The number of registered mobile money accounts grew 13% in 2020 to 1.2 billion accounts worldwide — double the expected growth for that period. The number of active accounts rose as well, with consumers using their accounts more frequently and for new and more advanced use cases. This all took place alongside an increase in transaction values, with the global value of daily transactions exceeding $2 billion for the first time ever. By the end of 2022, the global value of daily transactions is expected to exceed $3 billion.

Despite that growth, not all monetary transactions are as simple or easy as they could be, and users face restrictions even in moving money between accounts they own. Drew Edwards, CEO of Ingo Money, told PYMNTS that some modern money movements are the tech-enabled equivalents of removing money from one account through an ATM and traveling across town to deposit those funds into a different account. Today, those accounts are all accessed through a single mobile device, but moving money between them still requires overcoming barriers affecting both accessibility and processing time.

This month, PYMNTS Intelligence examines the challenges impeding money mobility for consumers and the concerns financial institutions (FIs) will need to address.

The Who, Where and How of New Account Openings

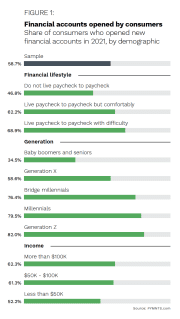

During 2021, 59% of U.S. adults opened a new financial account. Not surprisingly, Generation Z consumers, many of whom are just getting started in their financial journeys, led in opening new accounts, as 82% did so. Millennials and bridge millennials were not far behind, however, at 80% and 76%, respectively.

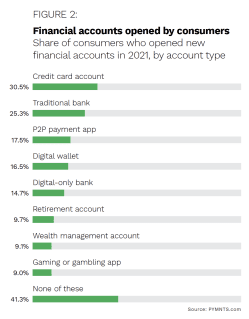

Credit cards were the top pull for consumers, with 30% of U.S. adults opening a new account for one in 2021. While 25% opened a traditional banking account, 18% created an account with a peer-to-peer (P2P) payment app and 17% opened a new digital wallet account. Just under 15% of surveyed consumers opened accounts at digital-only banks.

Digital still has a place even outside digital-only financial products, and 76% of new accounts opened in 2021 were opened using either a web browser or a mobile app. In addition, 41% of consumers said they were more likely to use digital channels to open a financial account in 2021 than they were in 2020.

Digital still has a place even outside digital-only financial products, and 76% of new accounts opened in 2021 were opened using either a web browser or a mobile app. In addition, 41% of consumers said they were more likely to use digital channels to open a financial account in 2021 than they were in 2020.

Getting Around the Money Mobility Obstacle Course

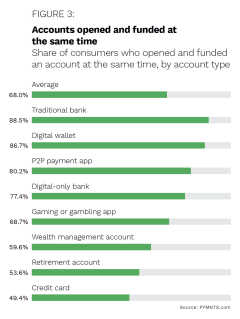

Even in opening all these new accounts, money mobility comes into play. The most common way for consumers to fund a new account was by linking it to an existing bank account, with 48% of surveyed consumers saying they funded a new account through these means. Even 80% of P2P payment accounts were funded as they were opened, with 59% of those funded by linking a personal bank account.

Whether funding a new account or transferring money between different accounts, consumers can encounter challenges and may have to get creative in how they move money. If the accounts are with the same institution, the task may be relatively simple, but even a credit card that bears the same logo as the FI where a checking account is held may be serviced by a separate company.

When consumers need their money to arrive reliably and on time, they may turn to other options, such as transferring money to themselves using a P2P app. They may also simply fall back on the familiar paper check. With modern mobile check deposit, users may be able to write a check from one account and immediately deposit it into another they own. This harks back to the analogy put forward by Edwards, though, and even raises some concerns about fraud for digital-only FIs. He pointed out in a separate interview that checks have become a fraud magnet and a particular concern for digital institutions.

FinTechs can successfully manage these risks, Edwards said, by giving consumers the opportunity to choose between making a deposit or paying a fee to have instant irreversible access. This makes check transactions safer because the consumer can choose to take the risk themselves for free or pay a fee and cover the costs necessary to ensure funds availability.

As consumers explore their options for financial accounts, many providers will be looking to stay ahead of the competition by making new account-opening smooth and easy. FIs also will not want to do anything that hinders consumers’ access to and movement of their funds among various accounts. For neobanks and FinTechs, the key will be to manage the fraud risk in a way that both keeps customers satisfied and minimizes the potential for bad actors to exploit the system.