Banks may feel pressure to match Apple’s offering of higher savings rates with a Goldman Sachs savings account than most institutions as the tech giant makes inroads into banking.

Americans have been hesitant to break up with traditional financial institutions (FIs) for years. Reasons have ranged from the convenience a brick-and-mortar location may offer to the trusted reputation many of these banks hold. However, a significant behavioral shift seems to be taking place. Consumers, choosing to no longer let their money sit in low-interest savings accounts, are moving their savings toward neobanks, FinTechs and others who can offer more.

And Apple’s recent announcement may prompt consumers to switch. Few entities have the resources of Apple. Continuing to make banking inroads following its Apple Pay Later announcement, the tech giant is partnering with Goldman Sachs to offer Apple Card holders a savings account with a 4.15% rate. With the planning stages first announced in October, savings accounts offered through this partnership will have no fees, minimum deposits or minimum balance requirements.

This makes Apple’s most recent announcement perfectly timed — for consumers. It may mean trouble for digital banks, as this competitive entry may draw depositors.

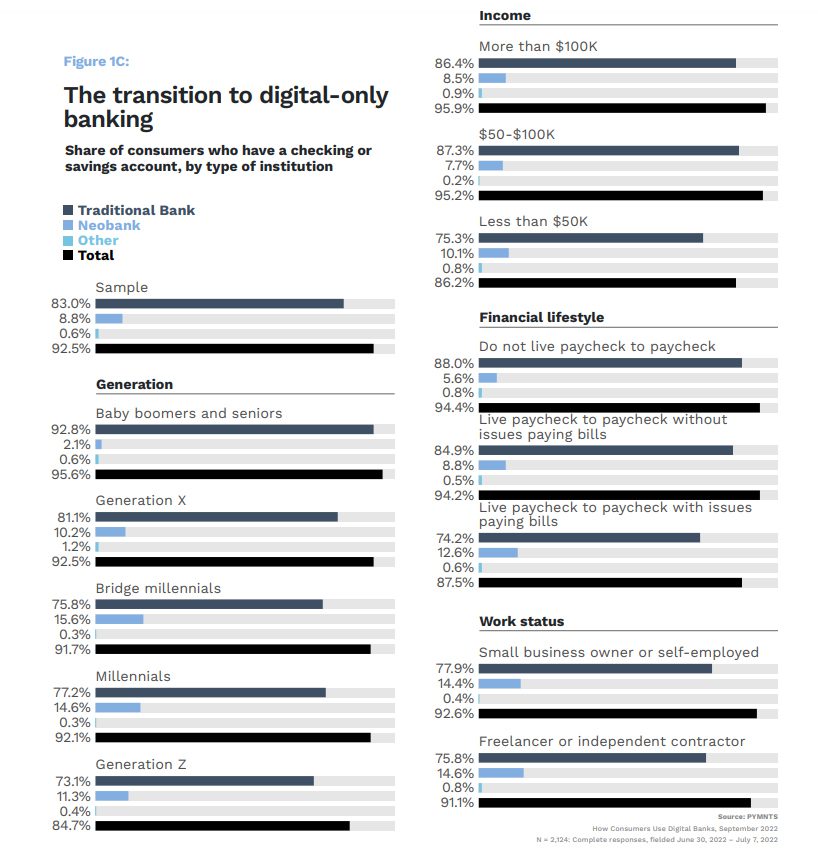

Neobanks have clawed their way into the picture, although getting consumers to move from traditional banks towards all-digital and similar solutions didn’t occur overnight. Consumers’ migration towards digital banks and digital banking overall is noted in the PYMNTS collaboration with Treasury Prime, “How Consumers Use Digital Banks.” It found that 8.8% of consumers hold a checking or savings account with a neobank, and more than 10% of all generations except baby boomers and seniors have such accounts.

Apple’s aggressive offer means that this consumer interest may be overtaken by a different type of interest: interest rates. Higher account interest rates may prove to be a primary concern moving forward as the cost of living seems to persistently outpace wages.

Indeed, in the wake of the banking mini-meltdown, traditional FIs began raising their interest rates on products such as CDs to keep depositors from leaving. Small banks, with less revenue cushioning to offer the same rates, saw their customers pull $109 billion from these institutions before catching up with their own rates. And, even these higher rates haven’t made bigger FIs impenetrable, as the top four U.S. banks lost a combined $52 billion overnight in March due to investor concerns over unrealized securities losses.

While these gains and losses in the short-term benefit bigger banks, the gap isn’t healthy for the sector overall. In an interview with PYMNTS’ Karen Webster, partner at QED Investors Amias Gerety explained the importance of deposits in banks of all sizes and the importance of community institutions in the tech industry. “It shouldn’t be the policy of the United States that we only want deposits in the 25 largest banks. I hope the policy debate is less about finger pointing and more about what type of banking system we want, and the policies we need to get there… With community banking, we can see the flowering of bank FinTech startups that are properly capitalized and properly scaled to become sustainable.”

The sector instability Gerety details may be behind consumers’ shift toward FinTech banking. Consumers increasingly store money in apps, and Apple’s recent savings announcement could shift behavior further.

Will Apple lead the mass movement away from traditional banking? Right now, it is hard to say — but the tech giant may be the player to beat in the still wide-open non-bank banking space.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More