Despite the nearly continuous drumbeat of doom and gloom from the world of physical retail, there is, according to Affirm CRO Rob Pfeifer, something of a curious side phenomenon unfolding at the same time: Online brands – famous and famously successful online brands – are branching out into physical retail.

“Brands are moving to the real world for a reason,” Pfeifer said. “Physical stores, they work when they are done right.”

And as retail is becoming more of seamless, single channel, Pfeifer noted, even the world’s most recognizable online brands – like Everlane and Pop Box – dip a toe into pop-ups, open stores in major metros (like Warby Parker) or even buy big physical brands (think Amazon and Whole Foods), the writing on the wall for an online retail lender like Affirm was clear.

Time to branch out into brick-and-mortar stores.

Affirm InStore launches today, and – as Pfeifer told Karen Webster in a pre-launch interview – that means taking what’s made Affirm successful online and extending those benefits to both consumers and merchants in a new, in-store channel.

“Affirm InStore is about giving merchants and consumers an easy way to get more people through the checkout flow,” Pfeifer explained, adding that consumers get a transparent POS credit alternative with no hidden fees and an easy-to-use mobile experience that provides a pre-approval based on what they can afford to spend before making a purchase.

For merchants, Pfeifer said, it’s a remarkably easy integration experience, particularly given the typical challenges of integrating with any in-store POS system, which he noted weren’t as “out of the box” ready as they were for many of the online merchants they serve.

Then there was the added challenge of ensuring that the experience for the consumer and the merchant was as omnichannel as the buying process now is for consumers.

Finding InStore Credit’s Lowest Common Denominator

Affirm InStore’s launch merchant is Simply Mac, an authorized retailer and repairer of Apple products with roughly 50 stores nationwide. When working with them, Pfeifer said it became clear that trying to figure out integrations for the universe of POS options was a very heavy lift – and too far and too long from delivering the seamless experience Affirm wanted for their merchants and end consumers.

Defaulting to the lowest common denominator in a brick-and-mortar store – the physical card – did nothing but add an unnecessary level of complexity all the way around.

Instead, Pfeifer and Affirm defaulted to what is now the lowest common denominator for every consumer who shops: the mobile phone. And for every merchant: in-store promotional material.

And put them together to create a POS credit option that allows consumers to get pre-qualified for credit before walking up to the register to check out.

The New Customer In-Store Credit Journey

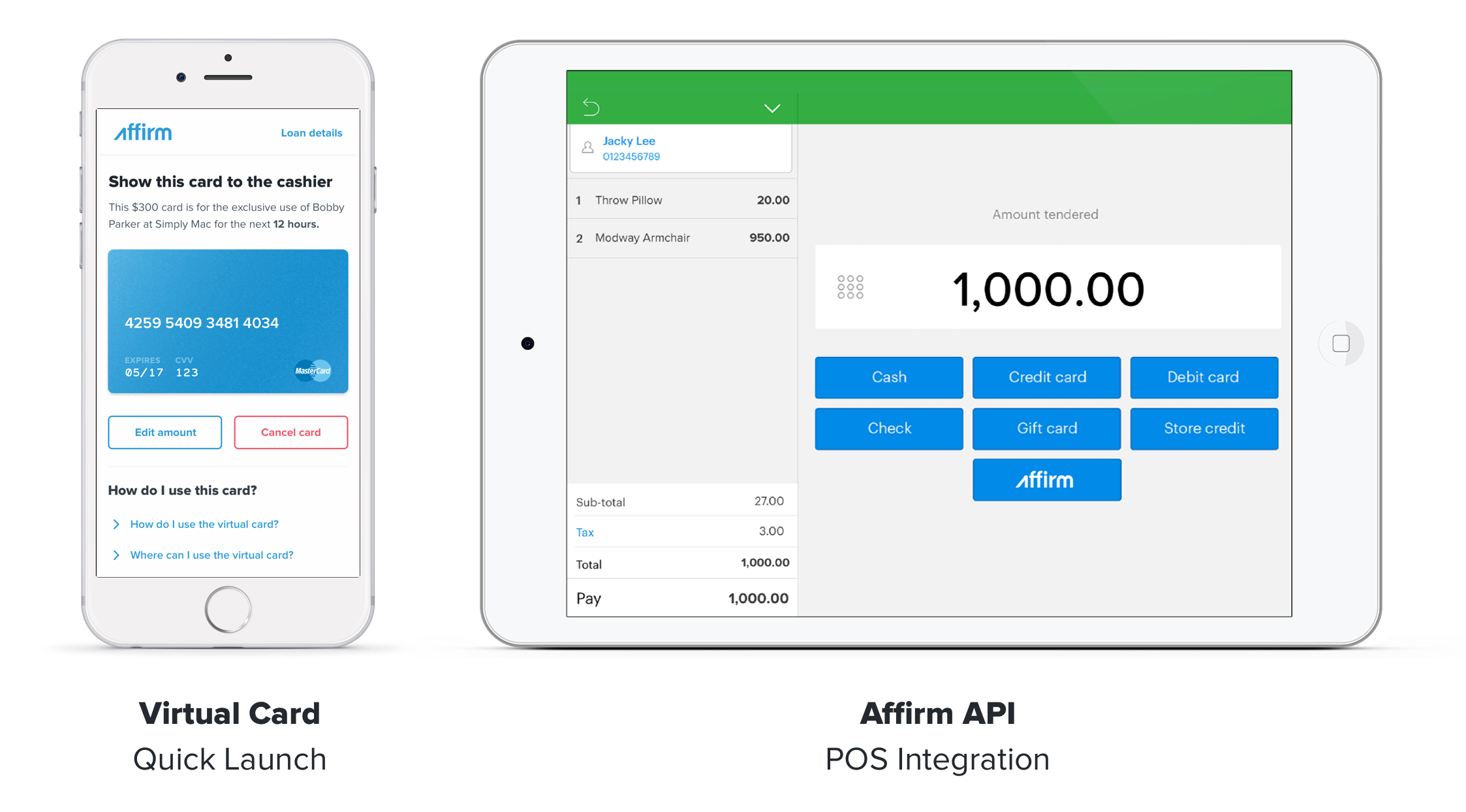

Brick-and-mortar customers will see Affirm InStore and the merchant’s co-branded materials displayed strategically in and around the store, cueing them that an alternative form of credit is available.

Consumers are prompted to text a merchant-specific code that returns a link to a simple Affirm application with four to five questions. A pre-approved amount and term – currently three, six or 12 months – is returned with the terms and conditions spelled out.

When it’s time to check out, the consumer uses her Affirm app to enter the purchase amount. At that time, a virtual card is issued and appears in her app. The store associate keys in the virtual card number (which is an instant issuance card running on Mastercard rails) at the POS in exactly the way they would key in a credit card number. The customer checks out with the good or service, the merchant gets paid and from there, Affirm manages the repayment process with the consumer.

But suppose that same consumer needed to go home to measure the space for the new Peloton they might want to buy, or confer the details of a computer’s key specs with her spouse or partner at home, and didn’t feel comfortable buying in the store right then?

The Affirm InStore pre-approval follows the consumer to the online touchpoint so she can complete the purchase from the merchant’s website at home.

“That’s a win for the customer, who gets more of what they want,” Pfeifer said. “And of course, it’s a win for retailers, who get to sell more goods to their customers.”

The consumer wins big too, Pfeifer said. Just like Affirm online, the pre-approved amount is what she will pay. Transparent financing is the firm’s ethos, something that Affirm’s CEO and founder Max Levchin emphasized in an interview with Karen Webster last year. Customers who know precisely what they’re paying are happier – and more loyal, Levchin emphasized – because they know that what they have been approved to spend is what they can afford, and that the amount of their monthly payment will be consistent over the term of the loan.

“We tell merchants that we will never charge any late fees or retroactive fees; these gimmicks aren’t okay with us and shouldn’t be okay with you, either,” Levchin said then.

That transparency, Pfeifer noted in his conversation with Webster, combined with the ways the customer is prompted to change the order of operations in their shopping experience, often brings a benefit to the merchant in the form of larger basket sizes.

“Working with Affirm gives merchants the ability to nudge their customers to apply for credit earlier in the buying cycle,” he said. “They will get approvals with very clear terms – and that means the consumer can adjust how they are thinking about what they are buying.”

Since turning to Affirm InStore, Simply Mac has seen a 20 percent increase in basket sizes, a 63 percent rise of in-store applications and a 34 percent boost of in-store approvals. Plus, nearly 81 percent of the brand’s total online sales are coming from Affirm.

Giving Retailers Honest Credit Options

Pfeifer said that for the Affirm team, the hardest thing about bringing Affirm into the physical store would be deciding where to put the signs to promote it.

Integrating with Affirm InStore, he said, is reasonably simple. For enterprise-level merchants, it’s a 50- to 60-hour process – and more like 20 or 30 hours for most firms, assuming they are using a modern POS system.

“There really isn’t any direct integration of Affirm into the in-store POS – that is all handled via the smartphone – so we are really training associates in the use of the app,” Pfeifer said. “And most retail clerks are fairly familiar with how to enter credit card numbers into a POS terminal.”

Once those signs are up, he noted, Affirm hopes to begin really delivering on what Levchin promised with that last fundraising round: a bigger boost for their merchant partners by allowing consumers to participate in a credit underwriting experience that they not only like, but enthusiastically embrace.

Pfeifer said that Affirm’s risk models are built on an approve/deny model with a goal of approving everyone – but at a level they can afford. That, he noted, helps consumers build the kind of relationship to credit that, over time, allows them to borrow more, in a responsible manner.

When asked by Webster about Affirm’s potential to significantly marginalize the branded store card model – despite their promise of rich rewards, perks and other “free” benefits to consumers – Pfeifer noted that some of their business partners have decided to drop their branded card in favor of Affirm’s offering, while others continue to offer both – at least for now.

“We want to make it obvious to consumers that they should choose Affirm,” said Pfeifer, noting that the best way to do that is to make customers feel confident that they are getting the fairest and clearest financing deal available, with no bait and switch on terms or costly interest charges that inflate the cost of goods purchased.

“The mindset we want in customers is that they should just pick Affirm,” he said, adding that helping consumers learn how to use credit responsibly is perhaps the biggest reward for both consumers and merchants.