What The Great Time Revolution Means For Consumers

The “Mighty Thor” was a household game-changer in 1908.

Invented by Alva John Fisher, Thor was the first electric washing machine to be mass-produced and sold. Until its debut, washing clothes was a tedious, time-consuming and very manual chore.

.jpg")

Image source: https://commons.wikimedia.org/wiki/File:The_Thor_Electric_Washing_and_Wringing_Machine_(captioned_advertisement).jpg

At the turn of the 20th century, few homes had running water or central heat. Doing the laundry required fetching water to fill big tubs, then heating the laundry over a coal stove. Clothes were then scrubbed by hand – a process that consumed roughly four hours of the typical American woman’s day at that time.

The Thor gave her back three hours and 19 minutes, since she could now do the laundry in 41 minutes.

Electric irons would soon follow, reducing the time spent ironing those freshly washed clothes from nearly five hours to fewer than two.

Those two devices – the electric washing machine and electric iron – gave women back more than six hours of the time they once spent doing the laundry.

In the early to mid-1900s, electricity would give women a new superpower: access to devices that saved them time doing basic household chores.

Electricity would also give innovators their own superpower, an incentive to design and manufacture a whole range of electric-powered appliances – irons, refrigerators, dryers, ovens, stoves, vacuum cleaners, dishwashers – that would do more than save women time “doing chores.”

These devices would help women shift time once spent on manual chores to higher-value activities, and shift some of those household duties to others in the family. Electricity, and the many electric-powered inventions it inspired, would democratize household chores by making it easy for any family member to pitch in, producing a predictably similar result.

The Connected Consumer’s Superpower

For most of the decade of the 2010s, smartphones and other connected devices, new technology, and the internet gave all consumers a new set of superpowers to save time, allowing them to allocate the time in which routine chores got done.

An on-the-go consumer could – and did – use mobile devices to refill a prescription while riding the subway to work, order groceries for delivery while cooking at home using a voice-activated speaker in the kitchen, pay bills using a mobile banking app while at lunch, order breakfast from the car on the way to the office for pickup, order dog food using an app while walking the dog, order a new pair of shoes to pick up at the store between meetings at the office, and shop for new clothes on a tablet before going to sleep at night. Mobile devices made it possible for consumers to compress time, and to complete routine activities while doing other things.

Over the last seven months, those devices and apps have given a much less on-the-go consumer two new superpowers: the chance to save time by moving physical routines online, and the ability to shift the days of the week once allocated to doing them.

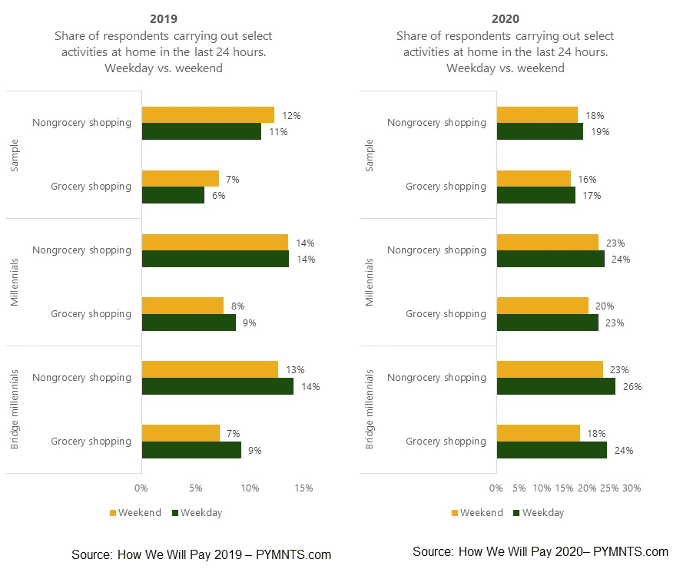

The fourth annual How We Will Pay 2020 study, done by PYMNTS in collaboration with Visa, paints a picture of a consumer who is using connected devices and apps to run the errands once done in the physical world on the weekends on the weekdays, using digital and digital-first channels.

This national study of 10,000 U.S. adult consumers conducted over a nine-day period between Aug. 15 and Aug. 23 also finds a consumer who is shifting many of the shopping and eating activities once done outside of the home during the week while on the go, to inside the consumer’s very connected, safe, touchless, now very home-centric commerce ecosystem.

This study, the full results of which will drop tomorrow, estimates that 43 million consumers who once shopped for groceries at the physical store on the weekends now shop for groceries during the week using digital-first channels.

This study, the full results of which will drop tomorrow, estimates that 43 million consumers who once shopped for groceries at the physical store on the weekends now shop for groceries during the week using digital-first channels.

Millennials and bridge millennials (32- to 42-year-olds) are the demographic cohorts who have most shifted the time and day of their grocery shopping. In just one year, we saw an increase of 167 percent in the number of bridge millennials who shop during the week for groceries, and 33 percent more consumers now buy on weekdays than on weekends using digital and digital-first methods, compared to 29 percent more consumers buying on weekdays than on weekends in 2019.

We observe the same pattern in shopping for retail products, with a year-over-year increase of 86 percent in the number of consumers shopping for retail products during the week. This is a demonstrable shift in an activity that most surveyed consumers once reported they did – and liked – as part of a social activity. In 2020, we also see that 13 percent more consumers buy retail products on weekdays than on weekends using digital and digital-first channels – perhaps troubling for retailers looking for in-store foot traffic from a consumer group with discretionary income to spend. This compares to only 8 percent of consumers buying more on weekdays than on weekends in 2019.

In the late summer of 2020, long after much of the physical economy had reopened, we now see a consumer who isn’t simply using apps and connected devices to save time or make the commerce experience safer by using touchless, digital channels.

Rather, we see a consumer who is now using them to realign how they spend the 24 hours in their day, and the seven days of their week.

Consumers are making these conscious decisions about when, how and where they perform their day-to-day routines, while also reporting that seeing family and friends is the one activity they both miss and value the most.

And getting out of the house – where they now largely spend 24 hours of their day, five days a week – has become an even higher priority on the weekends.

All of this points to the potential for innovators across the connected economy to unlock new commerce opportunities for a consumer with more time, more interest and the money to spend on developing an entirely new weekend routine.

Home Is Where the Economic Production Is

In 1934, economist Margaret Reid published a book titled “Economics of Household Production.” The book was based on her 1931 doctoral thesis at the University of Chicago. Her work, for the very first time, put a value on the contribution of women’s daily household activities in the overall economy.

Image Source: http://photoarchive.lib.uchicago.edu/rights.html

Reid wrote that the household is both the most important economic institution and the most neglected.

That’s important, she said, because the household is both a producer and a consumer of output.

Neglected, because that output is not easily measured by traditional economic metrics: Household labor is not paid, nor are the outputs of that labor sold.

In her book, Reid examined the economic impact of the work done by women in support of the household. She estimated that the economic contribution of women in 1918 to be 25 percent of U.S. GDP, which then was a whopping $61 billion.

Aside from quantifying the value of those household chores, Reid’s thesis posited that creating more efficiency in household chores would strengthen and improve the economic standing of women and their families.

She made the case that innovations in the way goods and services were produced and consumed inside and outside the household would give women more time to pursue different – and higher-value – activities. Reid cited the potential for innovations in manufacturing processes to free up women’s time by outsourcing basic household chores like baking and making clothes to third parties – and for the Industrial Revolution to produce devices that would further automate household chores once done by hand.

Reid’s work 89 years ago was path-breaking, and was the basis for an entire generation of work on the economics of time, and the costs and tradeoffs associated with how people spend it. It was only when Gary Becker began to pursue his own work on the economic theory of time allocation on human capital and the family structure in the 1960s was Reid’s contribution to economic literature on the importance of non-economic factors like household chores recognized. Becker would go on to win the Nobel Prize in Economics in 1992 for his work in this area.

Reid died 29 years ago in 1991, three or four years before eCommerce was even a glimmer in anyone’s eye, and 16 years before the world saw the first iPhone. She couldn’t have imagined, of course, the impact that those innovations – and others like them – would have on how all people are now able to spend their time, and the extent to which apps and devices have further democratized the day-to-day routine of getting household activities done, and the value of the time that is saved.

Platforms like Instacart, marketplaces like Amazon, and retailers like Walmart, Target, Home Depot, Kroger, Walgreens and CVS have made it possible for consumers to shift the time spent running errands on the weekends online, and to shift their purchasing patterns to digital-first channels any day of the week.

Consumers that once spent 60 to 90 minutes going to and from the grocery store on Saturday or Sunday mornings can now spend five to 10 minutes on a Wednesday morning using the grocery list stored from their last online visit.

Pharmacies prompt reminders for prescription refills and offer free delivery, avoiding the 30-minute (or longer) round trip to pick it up. Online pharmacies make that even easier and less time-consuming.

Food can be preordered for delivery from restaurants and restaurant aggregators, providing the certainty of the delivery window without the time spent driving to pick it up. Subscription services can put many of the items purchased in the center aisles of the grocery store on auto-refill – literally reducing the time spent shopping for cleaning supplies and pantry staples to near-zero.

We can also now put a dollar value on the time consumers save when they outsource those activities to apps, platforms and connected devices.

Instacart makes a point of telling its users how much time they have saved cumulatively every time an order is placed. Consumers do the mental math when deciding to pay a delivery fee to restaurant aggregators, and when using shopping aggregator platforms like Instacart and others – and when deciding whether to pay for a Prime or Walmart+ annual membership fee.

Consumers readily pay those fees because of the value they place on their own time, and the quality of the services they get when outsourcing those services to others.

But Will It Last?

Despite the continued use of digital channels to help consumers save time – and now, increasingly, shift how and when they spend that time – the question that remains unanswered is whether any or all of these digital habits will stick.

Many of them will – in large part because merchants are using digital technology as their own superpower, and are improving consumers’ digital-first experiences.

According to PYMNTS’ latest research on the consumer’s digital shift, reflecting a national sample of more than 30,000 consumers, the average consumer views digital-first channels – to shop for retail products and order food from restaurants using aggregators – as far better than they did in May. For grocery, consumers report that their digital-first and touchless experiences are now nearly twice as good.

Many of these consumers will stick to those habits, in part because it is likely that many will continue to have flexible work-from-home schedules.

Research from S&P Global Market Intelligence reports that 67 percent of employers say that some or all of their work-from-home practices will continue post-pandemic. A consumer who once could only shop for groceries on Saturday – because she was working Monday through Friday – can order and get groceries delivered during the week, and can use other digital retail channels to complete routine errands without cutting into precious weekend time.

As I have written many times before, it takes a lot to change consumer habits, and the pandemic has removed much of the inertia to doing physical world activities, like grocery shopping, online. Seven-going-on-eight months into the pandemic, many of those digital habits have become entrenched, and it seems unlikely that consumers will revert entirely, or even mostly, to what they once did.

Particularly since consumers now think it will be this time next year before they become confident reengaging in the physical world – and by then, those digital habits will become their routine. Superpowers provided by the apps and the connected devices have given consumers back their precious time.

Including how they spend their time on the weekends.

The most powerful innovations are those that turn the “I have to, but I don’t want to” activities into something that consumers no longer have to do, while giving them a better outcome. A consumer who once dedicated two hours every Saturday to shopping for groceries and putting them away, or running to the hardware store for the things needed to do projects around the house, has since found other, more valuable ways to use that time.

Margaret Reid would be impressed.