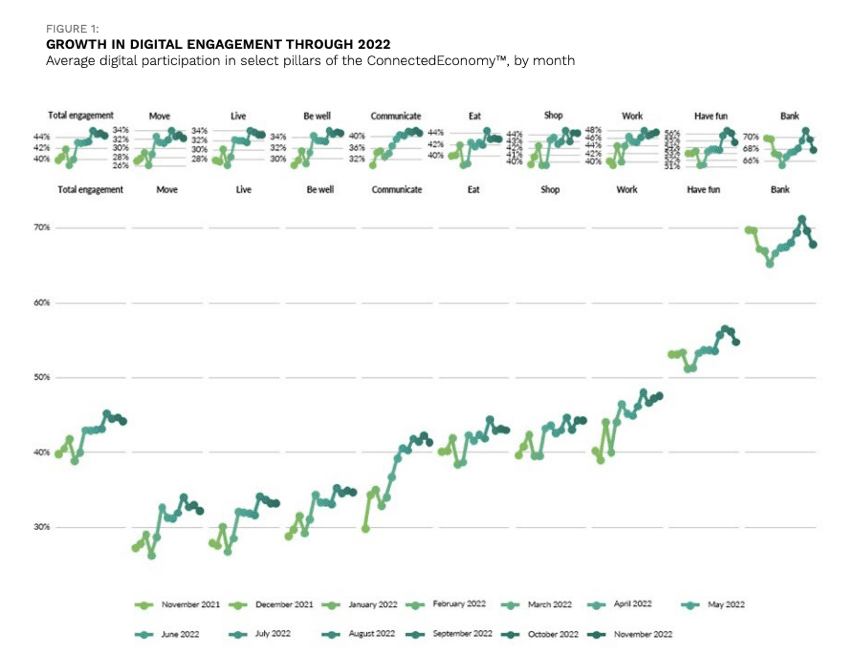

This, as the penchant for digital commerce and related connected economy activities, showed that consumers were now 10% more likely to engage with devices and digital channels to perform everyday tasks from shopping to messaging to booking travel than they were a year ago.

This, according to PYMNTS’ year-end study “12 Months Of The ConnectedEconomy™ “which revealed that consumers’ use of digital tools — leading to engagement with yet more connected activities — has increased and is becoming more commonplace as it blends into our daily routines.

Per that study, “By November 2022, consumers were participating in remotely working online 10% more than they did one year prior. They were also 18% more likely to use travel and commuting apps such as Uber and Airbnb and 19% more likely to use digital assistants to organize or assist with household chores.”

Perhaps more telling is that more than four in 10 consumers went online to buy a retail product in November 2022, which is 12% higher than 12 months before. This was despite the rush of consumers heading back to brick-and-mortar stores as COVID restrictions vanished.

That throng of in-store shoppers didn’t do much to impede online ordering and delivery: In fact, by year’s end, 131 million U.S. consumers were averaging online retail purchases and deliveries every month, according to PYMNTS data.

Get the Report: 12 Months Of The ConnectedEconomy™

Shortages and Excesses

Meanwhile, rolling product shortages kept consumers and merchants on their toes for most of 2022 and are still dragging on in pockets of retail today. It’s a problem that saw shoppers turn to digital tools to find a clever workaround to replace needed items or to locate a place that might have a few left in stock.

As PYMNTS reported, within Google’s “Year in Search” report, a long list of different “shortages” could be found, including queries for suddenly scarce things like baby formula, sriracha, cream cheese, avocados and lettuce.

As the Walmarts of the world automated vast supply chains to ensure more in-stock positions, grocers of considerable clout — but not Walmart-sized clout — took issue with suppliers.

In a PYMNTS interview, IGA (Independent Grocers Alliance) President and CEO John Ross said being treated as the back of the line “creates an adversarial relationship with our suppliers. It’s very emotional. So, getting back in stock, getting back to normal terms might mean reducing our top line.”

As big a story as shortages was in 2022, ironically, excess inventories in certain categories also commanded headlines in a strange case of too much over here, too little over there.

We reported on Dec. 29 that “This year has seen Target struggle to deal with high inventory levels, but the company is far from alone on that score. Inventory bloat led both Target and Walmart to launch their holiday sales earlier than normal.”

That story also noted that, for its part, bellwether Walmart felt it’s dealt with the oversupply issues of 2022 adequately: “Walmart’s executive team said that its efforts to reduce inventory had gotten to the point where it expected not to have to discuss the issue. The company’s third-quarter inventory was up just 13% versus the year before, a move representing a 10-percentage-point improvement from the previous quarter.”

This was a boon to deal-chasing digerati who cashed in on markdowns like never before, even as trade-downs and belt-tightening dominated consumer spending this year.

Creditworthy But Cautious

Adding more topsy-turvy to the story are the spending habits of consumers with solid incomes and good credit scores, who began intentionally pulling back purchases, perhaps readying for recession.

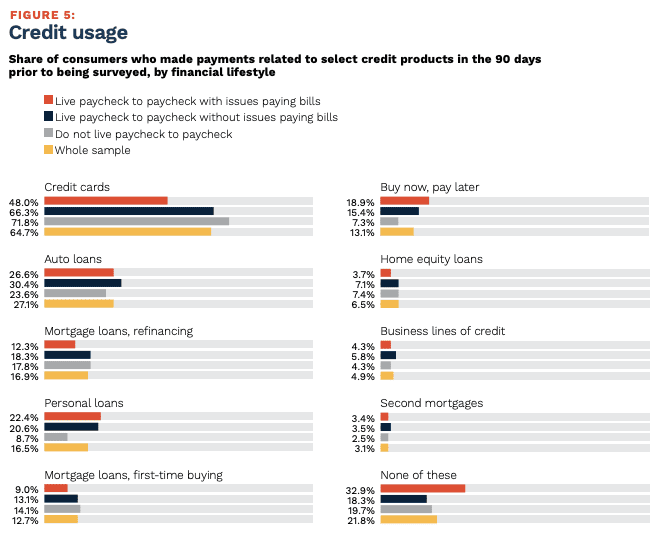

In the report New Reality Check: The Paycheck-To-Paycheck Report: 2022 Year In Review, a PYMNTS and LendingClub collaboration, credit usage among those with open credit to buy was down slightly, suggesting that even those that can spend are not doing as much of it.

“Consumers living paycheck to paycheck average fair to good credit scores, according to our data. Paycheck-to-paycheck consumers without issues paying their bills average a credit score of 689, while those struggling to pay bills each month average a score of 615. Still, 32% of paycheck-to-paycheck consumers with issues paying their bills have not paid for a credit product in the last three months, indicating that these consumers are more apt to be perceived as a liability.”