Consumers aren’t just using financial apps to check on their last five transactions or send and receive payments. They are increasingly turning to their smartphones for handling a host of complex tasks — such as imposing spending controls on their children, keeping tabs on their spouse’s shopping spree, turning their cards on or off and requesting a replacement card. More importantly, they can do it all without calling into a call center.

Consumers aren’t just using financial apps to check on their last five transactions or send and receive payments. They are increasingly turning to their smartphones for handling a host of complex tasks — such as imposing spending controls on their children, keeping tabs on their spouse’s shopping spree, turning their cards on or off and requesting a replacement card. More importantly, they can do it all without calling into a call center.

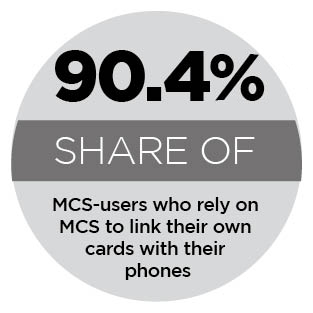

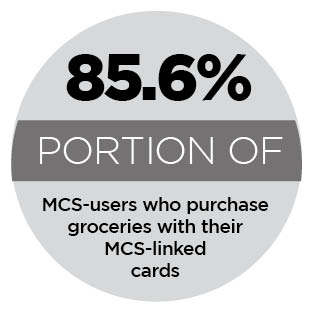

They are achieving all this with the help of mobile card services (MCS). MCS works by allowing consumers to link a digital version of their credit or debit cards to a mobile app. Now, 34 percent of card users are using MCS to set spending limits at certain stores, monitor how their children are using their cards or turn those cards on and off as they wish. In essence, MCS places the control over cards squarely in the hands of the consumers, rather than in the hands of a call center employee.

How does this stand to change the way consumers make card payments, though? Moreover, how are current MCS users leveraging their phones to enhance their shopping experiences?

How does this stand to change the way consumers make card payments, though? Moreover, how are current MCS users leveraging their phones to enhance their shopping experiences?

The Mobile Card Services Report, a PYMNTS and Ondot collaboration, sought to answer these questions, and more, by delving into the everyday spending habits of over 9,500 American card users — regardless of whether they use MCS.

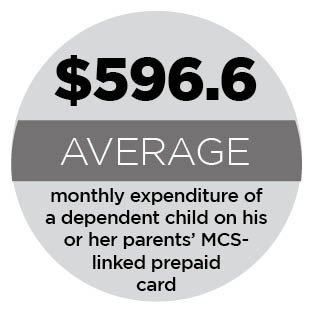

We learned that, for most consumers, MCS isn’t just useful for  managing their own cards, but the cards they provide to friends, family members and caretakers. For example, 78.5 percent of MCS users who link their phones to a card they gave their dependent child said it was “very” or “extremely” important to receive a text when their child uses that card. Meanwhile, 71.7 percent of people who gave an MCS-connected card to their spouse said they appreciated receiving automatic texts when that card was declined.

managing their own cards, but the cards they provide to friends, family members and caretakers. For example, 78.5 percent of MCS users who link their phones to a card they gave their dependent child said it was “very” or “extremely” important to receive a text when their child uses that card. Meanwhile, 71.7 percent of people who gave an MCS-connected card to their spouse said they appreciated receiving automatic texts when that card was declined.

For many, the appeal of MCS extends beyond automatic text updates.

To learn more about how modern consumers use MCS to enhance their purchasing experiences, click here to download the report.

See More In:

card payments, Consumer Spending, credit cards, customer service, debit cards, Main Feature, mobile apps, Mobile Payments, News, Ondot, shopping, Smartphones