Paying the bill used to be something you did at the end of a journey, or an interaction, or when an agreement had been struck — a fixed moment in time where funds changed hands.

Now payments are an experience, or are woven so tightly into the fabric of customer/business relationships that they’ve become invisible.

It might be cliché — just a bit — to think of Uber and Amazon as the yardsticks and aspirational benchmarks here. But then again, the intuitive transactions that are well-stitched into the mix, across hardware and software, mobile devices and voice activated assistants show that financial services need not be conspicuous.

Embedded finance is not just a consumer-facing phenomenon. It promises to change the ways in which B2B payments are done, and opens up a whole new avenue for banks serving their corporate clients.

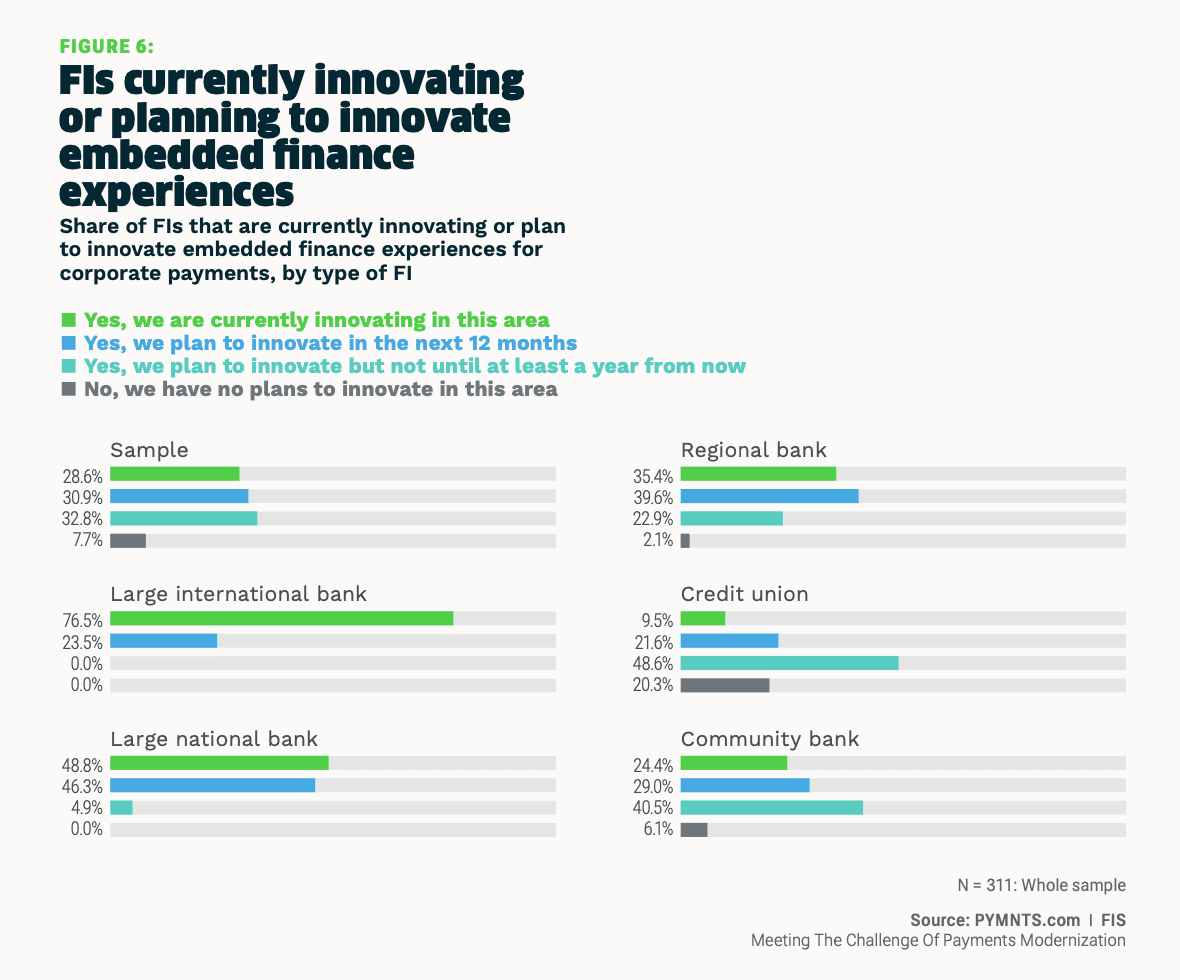

The whole-hearted embrace by financial institutions (FIs) to embed finance into their own offerings is illuminated by recent PYMNTS data that show that 9 out of 10 FIs are in the midst of, or plan on, giving embedded finance solutions to help modernize B2B payments. In terms of the low-hanging fruit, more than half of these FIs are embedding payments processing, with larger FIs setting sights on embedded loans and cash flow management as other areas for innovation with their clients.

Read more: Data Point: 92% of FIs Are Innovating or Plan to Innovate Embedded Finance Experiences

The greenfield opportunity is there, certainly in terms of providing the tech that B2B payments need to get more firmly rooted in the 21st century. PYMNTS has found that 42% of companies have pointed to a lack of supplier portals — typically third-party platforms that enable them to connect online with their suppliers or vendors — as a pain point in their B2B payment processes.

The Demographic Shift

Perhaps no surprise: Some demographic shifts are giving rise to embedded finance — and the demand for it.

PYMNTS data show that the workforce is skewing younger — and that, at present, nearly three-quarters of working United States millennials are now involved in their companies’ purchasing, operational and organizational decisions. And, increasingly, they are taking their cues as to what finance should be like from their daily B2C experiences (there’s that nod to Uber and Amazon again).

Read more: Millennial, Gen-Z Digital Preferences Reshaping Embedded Finance Landscape

There are any number of firms that are grabbing onto the opportunity to digitize and embed banking services into new channels and fashion new experiences. In just a few examples, where traditional FIs and FinTechs are converging and partnering:

Software-as-a-service (SaaS) banking platform Mambu and FinTech Brim Financial teamed up on a digital banking, deposit, lending and cards platform across the U.S. and Canada. Those joint efforts would enable virtual cards and digital payments including Apple Pay, Google Pay and Samsung Pay, to be integrated with Mambu’s platform.

Read also: Mambu, Brim Financial Team on Digital Banking, Embedded Finance Platform

Elsewhere, FinTech Alviere is partnering with card issuer Marqeta in a bid to enable enterprises to issue branded cards to their end users.

See also: Embedded Finance FinTech Alviere Inks Deal With Card Issuer Marqeta

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More