Barely a week has gone by since the Fed “paused” its policy of hiking interest rates.

And the pause may prove short-lived — signaling some continued pressure ahead in the paycheck-to-paycheck economy.

In testimony being given Wednesday morning (June 21) before the House Committee on Financial Services, Federal Reserve Chair Jerome Powell said the rate hike campaign may resume later this year.

In his remarks tied to the Fed’s “Semiannual Monetary Policy Report,” Powell said that “inflation remains well above our longer-run goal of 2%,” adding that “the process of getting inflation back down to 2 percent has a long way to go.” And against that backdrop, there is the expectation that “it will be appropriate to raise interest rates somewhat further by the end of the year.” We note the fact that Powell has stated, too, that pretty much all Fed members see the need to raise rates.

Revolving Debt Rises — as Does Its Cost

The fact that the Fed members are traveling, arguably, in lockstep, toward higher rates comes as 60% of the population lives paycheck to paycheck. The pinch will be keenly felt with households carrying revolving debt. That debt becomes more expensive — and as Fed data showed earlier this month, revolving credit jumped at an annual rate of more than 13% into April. The Fed noted that credit card debt interest rates stood at more than 20%, up from roughly 15% just before the pandemic hit.

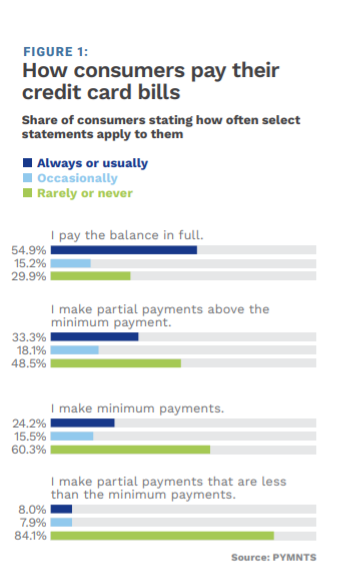

PYMNTS data show that fewer than half of consumers pay down their balances each month, which means that the revolving debt that they’re not paying down becomes more expensive as rates inch inexorably higher. Given the fact that 33% of cardholders, on average, increased their reliance on credit cards in the last six months, and just 15%, on average, decreased that reliance, the burden is mounting. The chart at right shows that only a third of consumers “always” make payments above the monthly minimum, and a significant percentage make only the minimum payment. The data show that about 16% of consumers always or sometimes make payments below the minimum threshold, which in turn hints at penalties and perhaps even a decrease in credit lines, adding to the pressures already being felt.

Elsewhere in his testimony, Powell addressed the topic of additional bank regulation. The banking system, overall, is “sound and resilient,” he said. But, according to Powell, “the recent bank failures, including the failure of Silicon Valley Bank, and the resulting banking stress have highlighted the importance of ensuring we have the appropriate rules and supervisory practices for banks of this size.”

The Fed’s Monetary Policy Report hints at some possible turbulence to come in commercial lending where our Main Street small and medium-sized businesses (SMBs) are concentrated. The Fed noted that that business financing conditions have been tightening, and stated, “Despite the increase in borrowing costs, credit quality has remained strong for most nonfinancial firms. However, some predictors of future business defaults suggest that defaults are more likely.”