Special purpose acquisition companies (SPAC) listings continue to outpace levels seen in any previous year — but regulatory scrutiny might slow the waves of new listings in the months ahead.

Thus far into 2021, as detailed by SPAC Research, there have been more than 300 listings, compared to 248 in all of 2020.

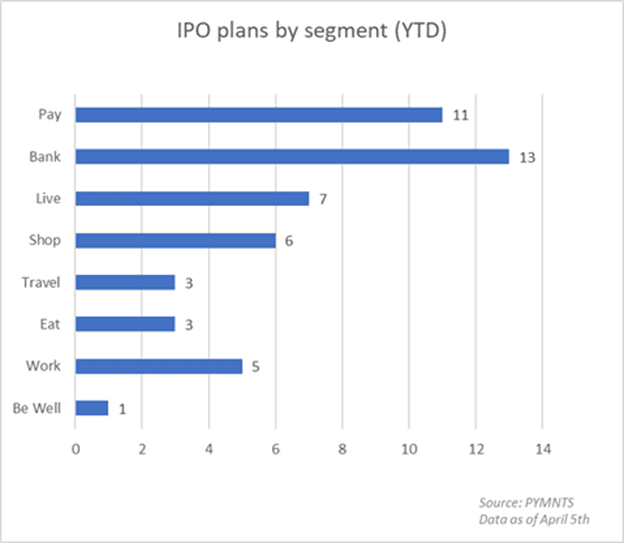

And within those initial public offerings (IPOs), the PYMNTS/SPAC Tracker shows that through the first week of April, there have been 13 banking/financial services IPOs, and 11 payment-related issues.

Drilling down into recent activity, Alkami Technology, a provider of cloud-based digital solutions for financial institutions (FIs), said last week that it plans an IPO that could value the firm at more than $2 billion. In its filing with the U.S. Securities and Exchange Commission (SEC), Alkami said it had recurring annual revenue of $128 million at the end of last year and a subscription revenue mix of 94 percent. Its user base is 9.4 million.

And among other headline grabbers (pun intended), Singapore’s ride-hailing super app Grab has said it will go public in the U.S. via a blank check merger with Altimeter Capital in a deal that gives the firm a valuation of about $35 billion,

The Regulatory Landscape

As detailed in this space last week, John Coates, acting director at the SEC’s corporate finance unit, warned of “some significant and yet undiscovered issues” with SPACs. In remarks at a conference, he said that there are “relatively as yet incompletely worked through mechanisms, despite the fact [SPACs] have been around for a while,” but noting that those issues would not stop SPAC deals and listings.

Coates’s observations come on the heels of a March release from the SEC’s Office of Investor Education and Advocacy. That release urged investors “not to make investment decisions related to SPACs based solely on celebrity involvement.” The SEC warned that “celebrities, like anyone else, can be lured into participating in a risky investment or may be better able to sustain the risk of loss.”

In a tweet that accompanied the release, Coates wrote that “the rapid increase in the volume of SPACs represents a significant change, and we are taking a hard look at the disclosures and other structural issues surrounding SPACs.”

At the end of last month, the SEC issued statements on considerations that should be examined by private companies mulling SPAC transactions. Among those considerations: record keeping and book-keeping germane to the disposition of assets or particulars related to transactions.

The SEC wrote that “It is critical that the board of directors, audit committee (as applicable), management, and auditors of these operating companies fully understand and fulfill their respective professional responsibilities so that companies meet their obligations under the federal securities laws and investors are provided with high-quality financial reporting at the time of the merger and on an ongoing basis in subsequent periods.”

Mike Tamulis, a managing director with Alvarez & Marsal‘s Transaction Advisory Group and leader of the firm’s Capital Markets and Accounting Advisory Practice, told PYMNTS in a written exchange that among the key risks facing the various stakeholders in a SPAC transaction, “we are seeing very compressed timelines for SPAC transactions, even when the target is less sophisticated.”

Historically, he noted, companies going through a traditional IPO spend a significant amount of time “preparing to be a public company — improving internal controls and financial reporting.”

But with the shortened timeframes tied to SPAC combinations, “we are seeing companies focused solely on what needs to get done to complete the transaction — primarily audits or re-audits of historical financial statements and preparation of the proxy statement.”

Smaller firms, he said, may not control environments that are as well designed as their larger brethren. “Small private companies typically lack proper segregation of duties which is a critical component of internal controls,” he said. The SEC statements, he said, serve as “a reminder that there is no grace period to comply with the books and records provisions and basic internal controls requirements.”

But, he said, the SEC statement is unlikely to discourage SPAC transactions and may not be a hint that, despite additional scrutiny, more regulation is on the horizon.

“Target company managements may be encouraged to slow a process down to allow appropriate time to prepare to be a public company, ensure basic internal controls are in place and feel comfortable signing financial statement certifications,” he told PYMNTS.