Mobile wallets have an excellent track record for generating a lot of hype in the payments ecosystem, but their pre-pandemic track record for use and consumer enthusiasm was decidedly mixed. While some wallets, most notably PayPal, did well for online transactions, consumers leveraging them in physical shopping contexts was limited at best.

But the entrance of the pandemic — and the emergence of the connected economy and the highly digitized consumer turning to digital means of performing essential and nonessential functions — has changed things. PYMNTS’ new report, How Consumers Live in the Connected Economy, indicates that mobile wallets have picked up a lot of prominence, particularly among the roughly 30 percent of consumers the study identified as “highly connected” — those who use digital tools on a regular basis to perform a substantial portion of their daily activities.

A More Digital Diverse Consumer Group

PYMNTS data suggests that the more engaged a consumer is with each of the eight pillars of the connected economy (working, banking, travel and fun, eating, shopping, health, home and social engagement), the more likely they are to have avidly adopted a variety of digital payment tools, including services like Apple Pay or Google Pay.

That’s not to say that highly connected consumers have abandoned their plastic cards en masse. Among the four main payment methods they tend to favor, credit cards still hold the top spot, with 80 percent expressing a preference for them. But mobile wallets are coming quickly from behind, with 65 percent of consumers choosing them. That puts them in a tie for second place with debit cards, while PayPal is in a class by itself, taking up third place with 62 percent usage.

That strikes quite a contrast to the “lightly connected” consumers, which heavily favor cards (credit and debit). In this segment, PayPal sees only 30 percent usage, while mobile wallets only collect 10 percent.

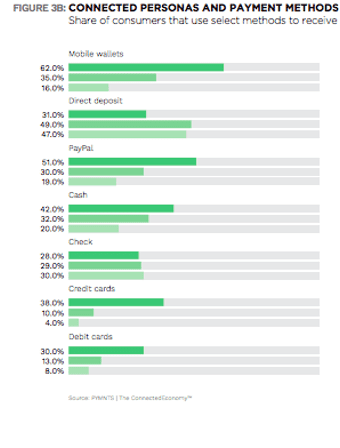

And the highly connected consumers aren’t just using mobile wallets more often than their less-connected counterparts, but they are also using them differently — not only to pay, but also to get paid. For example, highly connected consumers are more likely to report having been paid via mobile wallet than by traditional means, such as check or direct deposit. Some 62 percent of these consumers report that they’ve received payments via mobile wallets at least once over the past 12 months — more than twice the share that is paid via check or direct deposit.

Streamlining The Connected Experience

Moreover, the data demonstrates, mobile wallet providers have an opportunity to help customers better streamline and unify their experience of the connected economy, which is still a bit fragmented. PYMNTS data indicates that consumers want integrated, seamless experiences that do not require them to juggle multiple passwords and logins. At the same time, they want to feel confident that their personal and financial data is protected.

These are two areas that provide an opportunity for mobile wallet providers to dive in and help offer a smoother, more seamless, but also secure commerce journey — particularly as the same research indicates that consumers are more inclined to trust technology giants to build better, more unified connected commerce experiences.

Forty-three percent of consumers say they would trust Amazon to enable connected commerce opportunities, while 39 percent say the same about PayPal. The most trusted connected commerce enablers among super-connected consumers are Amazon (53 percent), Visa (46 percent), PayPal (44 percent), Apple (41 percent) and primary banks (35 percent). Thirty-two percent of consumers say they would trust banks to lead a connected commerce experience — still leading Apple’s 30 percent, but not by much.

Highly connected consumers are engaged in payment activities across online and physical channels. They also tend to receive payments from more sources than others, including employers (55 percent), family and friends (62 percent), merchants (41 percent) and healthcare providers (21 percent). They don’t lack channels or the enthusiasm to explore them. What they do lack, however, is a smooth, streamlined experience across the many channels of the connected economy.

Highly connected consumers are engaged in payment activities across online and physical channels. They also tend to receive payments from more sources than others, including employers (55 percent), family and friends (62 percent), merchants (41 percent) and healthcare providers (21 percent). They don’t lack channels or the enthusiasm to explore them. What they do lack, however, is a smooth, streamlined experience across the many channels of the connected economy.

And mobile wallets, particularly those offered by the tech giants that have vacuumed up so much consumer trust of late, might have an entry to use payments to build out that more unified experience.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More