As new ways to pay get introduced into the consumer market, there’s always one pressing question on the minds of merchants and issuers: How do consumers actually want to pay?

Well, according to TSYS’s latest study, the data shows that in the U.S. debit continues to be the king of payment methods, as consumers ranked it their most preferred payment type overall. But that trend is slowing. What TSYS’ study also showed is that over the past two years, there has been a decrease in consumers who say they prefer their debit card.

Or whatever they feel like using at their favorite merchants – and what merchants may incent consumers to use at their establishment.

Therein lies the tension – and complexity.

In general, merchants say they prefer that consumers pay with debit cards. But some merchants in TSYS’ study said they prefer credit card and cash over debit. And then there’s mobile commerce options, for which the data shows relatively low adoption. TSYS’ study — the 2015 U.S. Consumer Payment Choice Study — examines this to show what type of spending dominates, how loyalty and rewards play into the mix, how mobile banking app adoption is trending among consumers, and what cardholder communication preference is among those surveyed (1,000 U.S. consumers).

“We observed a narrowing in the number of respondents who prefer to use their debit card over their credit card. This year, 41 percent of survey respondents preferred debit when given a choice versus 35 percent who preferred credit,” TSYS’s results revealed, citing that “the reduction in debit appears to be due to respondents preferring cash and PayPal or other alternative payments at a higher rate.”

But the preference from consumers also varied by types of merchants. When making everyday purchases, debit was listed as the top consumer preference. Credit was listed as the top for online purchases or when making discretionary purchases. Cash was listed at the top for small dollar purchases.

“The takeaway from this year’s study shows debit continues to be the most preferred payment type overall, although in the last two years of the study, we have seen a decrease in the percentage of consumers who prefer to use their debit card. For certain merchant types, respondents indicated that they prefer credit cards or cash over debit cards. Mobile continues to gain traction, with consumers particularly interested in using the technology to view account activity and manage fraud,” the TSYS study concluded.

And then there’s loyalty and rewards, which are shown to play a strong role in driving consumer behavior — as well as impacting their payment choices. The survey’s results show that 58 percent of respondents have a rewards program attached with their preferred payment method type. Of those who said they preferred credit card, it was because of a rewards program associated with that card.

Moving toward the use of mobile devices and consumer payment preference, TSYS’s data showed that consumers still turn toward digital services more for financial management and protecting finances than to actually make payments.

“As mobile payment offerings increase, there remains an opportunity to accelerate the adoption of the payment services. According to our survey responses, mobile applications provided by financial institutions are highly adopted and frequently used. The respondents to our survey most often used the financial institution mobile app to verify balances and view recent transactions. In order to increase mobile adoption in financial services and payments, it is important that industry participants understand how consumers are using their devices today and how they are interested in using the devices in the future,” the study concluded.

I n terms of making a payment via a mobile app, the survey figures showed that most consumers haven’t made a purchase using a mobile device, and that many were never planning to do so.

n terms of making a payment via a mobile app, the survey figures showed that most consumers haven’t made a purchase using a mobile device, and that many were never planning to do so.

The number of respondents who said they prefer to use PayPal to pay increased to 14 percent in 2015, up from 12 percent in 2014. These figures, however, are down from the results of the 2013 survey, when 22 percent of respondents said they preferred to use PayPal when shopping online.

When asked about mobile banking preferences (which tended to be the top reason why consumers were using their smartphone for finances), a majority of consumers said they used mobile banking apps to verify their balance (86 percent). Seventy percent listed to verify recent transactions, 44 percent to transfer funds, 43 percent to make bill payments, 39 percent to make deposits, 14 percent to contact customer service and 11 percent listed verifying investments.

Despite the number of consumers who are turning toward digital and mobile options for their financial needs, there is still interest in having financial institutions provide strong communication. The survey results showed that they do rely on email as their most popular way to interact for communication methods. Respondents also said they prefer to receive communication roughly once a month with their financial service provider.

“Although our respondents prefer email, the majority have not asked their financial institution to stop sending paper statements. Results indicate that it is important that financial institutions understand consumer communication preferences so they are able to effectively engage current and potential future customers,” TSYS noted in its report.

The survey respondents indicated that they would most likely like communication from their bank once a month (43 percent), with 20 percent saying they’d like that communication to be once per week. Twenty percent also said they wanted to decide how often and 12 percent said they’d never like to hear from their bank. Still, when asked about asking the bank to stop sending paper statements, 55 percent of the respondents said they hadn’t.

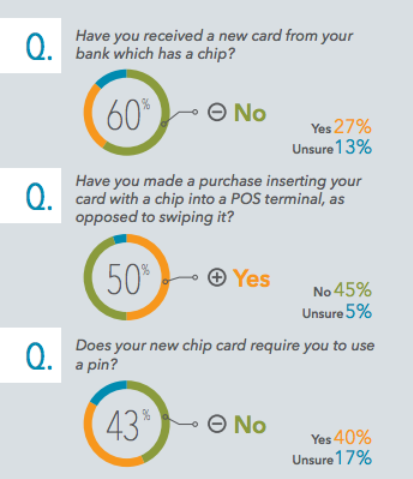

Trending back along the lines of how consumers are actually paying, TSYS’ study also dug into the use of chip card migration across the U.S. With the liability shift now more than two months behind, TSYS gathered data from consumers about chip cards, including if they have received the cards and if they have used them.

“The uncertainty in the answers from our respondents concerning chip cards supports other industry findings concerning the importance of consumer education around chip cards and their use. This need for education will continue as chip cards are more widely distributed and more chip point-of-sale terminals are enabled,” TSYS concluded in its report.

The report underscored that the rollout of chip cards in the U.S., along with the adoption of mobile services, is key data that FI should use in order to better understand consumers’ knowledge of the industry — as well as interest in adopting new offerings and technologies in the market.

“The majority of our survey respondents have yet to receive a chip card and some respondents were unsure if they have received one. Half of survey participants who have received a chip card said that they have used the card by inserting it into a POS terminal as opposed to swiping the card — and again some respondents were unsure if they have made a purchase by inserting their card,” TSYS reported.

“We believe that there needs to be a strong and continued focus on consumer and merchant education,” TSYS stated in its report.

“The payments industry continues to evolve quickly through innovation and the availability of new products. Companies that have not traditionally participated in payments are also looking at the industry as an opportunity for both growth and a more robust customer experience. We believe the expanded consumer choices will help drive the progress and innovation of payments,” TSYS’ study concluded.”

How Canadian Consumers Choose To Pay

Slightly different than in the U.S., the top preferred payment method in Canada was listed as credit cards, with 46 percent of respondents listing that as their top preference (that was up from 45 percent in 2014). Debit card preference rang in at 34 percent (up from 33 percent) and cash was down to 14 percent from last year’s 19 percent.

Canadian consumers showed strong interest in mobile adoption and being engaged digitally. Of those surveyed, 29 percent reported being highly interested in using a mobile phone for having the ability to stop an unauthorized transaction. And the percentage of respondents who wanted to view transactions with a card was 25 percent.

“The first difference we noted between our Canadian study and the U.S. study has to do with those payment preferences. When Canadian consumers have both a credit and debit card, they tend to prefer the credit card as their most preferred payment card. But in the U.S., that is reversed. We have found in the past that U.S. consumers have a preference for debit when they have both cards available, although this is narrowing and we are very interested to see what the U.S. study will show in the fall. Those preferences are even wider when we look at a couple of categories like grocery stores and gas stations, where in the U.S. those types of purchases are very heavily debit,” Sarah Hartman, Senior Director of Consumer Payment Solutions at TSYS, told PYMNTS in an interview about the study.

Like in the U.S., consumers showed strong interest in having communication from their banks with 47 percent of respondents saying that they wanted to receive coupons or special offers from their banks based on their purchasing behavior. On the mobile banking side, adoption was also strong, with 24 percent reporting that they use a mobile banking app from a FI at least a few times a month.

“The second area where we were a little surprised with the Canadian survey was in relation to different mobile features. U.S. consumers expressed a slightly higher level of interest in some of the mobile offerings. Both groups — U.S. and Canadian consumers — tend to prefer mobile features like inquiries and services over payments, at least for now, but we all know the mobile payments space is continuing to grow,” Hartman said.

Rewards were also a key driver of cardholder behavior for Canadian consumers, with 31 percent reporting that reward features (immediate discounts/cash back rewards) were valuable to them. As TSYS’ study noted: “For consumers with multiple credit cards, access to rewards incented them to use one card more than another.”

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More