Public listings continue at a strong pace — at least as evidenced by announcements of intentions/plans to go public in the payments and financial services realms.

Through traditional initial public offerings (IPOs), it should be noted.

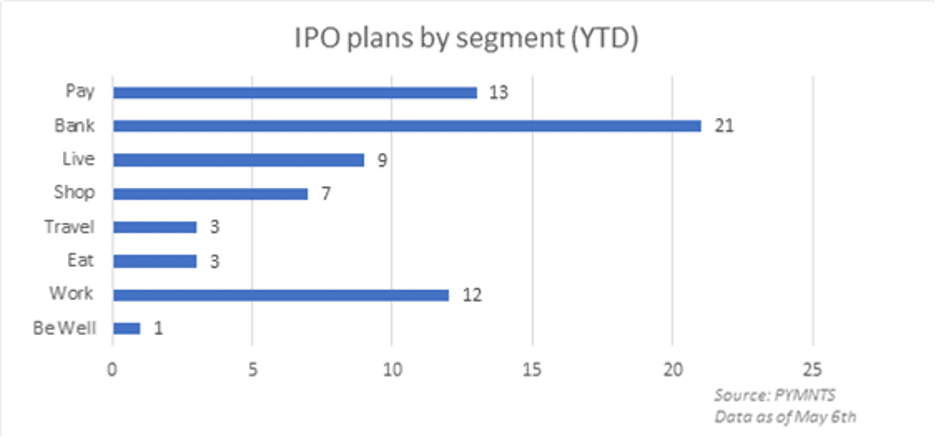

To that end, the IPO/SPAC Tracker finds in data that extends to May 6 that the payments space has logged 13 (planned) listings to date, outpaced by banking at 21.

CNBC has reported that increased interest in the SPAC space on the part of the Securities and Exchange Commission (SEC) has largely put the brakes on special purpose acquisition companies (SPACs). The question is whether the impact will last.

And, with a nod toward individual listings, earlier this month, cross-border eCommerce firm Global-e Online set terms for its planned IPO; the company said in a release it would offer 15 million shares at between $23 to $25, which would imply a valuation of between $3.3 billion to $3.6 billion. The Israel-based company has said that it has more than 440 merchant clients across smaller brands and global retailers.

Flywire set its own IPO plans last week that would look to raise as much as $300 million in an IPO, as Reuters reported. That comes on a confidential filing with SEC that would value the firm at as much as $3 billion; filings show the firm’s revenues in the latest quarter came to roughly $45 million, up about 38 percent year on year.

Paymentus Holdings, an electronic billing platform provider, filed last week with the SEC to raise about roughly $100 million. The company’s offerings include bill payment solutions, with choice of payment options. The SEC filing shows that during the year, the company’s revenues were $301 million, up from a bit more than $235 million in the previous period.

The SPAC Landscape: Momentum To Resume?

In an interview with PYMNTS conducted via written exchange, Bob Bartell, president of Duff & Phelps Corporate Finance, and David Larsen, managing director in the alternative asset advisory practice at Duff & Phelps (a Kroll business) said the chilling effect might not last long.

Bartell noted that “given the sponsor’s prior success, the SPAC investors tend to afford the sponsors some level of trust when asked to approve the deSPAC deal. Second, there is generally more disclosure for deSPAC deals relative to traditional IPOs.” Technology and healthcare have been among the more popular verticals, he said, though there has been “heightened interest in companies focused on sustainability and ESG.”

As to the heady pace of listings seen in 2020 and in the year to date, Bartell said investors have become somewhat “more disciplined with the due diligence process” and added that “SPAC boards have also increased the use of independent fairness opinions as a best practice.”

Bartell and Larsen noted that the SEC has increased its scrutiny on SPAC deals. But Bartell contended that the slowdown would be short term. Regulations, he said, ensure that investors get more information and trust in the process as a result.

“Given current market valuations and potential capital gains tax changes, we continue to believe there will be plenty of high-quality private equity-backed companies and corporate carve-outs to support the SPAC momentum for the foreseeable future,” Bartell told PYMNTS.

But, as always, risks are part of the process; Bartell and Larsen told PYMNTS that the SPAC sponsor is subject to reputational risk; the target company is subject to operating risk.

And with an eye on the SEC Staff Statement issued at the end of March, with additional statements last month, Larsen said that “the SPAC market was arguably super-heated. The SEC was reminding SPAC founders and targets of SPACs that existing regulation needs to be followed — there are no shortcuts with respect to disclosure, due diligence or complying with generally accepted accounting principles.”

Larsen pointed to the April 12 SEC Staff Statement as having had a particularly chilling impact on the SPAC market. He explained that the issue at hand centered on how to classify warrants within financial statements “SPACs had to take a pause and re-evaluate whether or not the equity accounting they had been using for the past decade plus was appropriate,” he said, and whether they might have to restate previous filings and financial statements.

“The three SEC statements, neither encourage or discourage the formation of SPACs and a SPAC’s goal to consummate a business combination,” said Larsen.

He predicted that once firms examine their accounting for warrants and other reporting issues, the SPAC market will likely continue, possibly at a slightly less frenetic pace, as long as there are sources of capital for SPACs to consummate acquisitions and as long as there continues to be a stable of private companies that are ready to withstand the scrutiny of the public markets.