or readily available. When consumers incorrectly believe a payment platform offers instant payments, their experience with it may cause them to think instant payments are not actually instant — 60% of consumers already believe instant payments take hours or days to process.

At every transaction, consumers are encountering a growing number of payment options, and 71% said they could choose between at least two options for receiving disbursements in 2021, up 23% from 2020. Many of those options are presented as instant, regardless of whether they really are. FIs that want to convince consumers of instant payments’ value must ensure consumers know the difference.

Making Business Sense of Instant Payments

Businesses recognize the  benefits of faster payments even more than consumers do, especially with 60% of companies citing cash flow management and working capital as top concerns. Three out of every four businesses with revenues ranging from $1 million to $250 million believe it is essential to offer faster payments. Most of those businesses also used some form of faster payment in 2020, but many of these were same-day ACH, push-to-card or digital wallet varieties rather than actual instant payments. Approximately two-thirds of firms said they would factor fast-payment options into their future banking choices.

benefits of faster payments even more than consumers do, especially with 60% of companies citing cash flow management and working capital as top concerns. Three out of every four businesses with revenues ranging from $1 million to $250 million believe it is essential to offer faster payments. Most of those businesses also used some form of faster payment in 2020, but many of these were same-day ACH, push-to-card or digital wallet varieties rather than actual instant payments. Approximately two-thirds of firms said they would factor fast-payment options into their future banking choices.

At the same time, 66% of microbusinesses and 60% of small businesses said they would not be interested in instant payments if it meant paying more than their current bank fees. Satisfaction with existing payment services also is enough to make 56% of microbusinesses and 40% of small businesses discount the benefits of switching to faster options.

Even such hesitant businesses, however, must appreciate instant payments’ potential to improve customer experience and loyalty. Two-thirds of consumers in a PYMNTS report said they would be more likely to continue doing business with firms that provided free instant payment options. Not being able to use their preferred payment choices also will leave 34% of consumers feeling disappointed or let down, and 46% are likely to feel anxious or stressed if they cannot use a payment method they consider secure. Customers demand trusted payment options, and for 53%, that means instant payments.

How both consumers and businesses perceive instant payments — and how well they understand them — will shape the future of these options. FIs should be prepared to communicate instant payments’ substantial benefits to both groups to drive their greater adoption.