At first glance, it might seem incongruous to mention the PYMNTS FinTech IPO Index and banks and M&A in the same sentence.

The index itself is up 32% year to date. And so the logic might follow that if stock is currency on Wall Street — deal making would involve buying up that stock — then the shares have been getting more expensive. All manner of companies (and, it should be noted, private investors, too) are cautious on costs, and how and where they deploy capital.

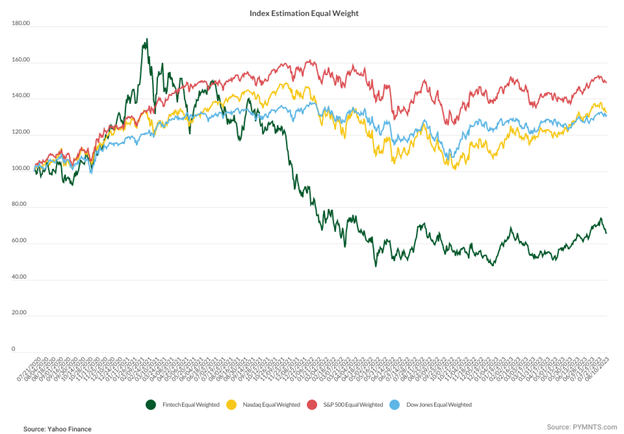

But a bit of a deeper dive reveals that even with the notably positive returns year to date for the index, the 2023 rally has been coming off a relatively low base, and the chart below details the significant underperformance logged by the index — marked by more than 40 companies — against broader market measures.

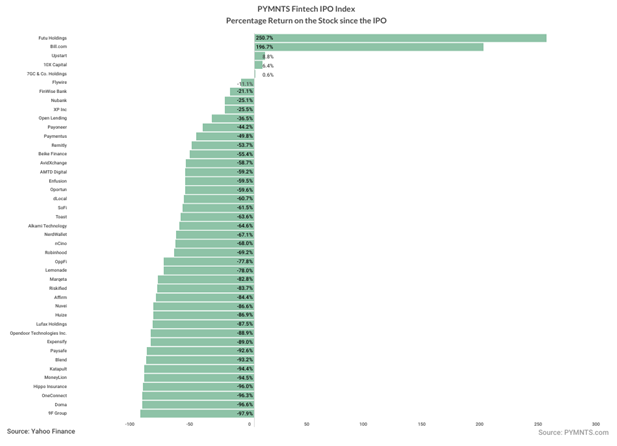

Zeroing in on the individual performers, we can see that, in fact, only five names have generated positive share price performance since their respective IPOs, with the vast majority of the field trading as “busted IPOs,” where the stock changes hand well below the initial offer price marked on the first day of trading.

In fact, the average return for the names that were negative, or at best flat, shows a dismal decline of more than 62%.

A significant number of platforms that seek to be disruptive to financial services, and especially lending across a variety of verticals — such as Hippo and OneConnect and Blend — are trading down 90% or more. Companies like OneConnect sport market capitalizations of around $100 million or a few hundred million dollars. For a bank, for example, taking all or part of the operations into its fold need not necessarily be a concern over price.

As detailed here, the prospect of bank-FinTech alliances and M&A can help bring profitability to the FinTechs (which has proven, by and large, elusive). And there are at least some trends that force FinTechs into the arms of more traditional (and well-capitalized) financial services mainstays.

For one thing, funding for these FinTechs has been pressured. CB Insights has estimated that global FinTech funding decreased 48% quarter-over-quarter in the second quarter of this year to $7.8 billion. That’s the lowest level seen since 2017.

In a recent interview with Karen Webster, Charlie Youakim, CEO of Sezzle, said that FinTechs bring some value and expertise to the banks.

“Banks are not great at digital, though they’re getting better at it,” said Youakim. And in at least some cases, when it comes to creating offerings at the digital cutting edge, “they don’t have the chops or the ability and talent, internally, to launch a new product or get it to scale.”

Verticals or focal points that may garner interest on the part of FIs stem from the fact that “many banks want to bring AI into the fold to help with investment advice. … If a bank can find a small startup that’s gaining momentum and has proven that their product works well, they can basically create the distribution platform within their bank that can explode it in terms of its capabilities or reach.”

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More