Just 58% of growth corporates in Central Europe, the Middle East and Africa (CEMEA) had been using working capital solutions, but that percentage is slated to grow to 95% in the coming months.

This is one key finding included in PYMNTS Intelligence’s “CEMEA Edition” of our 2023-2024 Growth Corporates Working Capital Index series, which was commissioned by Visa and examines working capital usage among growth corporates operating in CEMEA.

Growth corporates are those firms generating annual revenues between $50 million and $1 billion in the commercial travel, healthcare, agriculture, fleet and mobility and marketplaces sectors. Bigger than small and smaller than big, these firms are often making decisions that shape whether they will become the juggernauts of tomorrow. And PYMNTS Intelligence found that 77% of those that have accessed working capital solutions in the CEMEA region have seen improved business metrics and buyer-supplier relationships.

Yet, despite this success, CEMEA ranks fourth among the five regions we analyzed for our Working Capital Index (WCI) series. (The others were the Asia-Pacific region, Europe, Latin America and the Caribbean (LAC), and North America.)

However, growth corporates in the CEMEA region that actually tapped working capital solutions were most likely to report better metrics and relationships.

Still many growth corporates in the region are not taking full advantage of external financing solutions available in the market. This is slated to change, as growth corporates in the CEMEA region plan to increase their use of external working capital solutions in 2023, a 64% increase.

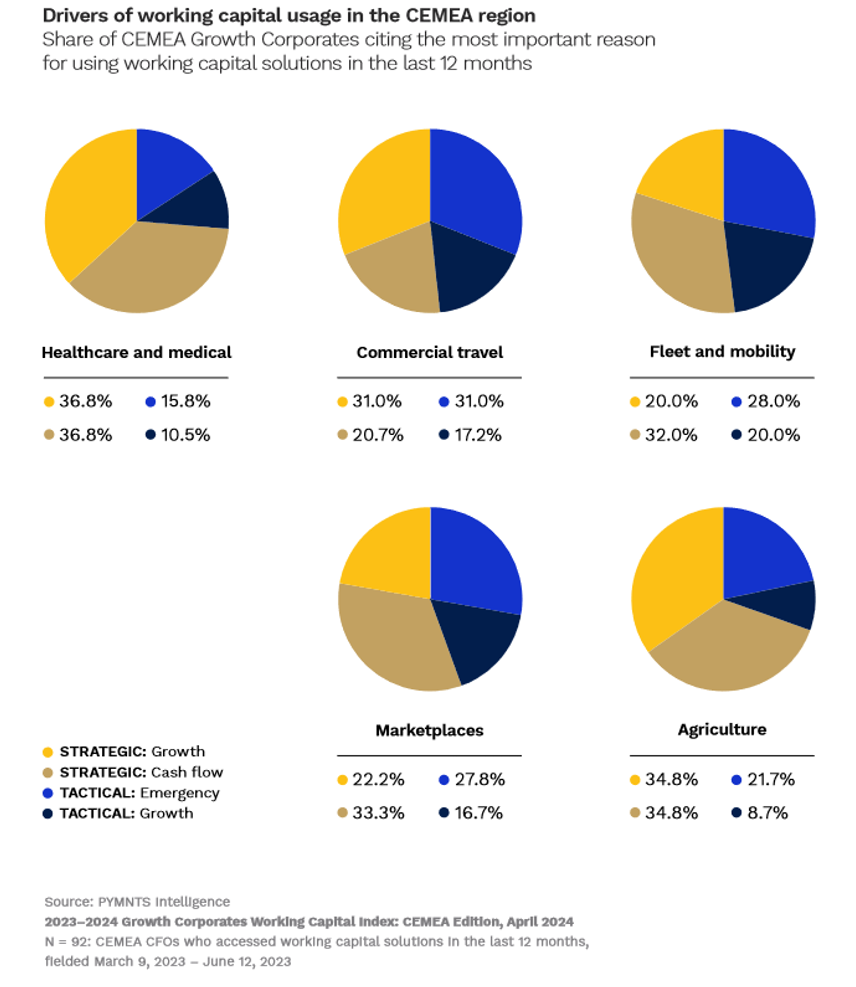

So, what were the drivers behind working capital usage among CEMEA growth corporates last year?

As the accompanying chart illustrates, 16% of healthcare and medical growth corporates said they were motivated by the need for emergency funding, while 37% of companies in that sector named both strategic growth and strategic cash flow needs as their main driver to access working capital. Thirty-one percent of those in the commercial travel sector identified the need to have tactical emergency cash on hand and funding for tactical growth initiatives. Strategic growth was also a major motivator for CEMEA growth corporates in agriculture (35%), the marketplaces segment (22%) and the fleet and mobility sector (20%).

As mentioned, these firms in CEMEA are expected to greatly increase their working capital use this year, suggesting that companies in the region that could not previously access working capital solutions are now intent on doing so. And although many growth corporates there were reluctant to access capital solutions, the reality that those that did reported significant improvements may be the final nudge needed for companies pondering using external financing solutions throughout 2024.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More